|

市場調査レポート

商品コード

1549824

イタリアのデータセンター電力:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Italy Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イタリアのデータセンター電力:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

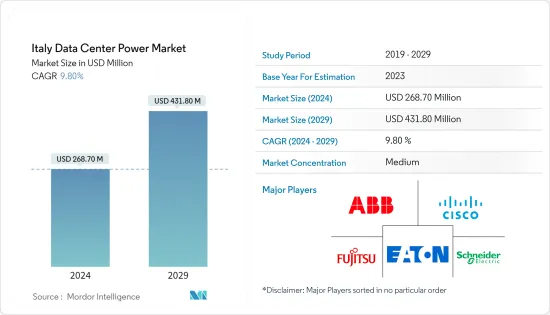

イタリアのデータセンター電力市場規模は、2024年に2億6,870万米ドルと推定され、2029年には4億3,180万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは9.80%で成長する見込みです。

中小企業におけるクラウドコンピューティング需要の増加、データセキュリティに関する政府規制、国内企業による投資の拡大などが、同国のデータセンター需要を促進する主な要因となっています。

主なハイライト

- 建設中のIT負荷容量:イタリアのデータセンター市場における今後のIT負荷容量は、2029年までに300MWに達すると予想されます。

- 建設中の高床スペース:イタリアでは2029年までに200万平方フィート以上の増床が見込まれています。

- 計画中のラック:国内の設置予定ラック総数は、2029年までに102,000ユニットに達する見込みです。2029年までに最大数のラックが設置されるのは大ミラノ地域であろう。

- 計画されている海底ケーブル:イタリアを結ぶ海底ケーブルシステムは32近くあり、その多くが建設中です。

データ・ストレージへのニーズの高まりにより、データ・センターの数が急増し、データ・センターの利用増加により国内の電力消費量も増加しています。イタリアは、電力・天然ガス市場の競争激化で明らかに前進しました。化石燃料の使用を減らし、再生可能エネルギーの割合を増やしました。また、同国の経済はエネルギー集約型ではなくなりつつあります。さらに、エネルギー消費量をさらに削減するため、主要市場プレーヤーは、データセンターにおける不必要な支出を抑制する目的で、PDU、バスウェイ、UPSなどの効率的な電源管理システムの導入に注力しており、これが市場の成長を促進すると予想されます。

イタリアのデータセンター電力市場の動向

IT・通信セグメントが市場の主要シェアを占める

- 同国ではクラウド・コンピューティング・サービスの導入が進んでおり、ITインフラ・コンポーネントの数が増加しています。多くのテクノロジー企業がクラウドサービスを開始し、多くの企業のデジタルトランスフォーメーションの取り組みをサポートしています。さらに、eコマース・サービスの導入が増加していることも、デジタル化を促進しています。こうした事例が、予測期間中のイタリアのデータセンター電力市場を押し上げると予想されます。

- さらに、データセンター市場は、統合や新たなプレイヤーの出現など、コネクテッドデバイスの普及拡大により新記録を達成しつつあります。このようなケースは、市場の成長にプラスの影響を与えると予想されます。

- イタリアのデータセンターのサーバー数は、こうしたデジタルサービスに対する需要の高まりにより増加するとみられます。主にデジタル接続に焦点を当てたエンドユーザーの採用形態の変化により、より多くのデータストレージが必要となります。通常、このような状況はデータセンター需要の増加に対応します。データセンターの増加には、より多くの電力供給システムが必要となります。

- 国内におけるデータ消費の増加は、通信サービス・プロバイダー間の競争が激化し、データ通信に関する割引やオファーが増加したこと、および消費者の間で4Gおよび5Gサービスが採用され、モバイル・データの利用しやすさが向上したことに起因します。5G端末の増加により、平均データ通信速度が向上するため、データ消費量が大幅に増加する可能性があります。このような動きは、データセットを効率的に処理・分析するためのデータセンター設備に対する重要な需要を生み出すと予想されます。

- イタリアではインターネット交換設備の数が非常に多いため、この地域がファイバー接続の拡大からどのような恩恵を受けるかが明らかになり、地域の接続ポートフォリオの強化に共同で貢献することになります。強力なインターネット交換設備がデータセンターのデータトランスミッション機能を支えており、これがデータセンター電力市場にプラスの影響を与えると予想されます。

市場で大きなシェアを占めると予想されるPDU

- 全国的なデジタル化、インターネット普及、eコマースへの注目の高まりにより、ストレージ容量のニーズが高まり、その結果、データセンターの需要が膨大になり、電力消費量が増加しています。データストレージに対するニーズの高まりは、データセンターにおける電力消費を最適化するため、単純なマルチソケットラック設置やサーバー、ネットワーク機器ではなく、インテリジェント配電ユニット(PDU)の採用につながっています。

- PDUは、データセンターやサーバールームのインフラに不可欠なコンポーネントであり、消費電力、電圧、電流、その他の電気パラメータをリアルタイムで監視することができます。このデータにより、管理者は電力配分やキャパシティプランニングについて、十分な情報に基づいた意思決定を行うことができます。

- 消費電力の動向を追跡することで、管理者は将来の成長を計画し、電力容量の超過を回避し、機器の故障につながる過負荷を防ぐことができます。また、非効率を特定し、エネルギー消費を最適化することもできます。これにより、不要な電力消費をなくし、コストを削減し、環境への影響を低減します。さらに、管理者はリモートでアクセスして制御できるため、物理的な立ち会いの必要性が減り、運用の中断を最小限に抑えることができます。

- 産業用エンドユーザーは、Microsoft Azure、Google Cloud、AWSなどのクラウドプラットフォームに注目しています。成長動向は、エンドユーザーによるクラウドベースのアプリケーションの急速な採用を示しています。これにより、このようなプラットフォームを運用するための電力要件の増加に対応できる、インテリジェントでコンパクトなPDUが求められるようになります。

- また、国内におけるメガデータセンターや大規模データセンターの増加に伴い、PDUのニーズも高まっています。インターネット速度の高速化と、それに伴うアクセス可能なデバイスの普及は、国内のデータ消費量の決定と見積もりに重要な役割を果たしています。5Gモバイル接続数は大幅に増加しており、これは国内における5Gモバイルの普及率が高いことを意味します。データトラフィックの増加は、インテリジェントPDUシステムを備えたDC設備への需要をさらに高める可能性があります。

イタリアのデータセンター電力業界の概要

イタリアのデータセンター電力市場は、初期投資が高く、リソースの利用可能性が低いため、適度に集中しています。シュナイダーエレクトリックSE、富士通株式会社、シスコテクノロジー株式会社、イートン株式会社、ABB株式会社など、少数の大手企業によって支配されています。圧倒的な市場シェアを持つこれらの大手企業は、海外における顧客基盤の拡大に注力しています。大手企業は、市場シェアと収益性を高めるために、戦略的な共同イニシアティブを活用しています。しかし、技術の進歩や製品の革新に伴い、中小企業も新規契約の獲得や新市場の開拓によって市場での存在感を高めています。例えば

- 2024年1月:ヴェルティヴは、2025年までにバスウェイ、スイッチギア、統合モジュラー・ソリューション(IMS)の製造能力を倍増させる計画を発表しました。この拡張計画には、アラブ首長国連邦、アイルランド、サウスカロライナ(米国)、メキシコ、スロバキア、北アイルランドでの稼働率向上と拠点拡大が含まれます。

- 2023年12月インテリジェントパワーマネージメントカンパニーであるイートンは、高いセキュリティと事業継続性をデータセンターに提供する新しいラックPDU G4(第4世代)の発売を発表しました。また、C14とC20電源コードの両方を安全に接続するC39アウトレットを組み合わせて、ロック機構と電源コードを固定する内蔵高保持システムによってバックアップされます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- メガデータセンターとクラウドコンピューティングの導入拡大

- 運用コスト削減需要の高まり

- 市場抑制要因

- 導入・保守コストの高さ

- バリューチェーン/サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- 電力インフラ別

- 電気ソリューション

- UPSシステム

- 発電機

- 配電ソリューション

- PDU

- スイッチギア

- クリティカル配電

- 転送スイッチ

- リモート電力パネル

- その他の配電ソリューション

- サービス

- 電気ソリューション

- エンドユーザー別

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他のエンドユーザー

第6章 競合情勢

- 企業プロファイル

- ABB Ltd

- Caterpillar Inc.

- Cummins Inc.

- Eaton Corporation

- Legrand Group

- Rolls-Royce PLC

- Vertiv Group Corp.

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Fujitsu Limited

- Cisco Systems Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Italy Data Center Power Market size is estimated at USD 268.70 million in 2024, and is expected to reach USD 431.80 million by 2029, growing at a CAGR of 9.80% during the forecast period (2024-2029).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

Key Highlights

- Under construction IT load capacity: The upcoming IT load capacity of the data center market in Italy is expected to reach 300 MW by 2029.

- Under construction raised floor space: The country's construction of raised floor area is expected to increase by more than 2.0 million sq. ft by 2029.

- Planned racks: The country's total number of racks to be installed is expected to reach 102,000 units by 2029. The Greater Milan region will likely house the maximum number of racks by 2029.

- Planned submarine cables: There are close to 32 submarine cable systems connecting Italy, and many are under construction.

The increasing need for data storage has resulted in an upsurge in the number of data centers, and the rising usage of data centers has increased electricity consumption in the country. Italy made clear progress in increasing competition in electricity and natural gas markets. It has reduced the use of fossil fuels and increased the share of renewable energy. The country's economy is also becoming less energy-intensive. Moreover, to further reduce energy consumption, key market players are focusing on introducing efficient power management systems such as PDUs, busways, and UPS for the purpose of controlling unnecessary expenditures in data centers, which is expected to drive the market's growth.

Italy Data Center Power Market Trends

IT & Telecommunication Segment to Hold Major Share in the Market

- The increased adoption of cloud computing services in the country has increased the number of IT infrastructure components. Many technology companies have launched cloud services to support the digital transformation efforts of many enterprises. Moreover, the increased adoption of e-commerce services has facilitated digitization. These instances are anticipated to boost the Italian data center power market during the forecast period.

- Moreover, the data center market is achieving new records due to the increasing penetration of connected devices, including consolidation and the emergence of new players. Such cases are expected to have a positive impact on the market's growth.

- The number of servers in data centers in Italy is likely to increase due to the growing demand for these digital services. Changing adoption of end users, primarily focused on digital connectivity, requires more data storage. Typically, this situation corresponds to increased demand for data centers. Increasing data centers necessitates more systems for power facilitation.

- The increase in data consumption in the country is a result of the high competition among telecom service providers, leading to increased discounts and offers on data and the adoption of 4G and 5G services among consumers, which increased the affordability of mobile data. The increase in the number of 5G devices may significantly increase data consumption because of the increased average data speeds delivered, which would further generate more data to be processed. Such developments are expected to generate crucial demand for data center facilities to efficiently handle and analyze data sets.

- The significant number of internet exchanges in Italy highlights how the region will benefit from fiber connectivity expansion, jointly contributing to strengthening the region's connectivity portfolio. The highly potent internet exchange facilities support data centers for data transmission functions, which is expected to positively affect the data center power market.

PDUs Expected to Hold Significant Share in the Market

- The growing focus on digitization, internet penetration, and e-commerce across the country has created more need for storage capacity, resulting in huge demand for data centers and increased power consumption. The growing need for data storage is leading to the adoption of intelligent power distribution units (PDUs) to optimize power consumption in data centers rather than simple multi-socket rack installations and servers and networking devices.

- PDUs are essential components of data center and server room infrastructure, allowing real-time monitoring of power consumption, voltage, current, and other electrical parameters. This data allows administrators to make informed decisions about power allocation and capacity planning.

- By tracking power consumption trends, managers can plan for future growth and avoid exceeding power capacity, preventing overloads that can lead to equipment failure. It also helps identify inefficiencies and optimize energy consumption. This eliminates unnecessary power consumption, lowers costs, and reduces environmental footprint. In addition, administrators can access and control it remotely, reducing the need for physical presence and minimizing disruption to operations.

- Industrial end users are gravitating toward cloud platforms such as Microsoft Azure, Google Cloud, and AWS. Growth trends indicate rapid adoption of cloud-based applications by end users. This opens up opportunities for intelligent and compact PDUs that can meet the increasing power requirements to operate such platforms.

- With the growth of mega and massive data centers in the country, the need for PDUs is also increasing. Faster internet speeds and the associated proliferation of accessible devices play an important role in determining and estimating national data consumption. The number of 5G mobile connections has increased significantly, which means that the penetration rate of 5G mobile in the country is high. Increased data traffic may further increase the demand for DC facilities with intelligent PDU systems.

Italy Data Center Power Industry Overview

The data center power market in Italy is moderately concentrated due to higher initial investments and low availability of resources. It is dominated by a few major players like Schneider Electric SE, Fujitsu Ltd, Cisco Technology Inc., Eaton Corporation, and ABB Ltd. These major players, with a prominent market share, focus on expanding their customer base across foreign countries. Major companies leverage strategic collaborative initiatives to increase their market share and profitability. However, with technological advancements and product innovations, mid-size to smaller companies have increased their market presence by securing new contracts and tapping new markets. For instance,

- January 2024: Vertiv announced plans to double its manufacturing capacity for busway, switchgear, and integrated modular solutions (IMS) by 2025. The expansion plans include increasing the utilization and footprint in the United Arab Emirates, Ireland, South Carolina (United States), Mexico, Slovakia, and Northern Ireland.

- December 2023: Eaton, an intelligent power management company, announced the launch of its new Rack PDU G4 (4th generation) that provides high security and business continuity data centers. It also combines with C39 outlets that securely connect both C14 and C20 power cords, backed by a locking mechanism and a built-in high retention system that secures the power cord.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Mega Data Centers and Cloud Computing

- 4.2.2 Increasing Demand to Reduce Operational Costs

- 4.3 Market Restraints

- 4.3.1 High Cost of Installation and Maintenance

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Power Infrastructure

- 5.1.1 Electrical Solution

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.3 Power Distribution Solutions

- 5.1.1.3.1 PDU

- 5.1.1.3.2 Switchgear

- 5.1.1.3.3 Critical Power Distribution

- 5.1.1.3.4 Transfer Switches

- 5.1.1.3.5 Remote Power Panels

- 5.1.1.3.6 Other Power Distribution Solutions

- 5.1.2 Service

- 5.1.1 Electrical Solution

- 5.2 By End User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ABB Ltd

- 6.1.2 Caterpillar Inc.

- 6.1.3 Cummins Inc.

- 6.1.4 Eaton Corporation

- 6.1.5 Legrand Group

- 6.1.6 Rolls-Royce PLC

- 6.1.7 Vertiv Group Corp.

- 6.1.8 Schneider Electric SE

- 6.1.9 Rittal GmbH & Co. KG

- 6.1.10 Fujitsu Limited

- 6.1.11 Cisco Systems Inc.