|

市場調査レポート

商品コード

1850125

データセンター電力:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データセンター電力:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月16日

発行: Mordor Intelligence

ページ情報: 英文 176 Pages

納期: 2~3営業日

|

概要

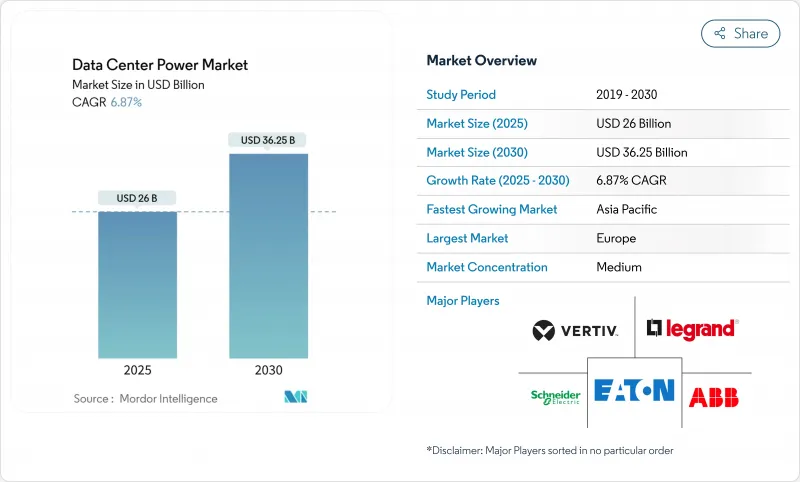

データセンター電力の市場規模は2025年に245億6,000万米ドルと予測され、CAGR 7.25%で推移し、2030年には348億6,000万米ドルに達すると予測されています。

人工知能の展開の拡大、積極的なハイパースケール容量の追加、より厳格な信頼性の義務化は、電気インフラの優先順位を再形成し、データセンター電力市場の拡大に拍車をかけています。高密度のAIワークロードは従来のCPUの3倍の電力を消費するため、事業者はより高電圧の配電、液体冷却、グリッド・インタラクティブ・パワー・トレインへと向かっています。電力会社、規制当局、クラウドプロバイダーが、数ギガワットの相互接続を必要とする大規模プロジェクトで足並みを揃える中、機器サプライヤー間の統合が進んでいます。引退した石炭発電所をキャンパス型施設に再利用する参入企業が増える中、データセンター電力市場は、受動的なエネルギー消費から能動的なグリッド参加へと移行しつつあり、アンシラリーサービスを通じて新たな収益源を引き出しています。

世界のデータセンター電力市場の動向と洞察

ハイパースケールとクラウドコンピューティングの拡大

ハイパースケール事業者は、中規模都市の電力需要に匹敵するキャンパスを稼働させています。メタ社の2GWの開発と5.6GWのワンダーバレー・サイトは、クラウドの成長を維持するために必要な規模を示しています。シュナイダーエレクトリックは、2025年の受注量の24%をデータセンターが占めていることを明らかにしました。電力会社の相互接続を段階的な容量解放に結びつける構造化契約は一般的になりつつあり、電力会社、地主、クラウドのテナント間のリスク配分が改善されています。IT負荷が1メガワット増加するごとに、スイッチギア、UPS、中電圧システムへの投資が比例して増加するため、データセンター電力市場が直接利益を得る。

AIによる高密度ワークロード

AIアクセラレータは、ラック密度を5~10kWから50~100kWに引き上げ、48V DC配電、高位相数、液冷への移行を迫ります。Vertivの360AIプラットフォームは、統合バスウェイ、冷却液分配、リーク検出制御により、ラックあたり100kWをサポートします。持続的な熱負荷はUPS機器のデューティサイクルを増加させるため、部分負荷時の効率曲線は重要な選択指標となります。国際エネルギー機関の予測によると、AIは2029年までに世界の電力の1.5%を消費する可能性があり、GPUの使用率と同期して動的にスロットルを切り替えるエネルギー比例電源システムの緊急性が高まっています。電源と冷却をコンパクトなプレハブ・ブロックに統合するベンダーは、オペレーターが予測可能な導入スケジュールを求める中、シェアを獲得しています。

電気インフラの高いCAPEX

AI対応キャンパスのエンド・ツー・エンドのコストは、MWあたり3,800万米ドルに迫り、液冷はパワートレインの支出を空冷ベースの設計に比べて15~20倍に膨らませる。小規模なコロケーション事業者は、カスタマイズされた中電圧ギア、長リード変圧器、特殊バッテリーのための資金を確保することが困難です。サービスとしての設備契約が台頭しつつあるが、特注スイッチギヤの二次市場価値は限られているため、金融機関は慎重な姿勢を崩していないです。予算の制約が新興国での事業拡大を遅らせ、データセンター電力市場の好調な軌道を弱めています。資金調達のギャップは、地主と電力会社が共同出資する合弁モデルにも拍車をかけ、リターンは希薄化するが、プロジェクトの実行可能性は確保されます。

セグメント分析

UPSプラットフォームは2024年にデータセンター電力市場シェアの62.1%を維持し、送電網の不安定性に対する最後の防衛手段としての役割を明確にしました。リチウムイオンの採用は続いているが、低密度ホールでのコスト優位性から、バルブ制御鉛蓄電池が依然として主流です。インテリジェントなスイッチモード整流器は変換ロスを削減し、施設全体のエネルギープロファイルを改善します。並行して、配電装置はCAGR7.5%を記録しています。これは、事業者が分岐回路監視、温度検知、安全なファームウェアを組み込むようになったためです。発電機は依然として不可欠であるが、水素対応発電機が試験的に使用されるようになり、シナリオは変化しています。スイッチギヤのアップグレードはAIラックが要求する高電圧に対応し、バッテリーエネルギー貯蔵システムはピークカットと収益積み上げのために支持されるようになります。

UPSベンダーがグリッド・サービス・モジュールを追加し、ライドスルー性能を損なうことなく周波数調整を可能にすることで、エコシステムのダイナミクスが変化します。Vertivのグリッド・インタラクティブ・ファームウェアは、クリティカルでない時間帯に予備容量をディスパッチします。デルタのスマートPDU I-Typeは、高密度のAIエンクロージャーをターゲットに、メータリング機能とリモートアップグレード機能を42mmのシャーシに統合しています。高密度ホールの試運転には、熱マッピング、高調波調査、継続的なファームウェアの検証が必要なため、サービス収入は増加します。その結果、オペレーターはライフサイクルサポートを外注し、インテグレーターの予測可能な年金形式の収入源を促進し、データセンター電力市場を豊かにします。

コロケーション施設は2024年のデータセンター電力市場規模において43.8%のシェアを占めています。しかし、ハイパースケーラはCAGR 8.7%を占め、アップル、マイクロソフト、グーグルのAIホスティングゾーンの自前構築戦略に後押しされています。エンタープライズ・キャンパスはコンプライアンスに敏感な業界のために存続し、エッジノードはレイテンシを低減するために人口クラスタの近くに増殖しています。ハイパースケーラはオンサイトの変電所とバッテリーファームを統合した独自の電力トポロジーを設計し、コロケーションのプレーヤーは柔軟な電力密度と相互接続ファブリックで対抗します。

競合の緊張がイノベーションを促進する:コアサイトは液体チップ冷却と48Vバスウェイを次世代ホールの標準として宣伝し、クラウド大手は15MW単位でモジュールブロックを改良しています。両陣営とも、資本配分と即時の稼働を切り離した従量制の契約を採用しています。エッジ事業者は、5Gの展開に歩調を合わせるため、標準化されたマイクロパワーモジュールを導入します。このような戦略が絡み合うことで、データセンター電力市場に流入する機器の数量が増加します。

地域分析

欧州が2024年の売上高シェア34.18%で首位。事業者は、エネルギー効率指令を満たすために、レガシー施設を高効率UPSとバッテリーストレージで改修します。Sines DCのような石炭発電所の転換は、既存の系統連系と海水取水ラインを再利用し、環境への影響を抑えながら導入を加速します。ベンダーは、風力の強い地域の送電網を安定させるグリッドインタラクティブUPSを供給し、持続可能な設計における欧州大陸のリーダーシップを強化しています。企業バイヤーは、再生可能な原産地保証がネット・ゼロの誓約をサポートし、データセンター電力市場全体の機器需要を維持するため、欧州のサイトを好みます。

アジア太平洋地域は、政府がクラウドコリドーに資金を供給し、土地、ファイバー、電力に補助金を出しているため、CAGRが最速の9.2%となっています。2024年下半期の時点で、アジア太平洋地域の実稼働IT容量は12,206MWで、14,338MWが建設中です。マイクロソフトはインドと日本で数十億米ドル規模の計画を発表し、事業拡大の規模を強調しています。中国がPUE上限規制を実施し、高効率電力部品の発注が加速。インドのデジタル個人データ保護法は、国内ホスティングを推進し、再生可能エネルギー・クラスターに近い新キャンパスを刺激します。東南アジア諸国は、ハイパースケーラーを誘致するために減税措置を講じ、スイッチギア、UPS、スマートPDUの調達パイプラインをさらに広げています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ハイパースケールとクラウドコンピューティングの拡張

- AI駆動型高密度ワークロード

- より厳格な稼働時間と冗長性基準

- 持続可能性とエネルギー効率の義務

- グリッドインタラクティブな収益源

- 石炭火力発電所跡地をキャンパス用に再利用

- 市場抑制要因

- 電気インフラの高額な設備投資

- 炭素強度規制と報告

- 変圧器/配電装置の供給ボトルネック

- 変電所拡張に対する地元の反対

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- コンポーネント別

- 電気ソリューション

- UPSシステム

- 発電機

- ディーゼル発電機

- ガス発生器

- 水素燃料電池発電機

- 配電ユニット

- スイッチギア

- 転送スイッチ

- リモート電源パネル

- エネルギー貯蔵システム

- サービス

- 設置と試運転

- メンテナンスとサポート

- トレーニングとコンサルティング

- 電気ソリューション

- データセンタータイプ別

- ハイパースケーラー/クラウドサービスプロバイダー

- コロケーションプロバイダー

- エンタープライズおよびエッジデータセンター

- データセンター規模別

- 小規模データセンター

- 中規模データセンター

- 大規模データセンター

- 巨大規模データセンター

- メガサイズデータセンター

- ティアレベル別

- ティアIとティアII

- ティアIII

- ティアIV

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリアとニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Schneider Electric SE

- Vertiv Holdings Co.

- ABB Ltd

- Eaton Corporation plc

- Legrand SA

- Huawei Technologies Co. Ltd

- Fujitsu Ltd

- Cisco Systems Inc.

- Rittal GmbH and Co. KG

- Mitsubishi Electric Corp.

- Cummins Inc.

- Kohler Power Systems

- PDU Experts UK Ltd

- Schleifenbauer Products BV

- Delta Electronics Inc.

- Caterpillar Inc.

- Socomec Group

- Tripp Lite(by Eaton)

- Riello UPS S.p.A.

- KEHUA Tech