|

市場調査レポート

商品コード

1549897

アフリカのデータセンター向け電力:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Africa Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのデータセンター向け電力:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

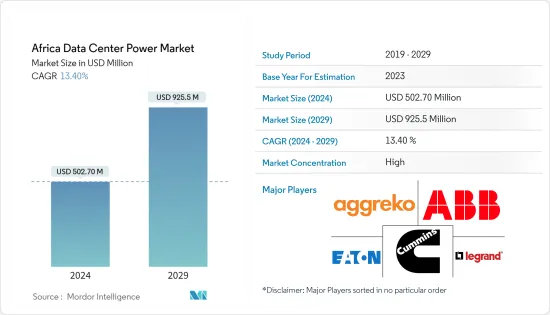

アフリカのデータセンター電力市場規模は、2024年に5億270万米ドルと推定され、2029年には9億2,550万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは13.40%で成長する見込みです。

アフリカのデータセンターは相当量の電力を使用しており、商用直流電力の使用量は、導入の加速に伴い、過去5年間で年平均40%増加しています。2022年には4,000GWhを超えると予想されていました。南アフリカの送電網は信頼性と安定性に課題があり、データセンターの運用に支障をきたす可能性があります。データセンターは、中断のない運用を確保するために信頼性の高い安定した電力供給を必要としており、送電網の不安定性は持続可能性への取り組みに影響を与えかねないです。このような要因が大きな市場需要につながっています。

主要ハイライト

- アフリカのデータセンター電力市場における今後のIT負荷容量は、2029年までに1,226MWに達すると予想されます。

- 同地域の床面積は2029年までに520万平方フィート増加すると予想されます。

- 同地域の総設置ラック数は2029年までに2億6,000万個に達すると予想されます。2029年までに最も多くのラックが設置されるのは南アフリカです。

アフリカを結ぶ海底ケーブルシステムは70近くあり、その多くが建設中です。2024年にサービス開始が予定されているそのような海底ケーブルのひとつがAfrica-1で、エジプトのポートサイドとラス・ガレブ(Ras Ghareb)を陸揚げ点とする1万km以上に及ぶものです。

アフリカのデータセンター電力市場動向

ITと電気通信が大きなシェアを占める

- 電気通信事業者は主にコンテンツ配信を推進し、モバイルサービスやクラウドサービスを促進する役割を担っているため、電気通信データセンターには高い接続性が求められます。この特殊なタイプのデータセンターは、他のデータセンター、クラウドプロバイダー、通信事業者とOSPケーブルで接続され、効率的な運用を確保するためにクロスコネクトが広く導入されています。

- ナイジェリアは、南アフリカに次ぐアフリカ大陸第2位の経済規模に支えられ、アフリカ最大級の通信市場を有しています。ナイジェリアの通信規制機関であるナイジェリア通信委員会は2023年2月、同国におけるアクティブなモバイル通信プランの契約数が2023年に約2,225億7,100万件に達したと報告しており、ナイジェリアにおけるモバイルサービスの需要が高いことを示しています。全体として、ネットワーク・トラフィックの増加は、大規模なデータセンター投資と直流電源の導入につながっています。

- NCC(ナイジェリア通信委員会)によると、2022年6月現在、ナイジェリアのブロードバンド普及率は44.30%で、加入者数は8,400万件を超えています(2022年には約7,600万件)。COVID-19はリモートワーク方式で加入者数を増加させました。データセンター建設の増加に伴い、同市場の需要も増加すると予想されます。

- 4Gの急速な普及と来るべき5Gの波は、アフリカのデータセンター電力市場に投資する通信ベンダーを固守しています。2022年10月、南アフリカの通信プロバイダーTelkomは、中国のHuawei Technologiesの協力を得て5G高速インターネット網を確立しました。ファーウェイは南アフリカの5Gネットワーク開発を引き続き支援しています。アフリカ大陸の著名な5Gネットワークには、2800以上の基地局が配備されています。

- 5Gの展開は、拡大計画を推進し、計画通りに実行する上で重要な役割を果たすと考えられます。5Gネットワークとユビキタスブロードバンドのためには、16万7,000kmのファイバーインフラが必要です。ファイバー接続が拡大し、先進技術を遠隔地から利用できるようになれば、ナイジェリアではデータセンター施設の需要が高まると考えられます。このような要因から、データセンターの電力導入が進むと考えられます。

著しい成長を遂げる南アフリカ

- サハラ以南のアフリカでは最近、データセンターインフラへの投資が進んでいるもの、同大陸の容量の多くは南アフリカにとどまっており、現地プロバイダーは2017~2019年にかけて50MW以上のデータセンター専用IT負荷容量をオンライン化しました。

- 南アフリカでは、化石燃料に大きく依存した不安定な電力供給が続いており、価格もますます高くなっていることが、データセンター産業にとって大きな課題となっています。安定した電力供給の重要性に加え、責任ある企業市民活動、環境・社会・ガバナンス(ESG)プラクティスへの適合が相まって、データセンター・オーナーには、アフリカ大陸でサービスを提供し、アフリカがその他と歩調を合わせられるようにするための大きなプレッシャーとなっています。

- 南アフリカの年間日照時間は2,500時間を超え、平均日射量は1日4.5~6.5 kWh/m2です。1平方メートルあたり約220ワットという南アフリカの平均日射量は、欧州(100W/m2)の2倍以上です。したがって太陽エネルギーは、送電網への依存を減らすための最も有望な再生可能エネルギーのひとつです。北ケープ州は太陽光発電所投資のホットスポットとなっており、予測期間中の太陽光発電機の主要な需要が見込まれています。

- クラウドスイッチドPDUシリーズは、先進的サージ保護、シームレスなクラウド管理、容易な設置を特長とする汎用性の高い電源管理ソリューションを記載しています。この未開拓の市場から利益を得るために、様々な大手クラウド企業が国内での投資を増やしながらこのようなPDUを採用しています。AWSは、同国でデータセンターインフラを立ち上げる計画を発表しました。AWSは、クラウドコンピューティングサービスに対する顧客の需要に応えるため、2022年までに156億ZAR(8億5,800万米ドル)を投資しました。

- また、スイッチ型配電ユニットでは、主要な担当者が個々のコンセントのオン/オフを遠隔操作できます。これにより、オペレータは重要な負荷を管理し、無駄な電力を回避し、機器が正しい位相に接続されていることを確認し、スケジュールを管理することができます。南アフリカでは、HPEがHPE G2 Metered and switched PDUを提供しており、コンセントレベルの電力測定とスイッチングにより、ローカルとリモートの電力管理を実現しています。LCD画面によるローカルモニタリングとアラート表示、セキュアなWeb、SNMP、CLI、またはTelnetインターフェースによるリモートアクセスと設定が可能です。

アフリカのデータセンター向け電力産業概要

アフリカのデータセンター向け電力市場は、各参入企業の間で若干の統合が進んでおり、近年は競合優位性を獲得しています。市場の主要企業には、Aggreko ZA、ABB Ltd、Cummins Inc.などがいます。市場シェアの高いこれらの大手企業は、地域全体の顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な共同イニシアティブを活用しています。

- 2024年4月、重要なデジタルインフラと継続性ソリューションの重要なプロバイダーであるVertivは、5kVA~10kVAの世界電圧(GV)(200V~240V、デフォルト230V)用のVertiv Liebert GXT5リチウムイオンダブルコンバージョン、オンライン無停電電源装置(UPS)システムの拡大を発表しました。

- 2024年1月、Caterpillar Inc.はMicrosoftとBallard Power Systemsと提携し、数メガワットのデータセンター向けに、信頼性が高く環境に優しいバックアップ電源として大型水素燃料電池の使用を検査しました。水素燃料電池は、ディーゼルバックアップ発電機に代わる低炭素の代替電源となる可能性があり、直流発電機の成長を促進すると期待されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- メガデータセンターとクラウドコンピューティングの導入拡大

- 運用コスト削減需要の高まり

- 市場抑制要因

- 設置とメンテナンスのコスト高

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- 電力インフラ

- 電気ソリューション

- UPSシステム

- 発電機

- 配電ソリューション

- PDU

- スイッチギア

- クリティカル配電

- 転送スイッチ

- リモートパワーパネル

- その他

- サービス

- 電気ソリューション

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- メディア・エンターテイメント

- その他

- 地域

- 南アフリカ

- ナイジェリア

第6章 競合情勢

- 企業プロファイル

- ABB Ltd

- Caterpillar Inc.

- Cummins Inc.

- Eaton Corporation

- Legrand Group

- Rolls-Royce PLC

- Vertiv Group Corp.

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Fujitsu Limited

- Cisco Systems Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Africa Data Center Power Market size is estimated at USD 502.70 million in 2024, and is expected to reach USD 925.5 million by 2029, growing at a CAGR of 13.40% during the forecast period (2024-2029).

African data centers use a considerable amount of power, and commercial DC power usage has been growing by an average of 40% annually over the past five years as adoption has accelerated. It was expected to pass the 4,000 GWh mark in 2022. South Africa's power grid has experienced challenges with reliability and stability, leading to potential disruptions in data center operations. Data centers require a reliable and stable power supply to ensure uninterrupted operations, and grid instability can impact their sustainability efforts. Such factor leads to major market demand.

Key Highlights

- The upcoming IT load capacity of the Africa data center power market is expected to reach 1,226 MW by 2029.

- The region's construction of raised floor area is expected to increase 5.2 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 260 K units by 2029. South Africa is expected to house the maximum number of racks by 2029.

There are close to 70 submarine cable systems connecting Africa, and many are under construction. One such submarine cable that is estimated to start service in 2024 is Africa-1, which stretches over 10,000 km with landing points in Port Said and Ras Ghareb in Egypt.

Africa Data Center Power Market Trends

IT and Telecom to Hold Significant Share

- Telecom providers are primarily responsible for driving content delivery and facilitating mobile and cloud services, which is why telecom data centers require high connectivity. This specific type of data center is connected to other data centers, cloud providers, and telecom operators through outside plant (OSP) cables, with cross-connects extensively deployed to ensure efficient operations.

- Nigeria has one of the largest telecom markets in Africa, supported by the second-largest economy on the continent after South Africa. In February 2023, the Nigerian Communications Commission, the Nigerian telecom regulator, reported that the number of active mobile telecommunication plan subscriptions in the country reached about 222,571 million in 2023, which shows the demand for mobile services in Nigeria. Overall, the increasing network traffic is leading to major data center investment and DC power adoption.

- According to the NCC (Nigerian Communications Commission), as of June 2022, Nigeria's broadband penetration was 44.30%, with more than 84 million subscriptions, compared to about 76 million in 2022. COVID-19 boosted subscriber counts under remote working schemes. With increasing data center construction, the demand for the market is expected to increase.

- The rapidly increasing 4G penetration and the upcoming 5G wave are adhering telecom vendors to invest in the African data center power market. In October 2022, the South African telecom provider Telkom established the 5G high-speed internet network with the help of Huawei Technologies from China. Huawei continues to assist South Africa in developing its 5G networks. The prominent 5G network on the African continent has more than 2,800 base stations deployed.

- The deployment of 5G would play a key role in pushing the expansion plans and executing them as planned. For 5G networks and ubiquitous broadband, the country requires 167,000 km of fiber infrastructure. Data center facilities will be in demand in Nigeria as fiber connectivity increases and advanced technologies can be used remotely. Such factors will lead to major data center power adoption.

South Africa to Register Significant Growth

- Despite recent investments in data center infrastructure in Sub-Saharan Africa, much of the continent's capacity remains in South Africa, where local providers brought more than 50 MW of dedicated data center IT load capacity online between 2017 and 2019.

- In South Africa, unstable power supplies that are still heavily fossil fuel dependent and increasingly expensive are significant challenges for the data center industry. Over and above the critical importance of a stable power supply, responsible corporate citizenship, and meeting environmental, social, and governance (ESG) practices combine to put significant pressure on data center owners to service the continent and ensure that Africa can keep pace with the rest of the world.

- South Africa receives more than 2,500 hours of sunshine annually, with average solar radiation levels ranging between 4.5 and 6.5 kWh/m2 daily. The country's average solar radiation of about 220 Watts per square meter is more than double that of Europe (100 W/m2). Solar energy, therefore, is one of the most promising renewable energy options for reducing dependency on the grid. The Northern Cape has become a hotspot for solar power plant investments, which expects the major demand for solar generators during the forecast period.

- The cloud switched PDU series provides a versatile power management solution featuring advanced surge protection, seamless cloud management, and easy installation. To take benefit of this untapped market, various large cloud companies are adopting such PDUs with increasing investment in the country. AWS announced plans to launch data center infrastructure in the country. AWS invested ZAR 15.6 billion (USD 858 million) through 2022 to meet customer demand for cloud computing services.

- Switched power distribution units also allow key personnel to control the on/off state of individual outlets remotely. This allows operators to manage critical loads, avoid wasted power, ensure equipment is plugged into the correct phase, and manage schedules. In South Africa, HPE offers HPE G2 metered and switched PDU, providing local and remote power management with outlet-level power metering and switching. An LCD screen provides local monitoring and alert indications, while remote access and configuration are obtainable through secure web, SNMP, CLI, or telnet interfaces.

Africa Data Center Power Industry Overview

The African data center power market is slightly consolidated among the players and has gained a competitive edge in recent years. A few major players in the market include Aggreko ZA, ABB Ltd, and Cummins Inc. These major players with a prominent market share focus on expanding their customer base across the region. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

- In April 2024, Vertiv, a significant provider of critical digital infrastructure and continuity solutions, introduced the extension of the Vertiv Liebert GXT5 lithium-ion double-conversion, online uninterruptible power supply (UPS) system for 5 kVA-10 kVA global voltage (GV) (200 V-240 V; default 230 V) applications.

- In January 2024, Caterpillar Inc. partnered with Microsoft and Ballard Power Systems to test the use of large-format hydrogen fuel cells as a reliable and eco-friendly backup power source for multi-megawatt data centers. Hydrogen fuel cells are seen as a possible low-carbon alternative to diesel backup generators, which is expected to drive the growth of DC generators.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Mega Data Centers and Cloud Computing

- 4.2.2 Increasing Demand to Reduce Operational Costs

- 4.3 Market Restraints

- 4.3.1 High Cost of Installation and Maintenance

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Power Infrastructure

- 5.1.1 Electrical Solution

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.3 Power Distribution Solutions

- 5.1.1.3.1 PDU

- 5.1.1.3.2 Switchgear

- 5.1.1.3.3 Critical Power Distribution

- 5.1.1.3.4 Transfer Switches

- 5.1.1.3.5 Remote Power Panels

- 5.1.1.3.6 Others

- 5.1.2 Service

- 5.1.1 Electrical Solution

- 5.2 End User

- 5.2.1 IT and Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media and Entertainment

- 5.2.5 Other End Users

- 5.3 Geography

- 5.3.1 South Africa

- 5.3.2 Nigeria

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ABB Ltd

- 6.1.2 Caterpillar Inc.

- 6.1.3 Cummins Inc.

- 6.1.4 Eaton Corporation

- 6.1.5 Legrand Group

- 6.1.6 Rolls-Royce PLC

- 6.1.7 Vertiv Group Corp.

- 6.1.8 Schneider Electric SE

- 6.1.9 Rittal GmbH & Co. KG

- 6.1.10 Fujitsu Limited

- 6.1.11 Cisco Systems Inc.