|

市場調査レポート

商品コード

1849989

農業用酵素:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Agricultural Enzymes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 農業用酵素:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月29日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

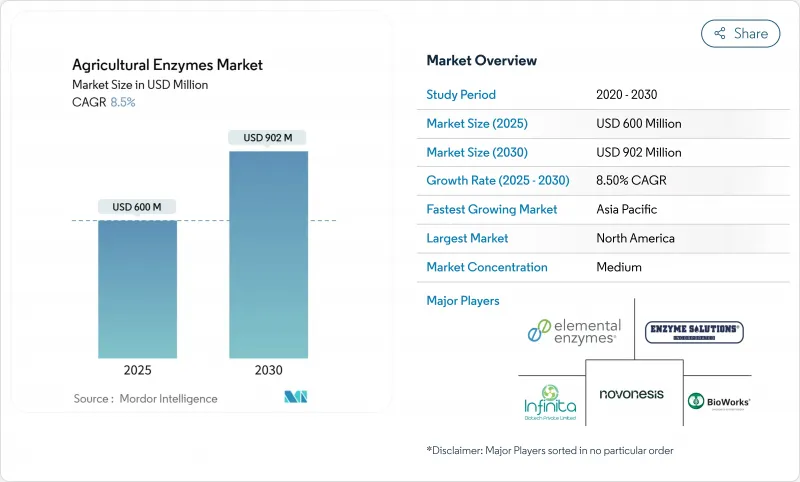

農業用酵素市場規模は2025年に6億米ドルと推定され、2030年には9億200万米ドルに達すると予測され、予測期間中のCAGRは8.5%です。

この成長は、合成化学物質に対する規制の強化、無残渣食品に対する消費者の欲求の高まり、酵素製剤および送達技術の着実な進歩を反映しています。成熟市場の商業生産者は、従来の投入資材の一部を酵素ベースの生物学的製剤に置き換えており、アジア太平洋地域の小規模農家は、対象を絞った補助金プログラムに支えられて、収量を高める生物学的製剤に移行しています。精密発酵とAI主導のタンパク質設計の並行的な開発により、製品開発サイクルが短縮され、長期的な炭素クレジット・プログラムにより、再生酵素ソリューションを展開する農家に新たな収入源がもたらされています。農薬メジャーは提携や買収を通じて生物学的ポートフォリオを強化し、専門バイオテクノロジー企業は次世代マルチ酵素カクテルの商品化を競うため、競合の激しさが増しています。

世界の農業用酵素市場の動向と洞察

有機食品と無残渣食品の需要

小売業者が残留基準値を厳格化し、EUのFarm to Fork戦略が2030年までに化学農薬の使用を50%削減することを義務付けているため、有機農産物への世界的な支出が増加しています。農家は認定オーガニック・チャネルで20~30%の価格プレミアムを得ており、化学残留物を使わずに栄養素を動員する酵素を採用する移行コストを相殺しています。酵素を組み込んだプログラムは、リンと窒素の利用可能性を高め、植物の防御経路を強化し、土壌マイクロバイオームのバランスを改善することで、有機システムにおける収量ギャップを埋めるのに役立ちます。スペインの商業果樹園経営者は、2024年にリン酸肥料からホスファターゼ・ウレアーゼ混合粒剤に切り替えた後、収量が9%増加したと報告し、明確な経済的利益を実証しました。同様の結果が、現在カナダ全土の温室栽培野菜での導入の原動力となっており、液体セルラーゼ混合肥料は、輪作間のバイオマス分解を改善することで作物サイクルを短縮しています。

生物投入物の導入急増

ブラジルは現在、耕作地の60%以上に生物学的作物保護ソリューションを適用しており、EUや米国の導入率を大幅に上回っています。合成除草剤や殺菌剤に対する耐性が高まり、新たな作用機序の探索が加速しており、農業用酵素は生物防除微生物と相乗効果を発揮する仲間として位置づけられています。マトグロッソ州の畑作農家は、リパーゼとマンナナーゼ酵素を含む種子処理カクテルを組み込んだ後、2024/25年シーズンにトウモロコシ対トウモロコシの収量を4.6%増加させました。インドでも同様の勢いがあり、州レベルの補助金制度が酵素投入コストの30%までをカバーしているため、零細農家への導入が促進され、2桁台の市場成長が加速しています。

断片的な規制当局の承認

生物学的製剤の開発企業は、EUでは製品分類に応じて複数の申請書を提出する必要があるなど、依然として承認までのスケジュールがまちまちです。米国の新しいバイオテクノロジー規制のための統一ウェブサイトは国内の透明性を向上させたが、世界的な調和はまだ遠いままです。遅延は平均的な商業化サイクルに18~24ヵ月を追加し、コンプライアンス・コストを膨れ上がらせ、一部の企業はより少ない価値の高い市場を優先するよう促しています。小規模なイノベーターが最も苦労しているのは、規制当局のサポートのために大手の農薬会社と提携することが多いため、独自の市場開拓戦略が制限されることです。

セグメント分析

ホスファターゼは、施肥量の80%に達する土壌の固定化リンを分解することで、2024年の農業用酵素市場の37%を占めました。肥料価格が不安定であるため、リンを固定化するソリューションに対する需要は穀物や油糧種子全体で堅調に推移しています。したがって、ホスファターゼの農業用酵素市場規模は、2030年まで支配的な収益ポジションを維持するものと思われます。セルラーゼは、CelOCEとその関連技術革新に後押しされ、CAGR13.8%で成長チャートのトップを占めています。これらの酵素は作物残渣を分解して糖を放出し、有益な微生物に燃料を供給して土壌構造を改善します。ウレアーゼ、リアーゼ、プロテアーゼがポートフォリオを構成し、複雑な圃場条件に適合するよう、補完的な活性を組み合わせたカクテル製品が増えています。

マルチ酵素ブレンドへのシフトは、高付加価値園芸において顕著であり、そこでは生産者は、一回の処理で正確な養分動員やストレス反応の強化を求めています。新興企業は、生産者が新鮮なセルラーゼリッチミックスを醸造できるようにする農場内発酵キットを開発しており、保存期間に関する懸念を回避し、コストを削減しています。大手企業は、ホスファターゼーウレアーゼの相乗効果を統合して窒素利用効率を改善し、水田での揮発を緩和しており、これは農業用酵素市場におけるソリューションセットの広がりを反映しています。

液体製品は、主に既存の散布装置との適合性と効率的な葉面吸収により、2024年の農業用酵素市場規模の46.2%を維持した。しかし、物流コストとコールドチェーン依存性により、製品管理者はより耐温度性の高い技術に舵を切っています。CAGR12.4%で前進している粒状製品は、現在では「バイオリアクター・イン・ア・グラニュール」構造を組み込んでおり、酵素を最大24ヵ月間安定させるとともに、土壌接触後の定時放出を可能にしています。

粉末製剤はコスト効率の良い中間領域を占めているが、専用の混合装置が必要です。ハイブリッド水分散性粒剤はこの境界線を曖昧にし、液体のような利便性と粒剤の耐久性を提供します。競合他社との差別化は、特にコールドチェーン格差が残るアジア太平洋やアフリカの熱帯地域で成長を追求する企業にとって、製剤の汎用性が決め手になると予想されます。

地域分析

2024年に農業用酵素市場の約35%を占める北米は、強固な流通インフラと生物学的投入物の迅速な規制クリアランスから利益を得ています。カナダの生産者は昨シーズンに1,180万ヘクタールの遺伝子組み換え作物を作付けし、補完的な酵素プログラムを受け入れる環境を作り出しました。米国のバイオスティミュラント分野も同様に活気に満ちており、酵素入り葉面散布剤がアーモンドやトマトの生産者の間で人気を集めています。

アジア太平洋は最も急速に成長している地域で、2030年までのCAGRは10%に達する見込みです。インドのバイオアグリ分野は2023年に124億米ドルに達し、国の補助金で酵素コストの30%まで賄えるようになったため、小規模農家での導入が加速しています。コールドチェーンのギャップは依然として重要なハードルであり、インドの酪農セクターでは必要な生産能力の80%がまだ不足しているため、メーカーは粒状製品を重視するようになっています。中国の土地譲渡改革は農場単位の大型化を促し、大規模に適用できる酵素技術のビジネスケースを改善します。

欧州は、グリーン・ディールの下での厳格な農薬削減目標のおかげで、強力な足場を維持しています。生物防除活性物質は2011年の120種類から2022年には220種類近くまで増加し、その間の売上は15億4,900万ユーロと倍増します。南米は、ブラジルの先駆的な60%の生物学的製剤の導入に牽引され、成熟しつつも拡大が続いており、特に大豆とトウモロコシの酵素強化種子処理がその分野です。中東とアフリカは、規制の明確化とコールドチェーンへの投資次第ではあるが、新たな可能性を示しており、南アフリカと湾岸諸国が早期導入の先陣を切っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 有機・無残留食品の需要

- 生物学的投入の採用急増

- 研究開発と製品イノベーションの強化

- 種子コーティングマイクロドーズデリバリー

- 再生型農業炭素クレジットプログラム

- 農場内酵素発酵ユニット

- 市場抑制要因

- 断片化された規制承認

- 土壌と気候によるパフォーマンスの変動

- 熱帯地域におけるコールドチェーンのギャップ

- 化学薬品に対する目に見えない短期ROI

- 規制情勢

- テクノロジーの展望

- ファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 酵素タイプ別

- ホスファターゼ

- 脱水素酵素

- ウレアーゼ

- プロテアーゼ

- リアーゼ

- セルラーゼ

- その他の酵素タイプ

- 剤形別

- 液体

- 粉

- 粒状

- 用途別

- 農作物保護

- 肥沃度の向上

- 植物の成長制御

- 適用モード別

- 種子処理

- 葉面散布剤

- 土壌処理

- 作物タイプ別

- 穀物

- 油糧種子と豆類

- 果物と野菜

- 芝生と観賞用植物

- その他の作物

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ケニア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Novonesis

- Elemental Enzymes

- Enzyme Solutions Inc.

- Bioworks Inc.

- Infinita Biotech Pvt. Ltd.

- Biocatalysts Ltd

- Enzyme Development Corporation