大豆油:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Soybean Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1910677

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

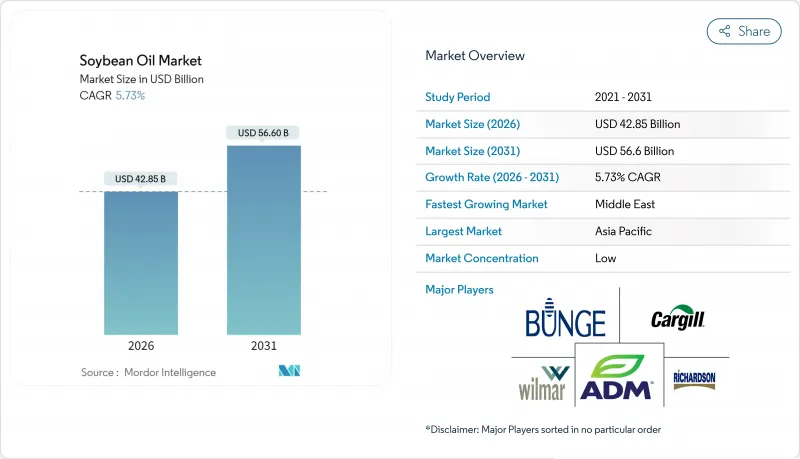

大豆油市場は2025年に405億3,000万米ドルと評価され、2026年の428億5,000万米ドルから2031年までに566億米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.73%と見込まれます。

この成長は、食料安全保障の確保、動物栄養の支援、低炭素燃料源としての役割において、大豆が極めて重要であることを示しています。主な成長要因としては、米国やブラジルなどの主要生産国における大豆生産量の増加と過去最高水準の搾油活動が挙げられます。これにより大豆油の供給が豊富となり、世界の価格下落圧力に寄与しています。家庭、消費財メーカー(FMCG)、外食産業からの安定した需要が消費基盤を支えています。北米では再生可能ディーゼル生産の増加が大豆油需要を押し上げ、製油所の生産能力拡大を促しています。アジア太平洋地域は、中国における家禽・水産養殖向け大豆粕の需要に牽引され、世界最大の消費地となっています。一方、中東地域は最も急速に成長している地域であり、湾岸諸国がサプライチェーンリスクを軽減するため食品輸入インフラへの投資を進めています。

世界の大豆油市場の動向と展望

拡大する畜産業が大豆粕消費を牽引

世界のタンパク質需要の増加は、大豆ミール消費を大幅に押し上げており、これが大豆油市場の成長を牽引しています。この相関関係は、大豆ミール需要の高まりが大豆の圧搾量増加を必要とし、この工程で製品別として大豆油も得られることに起因します。特に新興市場における畜産業は急速に拡大しており、大豆粕は動物飼料の重要なタンパク源として機能しています。米国では家禽が最大の国内消費部門として66.2%を占め、続いて豚が17.5%を消費しています(アイオワ大豆協会調べ)。都市化は食習慣にさらなる影響を与え、特にアジア太平洋地域において動物性タンパク質の消費増加をもたらしています。この変化は水産養殖分野で顕著であり、高タンパク飼料への需要が高まっています。同時に、世界の畜産業はより集約的で効率的な生産システムへ移行しており、成長を持続させるためには安定的で高品質なタンパク質原料が不可欠です。

拡大する食品加工・ファストフード産業が油消費を促進

大豆油の需要は、製造業者が大規模生産プロセス向けに安定性が高く風味が中立な油脂を優先する傾向が強まるにつれ、著しい成長を見せています。特に食品産業からのこの需要増加は、ファストフードチェーンの急速な拡大と加工食品製造セクターの成長に牽引されています。これらの動向は、利便性への嗜好の高まりや、可処分所得の増加が加工食品消費を促進する発展途上市場における都市化の影響など、より広範な消費者行動の変化を反映しています。食品加工業界が大豆油に依存する主な理由は、揚げ物用途への適性や製品の保存期間延長能力といった、その優れた機能特性にあります。こうした特性により、大豆油は多様な地域において一貫した品質と確実な供給が求められる世界の食品サプライチェーンにおいて、重要な構成要素となっています。

代替油糧種子の競合が成長を阻害

農家の輪作多様化が進む一方、加工業者はよりコスト効率の高い原料を積極的に模索しており、その結果、代替油糧作物が大豆油の市場シェアに重大な課題をもたらしています。キャノーラ油、ひまわり油、パーム油は、バイオディーゼル生産において大豆油の直接的な競合相手として台頭しています。この分野における顕著な動向として、使用済み食用油の輸入量が急増していることが挙げられます。輸入量は2021年の3億ポンド未満から、2023年には30億ポンド以上に拡大しました。この急増は、再生可能燃料生産における原料多様化への移行が加速していることを示しています。さらに、炭素強度評価メカニズムの導入により競合情勢は激化しており、廃棄物由来原料が未精製植物油よりも優先される傾向が強まっています。この動向は大豆油が再生可能燃料市場で築いてきた優位性を損なう可能性があります。タンパク質ミール分野での競争も激化しています。豚飼料の配合では中タンパク質代替品の採用により、大豆ミールの使用量が30%削減されました。

セグメント分析

従来型大豆油は市場を独占し続けており、2025年の総生産量の95.88%を占めています。この優位性は、堅牢なサプライチェーンと遺伝子改良による適応特性に支えられており、害虫抵抗性の向上や除草剤使用量の削減を通じて、最終的に生産コストの低減を実現しています。これらの要因により、従来型大豆は世界の商品市場において高い競争力を有しています。育種技術とバイオテクノロジーの進歩により、収量向上と圃場での性能改善が実現され、市場での地位はさらに強固なものとなっています。バイエル社が2027年に発売を予定している5種類の除草剤耐性を持つ大豆品種「Vyconic」は、農家の雑草管理における柔軟性を高め、収益性を大幅に向上させると期待されており、従来型大豆の市場での強みをさらに強化する見込みです。

有機大豆油は市場規模こそ小さいもの、非遺伝子組み換え(非GMO)製品やクリーンラベル製品に対する消費者需要の高まりを背景に、CAGR 7.44%という顕著な成長を遂げています。この分野の生産者は消費者信頼の維持を重視しており、農場監査、デジタルトレーサビリティシステム、第三者機関による検査など、厳格な対策の導入が進んでいます。この需要増に対応するため、加工業者は高コストにもかかわらず、従来型大豆との交雑汚染を防ぐ専用搾油施設への投資を進めています。有機農業は認証費用や雑草管理に追加費用がかかりますが、農場出荷時のプレミアム価格が生産者の継続的な取り組みを後押ししています。

大豆油市場レポートは、性質別(従来型と有機)、用途別(食品、飼料、工業用、その他)、地域別(北米、欧州、アジア太平洋、南米、中東・アフリカ)に分類されています。市場予測は金額(米ドル)と数量(リットル)で提供されます。

地域別分析

アジア太平洋地域は、世界市場の42.86%を占める最大の地域消費地として引き続き主導的な地位を維持しております。この優位性は、大豆粕や大豆油を主要な原料として多大に依存する畜産・水産養殖産業の急速な拡大によって支えられております。同地域の各国政府は、輸入依存度を低減するため、国内生産能力の強化や先進的な作物技術の承認に積極的に投資しております。加工業者は、効率の最適化と地域サプライチェーンの強化を図るため、特に主要港湾付近において、粉砕施設の近代化と拡張を進めています。こうした動きにより、大豆油製品に対する需要の増加に対応する安定した供給が確保されています。

中東地域は2031年までCAGR6.63%という堅調な伸びを示し、最も急速な成長が見込まれています。国家的な食料安全保障施策と、家禽・酪農産業における大豆由来原料の需要増加がこの成長を牽引しています。アラブ首長国連邦やサウジアラビアなどの国々は、飼料システムへの大豆ミールおよび大豆油の統合に注力すると同時に、現地の油糧種子加工インフラへの投資を進めています。気候制御された飼料工場や先進的な家禽複合施設の設立が、大豆油およびその派生製品の需要をさらに押し上げています。こうした取り組みにより、同地域は大豆油製品の主要な成長市場としての地位を確立しつつあります。

欧州では、持続可能性とサプライチェーンのレジリエンスという二つの優先課題を両立させながら、着実な成長を遂げております。厳格な環境規制と森林伐採防止政策の導入により、買い手は責任ある供給元から認証済みでトレーサビリティのある大豆油を調達するよう促されています。この変化は、デジタル監視システムの導入、透明性の向上、長期調達戦略の推進につながっています。同地域の持続可能な慣行への注力は市場情勢を再構築し、環境基準に適合し倫理的に調達された大豆油製品への移行を促進しています。これらの取り組みにより、欧州は世界の大豆油市場において重要な役割を担い続けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 拡大する畜産業が大豆ミール消費を牽引しております

- 食品加工業及びファストフード産業の拡大が油脂消費を促進しております

- 大豆油を用いたバイオディーゼル生産の成長

- 健康意識の高まりにより、ひまわり油などのより健康的な油への嗜好が変化しております

- 大豆油栽培における技術的進歩

- 再生可能エネルギーを促進する政府政策が、大豆油の需要を支えております

- 市場抑制要因

- 代替油糧種子の競合が成長を阻害しております

- 天候や貿易政策による世界の価格変動が成長を制限しております

- 高い生産コストが利益率に影響を及ぼします

- 耕作可能な土地の供給が限られているため、生産が制約されています

- バリューチェーン分析

- 規制の見通し

- テクノロジーの見通し

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額と数量)

- 性質別

- 従来型

- オーガニック

- 用途別

- 食品

- スプレッド

- ベーカリーおよび菓子類

- その他の用途

- 動物飼料

- 産業

- その他

- 食品

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- オランダ

- イタリア

- スウェーデン

- ノルウェー

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ベトナム

- インドネシア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、合弁事業、生産能力拡大)

- Market Positioning Analysis

- 企業プロファイル

- Cargill Incorporated

- Bunge Limited

- Wilmar International Ltd

- Richardson International Limited

- CHS Inc.

- The Scoular Company

- Archer-Daniels-Midland Company,

- Apical Group

- Granol S/A

- COFCO Group

- SD Guthrie Berhad

- AG Processing Inc.

- MWC Oil

- CJ Cheiljedang Corporation

- Nordic Soya Oy

- Galata Chemicals

- Louis Dreyfus Company B.V.

- Limketkai Manufacturing Corporation

- AMAGGI Group

- OLVEA Group

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日