|

|

市場調査レポート

商品コード

1549905

アジア太平洋地域のデータセンター向け電力:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Asia-Pacific Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のデータセンター向け電力:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

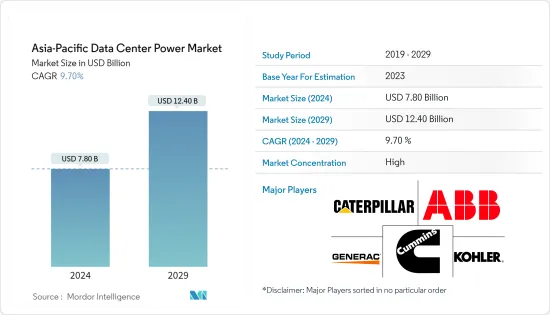

アジア太平洋のデータセンター向け電力市場規模は、2024年に78億米ドルと推定され、2029年には124億米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは9.70%で成長すると予測されます。

アジア太平洋は、5G技術の導入増加に後押しされ、エッジデータセンターの需要が急増しています。データトラフィックの増加、データセンターの建設とサーバーの増加により、電力ソリューションの需要が高まっています。事業者は、水素化植物油(HVO)、天然ガス、その他の環境に優しい代替品で稼働する新時代の発電機セットの採用を模索しています。このような要因によって、市場の拡大が見込まれています。

主要ハイライト

- アジア太平洋データセンター電力市場の今後のIT負荷容量は、2029年までに2万3,000kWに達すると予想されます。

- 同地域の床面積は2029年までに7,450万平方フィート増加すると予想されます。

- 同地域で設置されるラックの総数は、2029年までに420万個に達すると予想されます。2029年までに最大数のラックが設置されると予想されるのはインドです。

- アジア太平洋を結ぶ海底ケーブルシステムは160近くあり、その多くが建設中です。2024年に開通が予定されている東南アジア-日本ケーブル2(SJC2)は、中国、台湾、日本、韓国、タイ、ベトナムを陸揚げ点とする10,500kmを超える海底ケーブルです。

アジア太平洋データセンター電力市場動向

ITと電気通信が大きなシェアを占める

- アジア太平洋では、ハイパーコネクティビティ環境が、消費者や企業のコネクティビティやコラボレーションのニーズをサポートする上で基礎的な役割を果たす通信事業者の重要性を強化しています。アジア太平洋全体では、通信事業者の75%がプラス成長を記録しました。韓国は、通信市場成熟度の世界ランキングで香港に次いで2位です。韓国はまた、6Gを含む最新の通信開発の最先端を走っています。投資の面では、2022年11月にマレーシアのCelcomとDiGiが合併契約を承認しました。両社が完全に合併すれば、新会社は2,000万人以上の加入者を抱えるマレーシア最大級の通信事業者となります。

- アジア太平洋における5Gの登場は、高速ネットワーク接続のためのスモールセル展開を加速させています。多くの国が、新しいスモールセルを展開する際に適用できる免責基準を設けています。例えばシンガポールでは、情報通信メディア開発庁(IMDA)がビル開発者や所有者に対し、通信機器や通信プロバイダーに屋上スペースを無償で提供するよう指示しています。

- 政府による好意的なポリシーとポリシーは、データセンターへの新規投資を呼び込む上で極めて重要です。こうしたポリシーにより、データセンター市場を支える経済的・社会的資本が充実した環境が育まれています。マレーシア政府は、スマートグリッドを確立し、再生可能エネルギーの割合を2025年に31%、2035年に40%に引き上げることを目標としています。この政府の取り組みは、サステイナブル電力スケーラビリティに関する懸念に対処し、ハイパースケーラーやプロバイダーの需要を満たす可能性があります。このようなシナリオは、バックアップ電源ソリューションの需要にも対応します。

- 技術革新の面では、2023年6月現在、バーティブはアジアにおけるデータセンター事業者の省エネ達成を支援する熱管理最適化サービス「Vertiv EnerSav」を発表しています。バーティブはVertiv EnerSavサービスを導入し、事業者がインフラを大幅に見直すことなくエネルギー消費を削減することで、施設内のコスト削減機会を特定できるよう支援します。このサービスは、東南アジア、ニュージーランド、オーストラリアを含むアジア全域で利用可能です。

著しい成長を遂げるインド

- インドは世界で最も急成長している経済国のひとつであり、電力システムを利用する複数のエンドユーザーセグメントが複合的に影響しているため、大きな市場成長が期待されています。

- 現在のデータセンターの大半は、ムンバイ、チェンナイ、ハイデラバードに建設されています。中央政府と州政府は、データセンターポリシーと優遇措置の草案を発表しました。ウッタル・プラデシュ州やテランガナ州など一部の州はすでにポリシーを展開しています。インドでは電力や水などの資源がさらに不足しているため、市場関係者はこれまで以上にクリーンで環境に優しいデータセンターの実現に努めると考えられます。冷却とそれを支えるバックアップのインフラ・コンポーネントは、より効率的でクリーンなオプションへと進化していくことが期待されています。

- ポリシー面では、インド政府と各州政府は、税制補助金を通じてインドのデータセンターのインフラ成長を支援するため、データセンターポリシーの再策定を進めています。データセンターに関する国家ポリシーの枠組みのもと、IT省は最大1,500億インドルピー(18億米ドル)を奨励金として支給する意向です。このポリシーに基づき、政府は今後5年間でデータセンターのエコシステムに最大3兆インドルピー(350億米ドル)を投資する予定です。

- 国連の気候変動に関する政府間パネルは、インドは今後数十年で、より頻繁で激しい気象現象の影響を受けると予測しています。気候の影響や異常気象に直面しても持続可能で回復力のあるデータセンターを目指すデータセンター・プロバイダーにとって、立地選定や気候関連の災害シナリオはますます重要な計画ツールとなっています。このような要因により、バックアップ電源ソリューションに対する大きな需要が生じています。

- パンデミック以来、クラウドコンピューティングは企業、政府、消費者にとってミッションクリティカルな技術として発展してきました。2023年には、企業の65%がクラウドの採用を前年より増やし、組織の84%がSaaSを採用しました。FacebookとGoogleは、インドにメガプロジェクトを設立し、カーボンフットプリントの削減を図っています。全体として、データセンター向け電力市場は良好な状態にあります。

アジア太平洋データセンター電力産業概要

アジア太平洋のデータセンター向け電力市場は、各参入企業の間で若干の統合が進んでおり、近年は競合を高めています。同市場の主要参入企業には、ABB Ltd.、Caterpillar Inc.、Cummins Inc.などがいます。市場シェアの高いこれらの大手企業は、地域全体の顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な共同イニシアティブを活用しています。

2023年3月、Vertiv Group Corp.は、Vertiv Geist Upgradeable Rack PDUにC13/19兼用コンセントが付属し、購入、在庫管理、配備を簡素化すると発表しました。Vertiv Geistアップグレード可能ラック型PDUのユニバーサルC13/C19コンセントは、新しいラック構成に容易に対応できるため、ラック密度が増加するにつれてrPDUを変更または交換する必要がなくなります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- メガデータセンターとクラウドコンピューティングの導入拡大

- 運用コスト削減需要の高まり

- 市場抑制要因

- 設置とメンテナンスのコスト高

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- 電力インフラ

- 電気ソリューション

- UPSシステム

- 発電機

- 配電ソリューション

- PDU

- スイッチギア

- クリティカル配電

- 転送スイッチ

- リモートパワーパネル

- その他

- サービス

- 電気ソリューション

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- メディア・エンターテイメント

- その他

- 地域

- オーストラリア

- 中国

- インド

- インドネシア

- フィリピン

- シンガポール

- マレーシア

- 日本

- ニュージーランド

- タイ

- 香港

- 台湾

- ベトナム

- 韓国

第6章 競合情勢

- 企業プロファイル

- ABB Ltd

- Caterpillar Inc.

- Cummins Inc.

- Eaton Corporation

- Legrand Group

- Rolls-Royce PLC

- Vertiv Group Corp.

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Fujitsu Limited

- Cisco Systems Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Asia-Pacific Data Center Power Market size is estimated at USD 7.80 billion in 2024, and is expected to reach USD 12.40 billion by 2029, growing at a CAGR of 9.70% during the forecast period (2024-2029).

Asia-Pacific is experiencing a surge in demand for edge data centers, fueled by the rising deployments of 5G technology. Increasing data traffic and data center constructions and servers are laying the demand for power solutions. Operators are exploring the adoption of new-age generator sets that run on hydrotreated vegetable oil (HVO), natural gas, and other eco-friendly alternatives. These factors are expected to augment the market studied.

Key Highlights

- The upcoming IT load capacity of the Asia-Pacific data center power market is expected to reach 23 K MW by 2029.

- The region's construction of raised floor area is expected to increase by 74.5 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 4.2 million units by 2029. India is expected to house the maximum number of racks by 2029.

- There are close to 160 submarine cable systems connecting the Asia-Pacific, and many are under construction. One such submarine cable that is estimated to start service in 2024 is Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 km with landing points in China, Taiwan, Japan, South Korea, Thailand, and Vietnam.

Asia-Pacific Data Center Power Market Trends

IT and Telecom to Hold Significant Share

- In Asia-Pacific, the hyper-connectivity environment has reinforced the importance of telcos, which play a foundational role in supporting consumers' and enterprises' connectivity and collaboration needs. Across Asia-Pacific, 75% of the operators registered positive revenue growth. South Korea is second to Hong Kong in the world rankings of telecom market maturity. The country is also on the leading edge of the latest telecom developments, including around 6G. In terms of investment, in November 2022, Malaysian companies Celcom and DiGi approved the merger agreement. Once the two companies are fully merged, the new entity will be one of the largest carriers in Malaysia, with over 20 million subscribers.

- The advent of 5G in Asia-Pacific has accelerated small-cell deployment for high-speed network connectivity. Many nations have created exemption standards that can be applied when deploying new small cells. For instance, in Singapore, The Infocomm Media Development Authority (IMDA) has directed the building developers and owners to provide rooftop spaces free of charge for telecommunication equipment and telecom providers.

- Favorable policies and regulations from governments have been pivotal in attracting new investments in data centers. These policies have nurtured an environment with substantial economic and social capital that supports the data center market. The Malaysian government aims to establish a smart grid and increase the proportion of renewable energy to 31% in 2025 and 40% in 2035. This government initiative may address the concerns regarding sustainable power scalability and meet the demands of hyperscalers and providers. Such scenarios also address the demand for backup power solutions.

- In terms of innovations, as of June 2023, Vertiv unveiled a thermal management optimization service, the Vertiv EnerSav, to help data center operators achieve energy savings in Asia. Vertiv introduced the Vertiv EnerSav service to help operators identify cost-saving opportunities within their facilities by reducing energy consumption without needing a significant infrastructure overhaul. The service is available across Asia, including Southeast Asia, New Zealand, and Australia.

India to Register Significant Growth

- India is one of the fastest-growing economies in the world, and due to the combined impact of several end-user segments utilizing power systems, the country is expected to showcase major market growth.

- A majority of the current data centers are being built in Mumbai, Chennai, and Hyderabad. The central and state governments came up with the draft data center policies and incentives. Some states like Uttar Pradesh and Telangana have already rolled out the policies. As resources like power and water have become even more scarce in India, market players will strive to make cleaner and greener data centers than ever before. The cooling and supporting backup infra components are expected to evolve into more efficient and cleaner options.

- In terms of policy, the Government of India and various state governments are redrafting their data center policies to support the infrastructural growth of data centers in India through tax subsidies. Under a national policy framework for data centers, the IT ministry intends to provide up to INR 15,000 crore (USD 1.8 billion) as incentives. As per the policy, the government plans to invest up to INR 3 lakh crore (USD 35 billion) in the data center ecosystem over the next five years.

- The United Nations Intergovernmental Panel on Climate Change anticipates that India will be affected by more frequent and intense weather events in the coming decades. Site selection and climate-related disaster scenarios are becoming increasingly important planning tools for data center providers who aim to be sustainable and resilient in the face of climate impact and extreme weather events. Such factors lead to a major demand for backup power solutions.

- Since the pandemic, cloud computing has evolved as a mission-critical technology for businesses, governments, and consumers. In 2023, 65% of enterprises increased their cloud adoption compared to the previous year, and 84% of the organizations adopted SaaS. Facebook and Google are establishing their mega projects in India and taking measures to lower their carbon footprints. Overall, the data center power market is in favorable condition.

Asia-Pacific Data Center Power Industry Overview

The Asia-Pacific data center power market is slightly consolidated among the players and has gained a competitive edge in recent years. A few major players in the market include ABB Ltd, Caterpillar Inc., and Cummins Inc. These major players with a prominent market share focus on expanding their customer base across the region. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

In March 2023, Vertiv Group Corp. announced that its Vertiv Geist Upgradeable Rack PDUs come with a combination outlet C13/19, simplifying purchasing, inventory management, and deployment. The universal C13/C19 outlet on Vertiv Geist Upgradeable Rack PDUs can easily accommodate new rack configurations, eliminating the need to modify or replace rPDUs as rack densities increase.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Mega Data Centers and Cloud Computing

- 4.2.2 Increasing Demand to Reduce Operational Costs

- 4.3 Market Restraints

- 4.3.1 High Cost of Installation and Maintenance

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Power Infrastructure

- 5.1.1 Electrical Solution

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.3 Power Distribution Solutions

- 5.1.1.3.1 PDU

- 5.1.1.3.2 Switchgear

- 5.1.1.3.3 Critical Power Distribution

- 5.1.1.3.4 Transfer Switches

- 5.1.1.3.5 Remote Power Panels

- 5.1.1.3.6 Others

- 5.1.2 Service

- 5.1.1 Electrical Solution

- 5.2 End User

- 5.2.1 IT and Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media and Entertainment

- 5.2.5 Other End Users

- 5.3 Geography

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Philippines

- 5.3.6 Singapore

- 5.3.7 Malaysia

- 5.3.8 Japan

- 5.3.9 New Zealand

- 5.3.10 Thailand

- 5.3.11 Hong Kong

- 5.3.12 Taiwan

- 5.3.13 Vietnam

- 5.3.14 South Korea

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ABB Ltd

- 6.1.2 Caterpillar Inc.

- 6.1.3 Cummins Inc.

- 6.1.4 Eaton Corporation

- 6.1.5 Legrand Group

- 6.1.6 Rolls-Royce PLC

- 6.1.7 Vertiv Group Corp.

- 6.1.8 Schneider Electric SE

- 6.1.9 Rittal GmbH & Co. KG

- 6.1.10 Fujitsu Limited

- 6.1.11 Cisco Systems Inc.