EV用バッテリーパックの市場機会と促進要因、産業動向分析、2025~2034年予測

EV Battery Pack Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 129 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740891

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

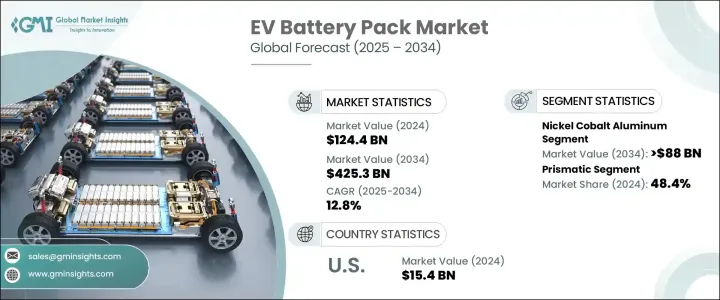

世界のEV用バッテリーパック市場は、2024年には1,244億米ドルとなり、電動モビリティへのシフトの加速、環境規制の高まり、強力な政策支援に後押しされ、CAGR 12.8%で成長し、2034年には4,253億米ドルに達すると推定されます。

各国が排ガス規制を強化し、持続可能な輸送を推進する中、高性能電気自動車の需要が急増しています。メーカーやエンドユーザーに対する補助金、税額控除、インセンティブといった政府の取り組みが、世界のEV普及をさらに後押ししています。自動車メーカーは、高まる消費者の期待に応えるためにEVポートフォリオを急速に拡大しており、効率的で信頼性の高いバッテリー・システムの必要性が高まっています。

リチウムイオン、ニッケル・コバルト・アルミニウム(NCA)、ソリッドステート技術などの電池化学の進歩により、エネルギー密度が向上し、充電時間が短縮され、電池全体の寿命が延びています。エネルギー貯蔵技術が進化するにつれて、消費者と自動車メーカーの双方がEVの大量導入に自信を示し、ダイナミックで競合情勢が形成されています。電池の研究開発への投資の増加、地域ギガファクトリーの設立、サプライチェーン全体での戦略的パートナーシップは、今後10年間にわたる業界の持続的成長の基盤を築いています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,244億米ドル |

| 予測金額 | 4,253億米ドル |

| CAGR | 12.8% |

電動モビリティへのシフトが勢いを増す中、自動車メーカーは生産能力を拡大し、より小型で高効率のバッテリーパックを統合するために車両アーキテクチャを再設計しています。このようなEV製造の急増は、より小型で軽量なフットプリント内でパワー、寿命、エネルギー密度のバランスをとる高度なバッテリー技術への需要を強めています。自動車メーカーは、安定供給を確保し、化学と設計のイノベーションを活用するため、バッテリーメーカーと戦略的提携を結んでいます。メーカーはまた、安全性を損なうことなく全体的な性能を高め、航続距離を最大化するために、軽量素材とモジュール式バッテリーシステムを優先しています。

ニッケル・コバルト・アルミニウム(NCA)電池化学は引き続き強力な牽引力となっており、EVバックアップ市場は2034年までに880億米ドルに達すると予想されています。高いエネルギー密度、軽量特性、長いサイクル寿命で知られるNCA電池は、自動車メーカーが効率を維持しながらEV性能を高めるのに役立っています。急速充電能力と優れた熱安定性により、増加する急速充電ステーション網のサポートに最適で、最終的には消費者の航続距離不安を緩和し、EV普及率全体を強化します。

プリズム型電池セルは2024年に48.4%の圧倒的なシェアを占め、自動車メーカーに設計の柔軟性を提供し、蓄電容量を最大化しながら、よりスマートで安全な電池パックを作ることができます。角形電池はケーシングが硬いため、物理的な損傷や膨張に対する保護が強化され、電池寿命の延長に貢献します。大手EVメーカーは、安全性と航続距離を優先した車両設計の進化に伴い急増する需要に対応するため、角形セルメーカーと長期供給契約を結んだり合弁会社を設立したりしています。

米国のEV用バッテリーパック市場は2024年までに154億米ドルを生み出し、13.1%のシェアを占める。2022年インフレ削減法のような連邦法が、クリーンエネルギー解決策への意識の高まりとともに、国内製造と投資を引き続き後押ししています。EVポートフォリオを拡大する既存の自動車メーカーは、この地域全体で先進的な高効率バッテリー・システムの必要性をさらに煽っています。

世界EV用バッテリーパック市場で企業が採用している主な戦略には、地域拡大、長期的なサプライチェーン・パートナーシップ、次世代電池技術への多額の投資などがあります。エネルギー密度と安全性を高めるための研究開発の優先、自動車メーカーや原材料サプライヤーとの協力関係の構築、重要鉱物の確保は、各ブランドが電気自動車の世界の需要急増に対応する弾力的なエコシステムを構築するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:電池形態別、2021-2034

- 主要動向

- 円筒形

- ポーチ

- プリズマティック

第6章 市場規模・予測:電池化学別、2021-2034

- 主要動向

- リン酸鉄リチウム

- ニッケルコバルトアルミニウム

- ニッケルマンガンコバルト

- マンガン酸リチウム

- その他

第7章 市場規模・予測:推進方式別、2021-2034

- 主要動向

- 電気自動車

- PHEV

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- スペイン

- 英国

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- FRIWO

- LG Energy Solution

- Octillion Power Systems

- Panasonic

- PMBL Limited

- Rivian

- Rapport

- Samsung

- TOSHIBA

- VARTA

目次

The Global EV Battery Pack Market was valued at USD 124.4 billion in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 425.3 billion by 2034, fueled by the accelerating shift toward electric mobility, rising environmental regulations, and robust policy support. As countries tighten emission norms and push for sustainable transportation, the demand for high-performance electric vehicles is skyrocketing. Government initiatives such as subsidies, tax credits, and incentives for manufacturers and end-users are further propelling EV adoption worldwide. Automakers are rapidly expanding their EV portfolios to meet growing consumer expectations, increasing the need for efficient and reliable battery systems.

Advances in battery chemistries like lithium-ion, nickel cobalt aluminum (NCA), and solid-state technologies are improving energy density, reducing charging times, and extending the overall lifespan of batteries. As energy storage technology evolves, both consumers and automakers are showing greater confidence in mass EV integration, creating a dynamic and competitive market landscape. Increasing investments in battery R&D, establishment of regional gigafactories, and strategic partnerships across the supply chain are laying the foundation for sustained industry growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $124.4 Billion |

| Forecast Value | $425.3 Billion |

| CAGR | 12.8% |

As the shift toward electric mobility gains momentum, automakers are scaling up production capabilities and redesigning vehicle architectures to integrate more compact, high-efficiency battery packs. This surge in EV manufacturing is intensifying demand for advanced battery technologies that balance power, longevity, and energy density within a smaller, lighter footprint. Automakers are forming strategic alliances with battery producers to ensure consistent supply and leverage innovations in chemistry and design. Manufacturers are also prioritizing lightweight materials and modular battery systems to enhance overall performance and maximize driving range without compromising safety.

Nickel cobalt aluminum (NCA) battery chemistry continues to gain strong traction, with the EV Backup Market expected to reach USD 88 billion by 2034. Known for high energy density, lightweight properties, and long cycle life, NCA batteries are helping automakers enhance EV performance while maintaining efficiency. Their fast-charging capability and superior thermal stability make them ideal for supporting the growing network of rapid charging stations, ultimately easing range anxiety for consumers and strengthening overall EV adoption rates.

Prismatic battery cells held a commanding 48.4% share in 2024, offering automakers design flexibility to create sleeker, safer battery packs while maximizing storage capacity. The rigid casing of prismatic cells provides enhanced protection against physical damage and swelling, contributing to extended battery life. Leading EV manufacturers are securing long-term supply agreements and forming joint ventures with prismatic cell producers to meet surging demand as vehicle designs evolve to prioritize safety and range.

The U.S. EV Battery Pack Market generated USD 15.4 billion by 2024, claiming a 13.1% share. Federal legislation like the Inflation Reduction Act of 2022, along with growing awareness of clean energy solutions, continues to boost domestic manufacturing and investment. Established automakers expanding their EV portfolios are further fueling the need for advanced, high-efficiency battery systems across the region.

Key strategies adopted by companies in the Global EV Battery Pack Market include regional expansion, long-term supply chain partnerships, and significant investment in next-generation battery technologies. Prioritizing R&D to enhance energy density and safety, building collaborations with automakers and raw material suppliers, and securing critical minerals are helping brands create resilient ecosystems that meet the surging global demand for electric vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Battery Form, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Cylindrical

- 5.3 Pouch

- 5.4 Prismatic

Chapter 6 Market Size and Forecast, By Battery Chemistry, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Lithium iron phosphate

- 6.3 Nickel cobalt aluminum

- 6.4 Nickel manganese cobalt

- 6.5 Lithium manganese oxide

- 6.6 Others

Chapter 7 Market Size and Forecast, By Propulsion Type, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 BEV

- 7.3 PHEV

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Spain

- 8.3.4 UK

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 FRIWO

- 9.2 LG Energy Solution

- 9.3 Octillion Power Systems

- 9.4 Panasonic

- 9.5 PMBL Limited

- 9.6 Rivian

- 9.7 Rapport

- 9.8 Samsung

- 9.9 TOSHIBA

- 9.10 VARTA

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 129 Pages

- 納期

- 2~3営業日