|

市場調査レポート

商品コード

1435988

冷凍野菜:市場シェア分析、業界動向と統計、成長予測(2024-2029)Frozen Vegetables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 冷凍野菜:市場シェア分析、業界動向と統計、成長予測(2024-2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

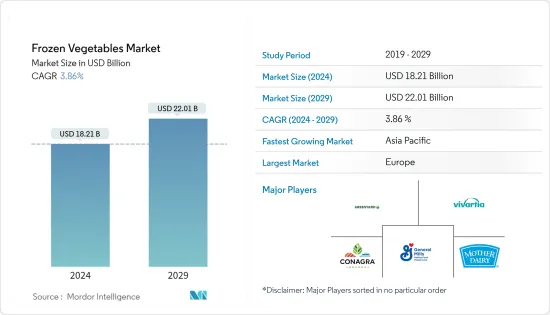

冷凍野菜市場規模は2024年に182億1,000万米ドルと推定され、2029年までに220億1,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.86%のCAGRで成長します。

主なハイライト

- 特に新興経済諸国における都市化の急速なペースは、可処分所得の増加と影響力の増大と相まって、さまざまな果物や野菜に関してコンビニエンス製品が中心的な地位を占めるようになりました。技術の進歩の変化に加え、包装の美しさ、保管のしやすさ、あらゆる用途での入手性の向上により、冷凍野菜の需要が高まっています。バランスのとれたコールドチェーンソリューションと接続された小売店の存在が市場の劇的な売上につながり、製品ポートフォリオのほとんどは地元の中小規模の農場によって提供されています。

- さらに、このセグメントは、市場のミレニアル世代の間で、生鮮食品、缶詰食品、調理済み食品や健康的なスナックの選択肢として好まれる代替品として人気を集めています。

- COVID-19の影響で、新型コロナウイルス感染症の発生後、冷凍野菜市場は好調に推移しています。冷凍野菜は栄養価を長期間保持できるため、消費者が店舗や販売店に足を運ぶ回数が減り、市場にとっても有利に働きます。COVID-19によるコールドチェーン供給への影響は大きいもの、健康志向が高まった消費者の購買パターンの進化により、冷凍野菜市場は予想よりも早く発展することができました。

冷凍野菜市場動向

インスタント食品の需要の増加

世界的に見て、若者(特にインドや中国などの新興諸国)は、さまざまな職業上の取り組みに積極的に取り組んでいるため、保存でき、すぐに食べられ、さらに賞味期限が長い食品をますます求めています。したがって、働くミレニアル世代は、定期的に野菜を切ったり買ったりする時間を減らすために、冷凍野菜を購入することを好みます。一方で、冷凍野菜の需要の急増により、食べたり調理したりするのに便利な商品のほうが有利であるようです。ラボバンクが分析した研究によると、欧州連合、特に米国からの冷凍サツマイモの輸入量が過去4年間で3倍に増加しており、そのため消費者が製品を貪り食う嗜好のレベルが高まっているとしています。

欧州が大きな市場シェアを保持

時間に追われている欧州の消費者の間で便利な食事ソリューションに対する需要は継続的に増加しており、これが欧州地域の冷凍野菜市場の成長を押し上げています。さらに、強い購買力と洗練された消費者を持つ欧州人は、一般的にアメリカ人の食の動向を反映する傾向があります。外食への消費支出の増加、特に若い消費者が平均よりも外食に多く支出していることで、欧州の冷凍野菜市場の収益はさらに押し上げられると思われます。この地域の消費者は、ライフスタイルの変化の一環として、ビーガンや健康的な食品に関心を持つようになってきています。高脂肪食品から低脂肪、高タンパク質の野菜や果物への大きな変化が見られます。したがって、これが市場の成長を促進しています。

冷凍野菜業界の概要

冷凍野菜市場は非常に細分化された市場であり、地域内および国際的な競合企業で構成されています。この市場は、ゼネラル・ミルズ社、コナグラ・ブランズ社、ピクトスイート・ファームズ社、マザー・デイリー・フルーツ&ベジタブル社などの企業によって独占されています。 Ltd、およびITCブランドなど。企業は、市場で競争上の優位性を得るために、製品の提供、成分、品質、価格、機能、サイズ、パッケージング、マーケティング活動などのさまざまな要素で競争します。主要企業は現在、より多くの顧客を引き付けるために、オンラインマーケティングと製品のブランディングのためにソーシャルメディアプラットフォームとオンライン流通チャネルに焦点を当てています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ別

- 豆

- トウモロコシ

- 豆

- キノコ

- カリフラワー

- アスパラガス

- ブロッコリー

- その他のタイプ

- 流通チャネル別

- スーパーマーケット/ハイパーマーケット

- 食料品店

- コンビニエンスストア

- その他の流通チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 北米のその他の地域

- 欧州

- スペイン

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- 南アフリカ

- サウジアラビア

- その他の中東とアフリカ

- 北米

第6章 競合情勢

- 最も活発な企業

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- General Mills Inc.

- Conagra Brands

- Pictsweet Farms

- Mother Dairy Fruit &Vegetable Pvt. Ltd

- Bonduelle Group

- Greenyard

- ITC Brands

- Vivartia

- Al-Kabeer Group

- Earthbound Farm

第7章 市場機会と将来の動向

第8章 COVID-19の市場への影響

The Frozen Vegetables Market size is estimated at USD 18.21 billion in 2024, and is expected to reach USD 22.01 billion by 2029, growing at a CAGR of 3.86% during the forecast period (2024-2029).

Key Highlights

- The rapid pace of urbanization, especially in the developing economies, coupled with growing disposable income and rising influence, has allowed convenience products to take center stage with regard to different fruits and vegetables. Altering technological advancements, along with aesthetic packaging, ease of storage, and all-around availability, are boosting the demand for frozen vegetables. The presence of well-balanced cold chain solutions and connected retail outlets have led to dramatic sales of the market, where most of the product portfolios are largely catered by local mid-and small-sized farms.

- Furthermore, this segment is gaining popularity as a preferred alternative to fresh, canned, and cooked food and healthy snack options among the millennial populations in the market.

- Due to the COVID-19, the frozen vegetable market has been performing well following the onset of the novel coronavirus. The fact that frozen vegetable is able to retain the nutritional value for a long period, and in turn, this helps bring down the number of times consumers have to visit the shop or outlet, which also works in favor of the market. Although the COVID-19 impact on the cold chain supply has been significant, the evolving buying patterns of the consumers with more inclination towards health have helped the frozen vegetable market develop faster than expected.

Frozen Vegetables Market Trends

Increasing Demand for Convenience Food Products

Since, globally, the younger population (particularly from the developing countries like India and China) is actively engaged in various professional commitments, they are increasingly looking for food products that can be stored and instantly eaten, also with more shelf life. Therefore, working millennials prefer to buy frozen veggies in order to decrease the vegetable cutting and buying time on a regular basis. On the other hand, the surge in demand for frozen vegetables seems to be more favorable for products that are convenient to eat and prepare as well. A study analyzed by RaboBank states that the import of frozen sweet potatoes in the European Union, particularly from the United States, has tripled over the last four years, hence, citing the level of consumer favoritism in devouring the product.

Europe Holds a Significant Market Share

Demand for convenient meal solutions among time-pressured European consumers has been witnessing a continuous increase, which is pushing the market growth of frozen vegetables in the European region. Furthermore, with strong purchasing power and sophisticated consumers, in general, the Europeans tend to mirror the food trends of the Americans. Increasing consumer spending on eating out, especially the younger consumers are spending more on eating than an average, will further boost the revenues in the European frozen vegetable market. Consumers in the region are becoming inclined toward vegan and healthy food as a part of lifestyle change. There has been a considerable shift from high-fat food products to low-fat and high-protein vegetables and fruits. Hence, this is boosting the market growth.

Frozen Vegetables Industry Overview

The frozen vegetables market is a highly fragmented market and comprises regional and international competitors. The market is dominated by players like General Mills Inc., Conagra Brands, Pictsweet Farms, Mother Dairy Fruit & Vegetable Pvt. Ltd, and ITC Brands, among others. Companies compete on different factors, including product offerings, ingredients, quality, price, functionality, size, packaging, and marketing activities, in order to gain a competitive advantage in the market. Key players are now focusing on social media platforms and online distribution channels for their online marketing and branding of their products to attract more customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Beans

- 5.1.2 Corn

- 5.1.3 Peas

- 5.1.4 Mushroom

- 5.1.5 Cauliflower

- 5.1.6 Asparagus

- 5.1.7 Broccoli

- 5.1.8 Other Types

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Grocery Stores

- 5.2.3 Convenience Stores

- 5.2.4 Other Distribution Channels

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Most Adopted Strategies

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 General Mills Inc.

- 6.4.2 Conagra Brands

- 6.4.3 Pictsweet Farms

- 6.4.4 Mother Dairy Fruit & Vegetable Pvt. Ltd

- 6.4.5 Bonduelle Group

- 6.4.6 Greenyard

- 6.4.7 ITC Brands

- 6.4.8 Vivartia

- 6.4.9 Al-Kabeer Group

- 6.4.10 Earthbound Farm