インドのEV用バッテリーパック:市場シェア分析、産業動向・統計、成長予測(2025年~2029年)

India EV Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029)- 発行日

- ページ情報

- 英文 276 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683875

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

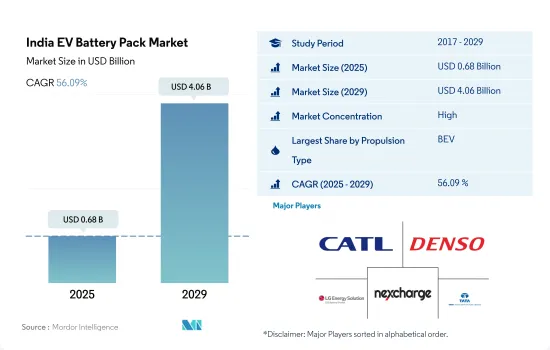

インドのEV用バッテリーパックの市場規模は2025年に6億8,000万米ドルと推定され、2029年には40億6,000万米ドルに達すると予測され、予測期間(2025-2029年)のCAGRは56.09%で成長する見込みです。

政府の政策、環境意識、プラグイン・ハイブリッド車に対するコスト優位性がインドの電気自動車用バッテリー産業を後押しすると予想される

- 電気自動車は、エネルギー効率を向上させ、汚染物質やその他の温室効果ガスの排出を減少させることを目的としているため、自動車産業にとって不可欠な存在となっています。政府による厳しい排ガス規制、電気自動車に関する認識、従来型自動車に対する電気自動車の利点、政府補助金などが、顧客の電気自動車への投資をさらに後押ししています。その結果、インドではバッテリー式電気自動車やプラグイン・ハイブリッド式電気自動車など、さまざまなタイプの電池でリチウムイオン電池の需要も増加しています。

- 電気自動車の選択肢が増えたため、バッテリー式電気自動車の需要はプラグイン・ハイブリッド式電気自動車に比べて高くなっています。その結果、純粋な電気自動車に使用される大型バッテリーの需要は、プラグイン電気自動車に使用されるものに比べて高いです。プラグイン・ハイブリッド技術はコストが高く、国内の誰もが簡単に購入できるものではないです。その結果、純粋な電気自動車に使用されるリチウムイオン電池がインドで成長しています。

- バッテリー電気自動車の需要の高まりも、リチウムイオン電池のニーズとともに拡大しています。しかし、様々な企業がプラグインハイブリッドのカテゴリーで新製品を発表しています。2023年1月、自動車博覧会でMGはプラグインハイブリッド電気自動車eHSを発表しました。新製品の発売により、2024年から2029年にかけてインドの電気自動車とバッテリー産業が活性化すると予想されます。

インドのEV用バッテリーパック市場動向

インドの電気自動車市場はタタ・モーターズが独占

- インドの電気自動車市場は初期段階にあります。市場は高度に統合されており、2022年には合計で市場の95%以上を占める大手5社によって大きく牽引されています。これらの企業には、トヨタ・グループ、MG、BYD India、タタ・モーターズ、現代自動車が含まれます。タタ・モーターズはインド最大の電気自動車販売会社で、EV販売シェアの約65%を占めています。国内メーカーとして、消費者からの信頼と信用を享受しています。価格戦略にも力を入れており、インドの他ブランドと比較して競争力のある価格で製品を提供しています。

- トヨタグループの市場シェアは約22%で、インド全土で電気自動車販売第2位となっています。同社は、成長する自動車業界において、手頃な価格設定の先進的な電動コンパクトSUVを提供しています。そのブランドイメージとインド市場における広大なプレゼンスが、同国における同社の成長を後押ししています。MGは電気自動車の販売台数で7.27%の第3位の市場シェアを占めています。技術的に先進的な製品を提供することで、インド市場でのシェアを拡大しています。

- ヒュンダイ・モーターズはインド全土のEV販売台数で4位につけています。韓国ブランドはここ数年、インドの顧客を強くつかんでおり、インドの電気自動車業界においても徐々にシェアを伸ばしています。インドのEV市場で第5位はBYDで、市場シェアは約1.1%です。インドでEVを販売している他のプレーヤーには、Mahindra、Kia、BMW、Mercedes、Olectraなどがあります。

インドの電気自動車販売の60%以上をタタ・モーターズが占め、バッテリーパック需要を牽引

- インドの電気自動車市場はまだ開拓段階にあり、電気自動車の需要は徐々に拡大しています。インドの消費者は経済的な選択肢を求めており、インドのさまざまなブランドが電気コンパクトSUVに優れた選択肢を提供することで、この需要に応えようとしています。その結果、インドではコンパクトSUVの需要が伸びています。インドでも近年、電動コンパクトSUVの需要が高まっています。

- 人々がスポーティで冒険的な乗り物を好むようになり、インドではコンパクトSUVの販売が好調です。タタ・ネクソンEVは、航続距離とパワーを備えたインドで最も手頃なフル電動コンパクトSUVの1つとして、2022年に大幅な販売増を記録しました。インドの人々は、トヨタの信頼性の高いブランドイメージのおかげで、トヨタのような様々なブランドに関心を示しています。同社はベストセラー・ブランドであり、2022年にはコンパクトSUVのアーバン・クルーザー・ハイライダーの販売が好調でした。

- ZS EVも2022年のインドEV市場でMGのベストセラーのひとつであり、航続距離250km以上のフル電動パワートレインやその他多くの魅力的な機能を備えています。インドのEV市場には、さまざまな国際ブランドの電動SUVやセダンもあります。一般的な車のひとつはヒュンダイ・コナで、2022年に好調な販売を記録しました。インドのEV市場で顧客に人気のある他の車には、Volvo XC 40 RechargeやTata Tigor EVなどがあります。

インドのEV用バッテリーパック産業概要

インドのEV用バッテリーパック市場はかなり統合されており、上位5社で98.33%を占めています。この市場の主要企業は以下の通りです。Contemporary Amperex Technology(CATL), Denso Corporation, LG Energy Solution Ltd., Nexcharge and Tata Autocomp Systems Ltd.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 電気自動車販売台数

- OEM別電気自動車販売台数

- 売れ筋EVモデル

- 選好されるバッテリーケミストリーを持つOEM

- 電池パック価格

- 電池材料コスト

- 各バッテリーケミストリーの価格表

- 誰が誰に供給するか

- EVバッテリーの容量と効率

- EVの発売モデル数

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ボディタイプ

- バス

- LCV

- M&HDT

- 乗用車

- 推進タイプ

- BEV

- PHEV

- バッテリーケミストリー

- LFP

- NCM

- NMC

- その他

- 容量

- 15 kWh~40 kWh

- 40 kWh~80 kWh

- 80kWh以上

- 15kWh未満

- バッテリー形状

- 円筒形

- パウチ

- 角型

- 方式

- レーザー

- ワイヤー

- コンポーネント

- アノード

- カソード

- 電解液

- セパレーター

- 材料タイプ

- コバルト

- リチウム

- マンガン

- 天然黒鉛

- ニッケル

- その他の材料

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Amara Raja Batteries Ltd.

- Contemporary Amperex Technology Co. Ltd.(CATL)

- Denso Corporation

- Exicom Tele-Systems Ltd.

- Exide Industries Ltd.

- LG Energy Solution Ltd.

- Manikaran Power Ltd.

- Nexcharge

- Panasonic Holdings Corporation

- Samsung SDI Co. Ltd.

- Tata Autocomp Systems Ltd.

- TOSHIBA Corp.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The India EV Battery Pack Market size is estimated at 0.68 billion USD in 2025, and is expected to reach 4.06 billion USD by 2029, growing at a CAGR of 56.09% during the forecast period (2025-2029).

Government policies, environmental awareness, and cost advantages over plug-in hybrids are expected to boost the electric vehicle battery industry in India

- Electric vehicles have become an essential part of the automotive industry, as they aim to improve energy efficiency and decrease emissions of pollutants and other greenhouse gases. Stringent emission norms by the government, awareness regarding electric vehicles, the benefits of EVs over conventional vehicles, and government subsidies further encourage customers to invest in electric vehicles. As a result, the demand for lithium-ion batteries is also increasing for various types of batteries, such as battery electric vehicles and plug-in hybrid electric vehicles in India.

- The demand for battery electric vehicles is higher compared to plug-in hybrid electric vehicles due to more options available for electric vehicles. As a result, the demand for large batteries used in pure electric vehicles is high compared to those used in plug-in electric vehicles. Plug-in hybrid technology is costly and is not easily affordable for everyone in the country. As a result, lithium-ion batteries used in pure electric vehicles have grown in India.

- The rising demand for battery electric vehicles is also growing, along with the need for lithium-ion batteries. However, various companies are launching new products in the plug-in hybrid category. In January 2023, at the auto expo, MG unveiled its plug-in hybrid electric car, eHS, which will be launched in India in the near future. Launching new products is expected to boost the electric vehicle and battery industry in India between 2024 and 2029.

India EV Battery Pack Market Trends

THE INDIAN ELECTRIC VEHICLE MARKET IS DOMINATED BY TATA MOTORS

- The Indian electric vehicle market is at an initial stage. The market is highly consolidated and largely driven by five major companies, which together held more than 95% of the market in 2022. These companies include Toyota Group, MG, BYD India, Tata Motors, and Hyundai. Tata Motors is the largest seller of electric vehicles in India, accounting for around 65% of the share in EV sales. As a domestic manufacturer, the company enjoys the trust and reliability of consumers. It extensively focuses on its pricing strategy and offers products with competitive pricing compared to other brands in India.

- Toyota Group holds a market share of around 22%, making it the second-largest seller of electric vehicles across India. The company offers advanced electric compact SUVs with affordable pricing in the growing automotive industry. Its brand image and vast presence in the Indian market have aided the growth of the company in the country. MG holds the third-highest market share of 7.27% in electric vehicle sales. The company is growing its share in the Indian market by offering technologically advanced products.

- Hyundai Motors has attained fourth place in EV sales across India. The South Korean brand has had a strong hold on Indian customers over the past few years and is also growing its share in the Indian electric vehicle industry gradually. The fifth-largest player operating in the Indian EV market is BYD, with a market share of around 1.1%. Some of the other players selling EVS in India include Mahindra, Kia, BMW, Mercedes, and Olectra.

TATA MOTORS ACCOUNTS FOR OVER 60% OF EV SALES IN INDIA, DRIVING BATTERY PACK DEMAND

- The Indian electric vehicle market is still in a developing phase, and the demand for electric vehicles is growing gradually in the country. Consumers in India are looking for economical options, and various brands in India are seeking to cater to this demand by offering good options for electric compact SUVs. As a result, the demand for compact SUVs is growing in the country. India has also witnessed an increasing demand for electric compact SUVs in recent years.

- The country has witnessed good sales of compact SUVs as people are gradually expressing a preference for sporty and adventurous rides, and India currently has limited options for electric sedans or hatchbacks. Tata Nexon EV recorded significant sales growth in 2022 as one of the most affordable full electric compact SUVs in India with good range and good power. People in India are showing interest in various brands such as Toyota, owing to the company's highly reliable brand image. The company is a bestselling brand and witnessed good sales of its compact SUV, Urban Cruiser Hyryder, in 2022.

- ZS EV was also one of the bestsellers from MG in the Indian EV market in 2022, with a full-electric powertrain with a range of 250+ km and many other attractive features. The Indian EV market also features a variety of electric SUVs and sedans from various international brands. One of the common cars is the Hyundai Kona, which registered good sales in 2022. Other cars in the Indian EV market that are popular with customers include Volvo XC 40 Recharge and Tata Tigor EV.

India EV Battery Pack Industry Overview

The India EV Battery Pack Market is fairly consolidated, with the top five companies occupying 98.33%. The major players in this market are Contemporary Amperex Technology Co. Ltd. (CATL), Denso Corporation, LG Energy Solution Ltd., Nexcharge and Tata Autocomp Systems Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 India

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Battery Chemistry

- 5.3.1 LFP

- 5.3.2 NCM

- 5.3.3 NMC

- 5.3.4 Others

- 5.4 Capacity

- 5.4.1 15 kWh to 40 kWh

- 5.4.2 40 kWh to 80 kWh

- 5.4.3 Above 80 kWh

- 5.4.4 Less than 15 kWh

- 5.5 Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 Method

- 5.6.1 Laser

- 5.6.2 Wire

- 5.7 Component

- 5.7.1 Anode

- 5.7.2 Cathode

- 5.7.3 Electrolyte

- 5.7.4 Separator

- 5.8 Material Type

- 5.8.1 Cobalt

- 5.8.2 Lithium

- 5.8.3 Manganese

- 5.8.4 Natural Graphite

- 5.8.5 Nickel

- 5.8.6 Other Materials

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Amara Raja Batteries Ltd.

- 6.4.2 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.3 Denso Corporation

- 6.4.4 Exicom Tele-Systems Ltd.

- 6.4.5 Exide Industries Ltd.

- 6.4.6 LG Energy Solution Ltd.

- 6.4.7 Manikaran Power Ltd.

- 6.4.8 Nexcharge

- 6.4.9 Panasonic Holdings Corporation

- 6.4.10 Samsung SDI Co. Ltd.

- 6.4.11 Tata Autocomp Systems Ltd.

- 6.4.12 TOSHIBA Corp.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 276 Pages

- 納期

- 2~3営業日