無菌包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1939003

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

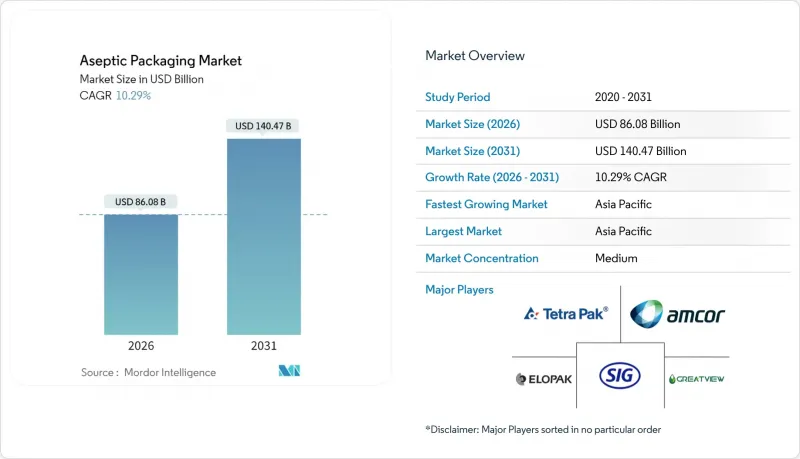

無菌包装市場は2025年に780億5,000万米ドルと評価され、2026年の860億8,000万米ドルから2031年までに1,404億7,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは10.29%と見込まれます。

保存性食品・飲料への需要拡大、食品安全規制の強化、コールドチェーンコスト削減の必要性により、無菌・常温流通フォーマットの魅力が高まっています。ブランドオーナーは、冷蔵インフラが未整備な地域において、即飲用(RTD)機能性飲料や保存性乳製品への需要増に対応するため、無菌ラインの拡充を進めています。同時に、バイオ医薬品製造や個別化治療の進展が、無菌包装市場における医薬品分野の収益基盤を拡大しています。アルミニウムフリーの高バリア性カートンやPFASフリーコーティングといった材料科学の革新により、メーカーは無菌性を損なうことなく新たな持続可能性要件への対応が可能となっています。コンバーターと樹脂メーカー間の統合は、変動の激しいポリマー市場における購買力を強化しています。一方、デジタル印刷技術は、増加するSKU(在庫管理単位)に適した、費用対効果の高い小ロット生産を可能にしています。

世界の無菌包装市場の動向と洞察

即飲機能性飲料の急成長

機能性RTD飲料には、微量栄養素、プロバイオティクス、植物成分を常温で最大12か月間封じ込める無菌ソリューションが求められています。各ブランドは、酸素・光・紫外線を遮断する高バリア性カートンや多層ボトルを採用し、コンビニエンスストアでのラストマイル配送を容易にしております。米国、中国、タイの飲料充填メーカーは、スポーツ栄養飲料、エナジードリンク、植物性プロテイン飲料の新製品投入に対応するため、時間当たり4万8,000本以上の処理能力を有する新型高速無菌ラインを導入しております。食品グレードの無菌性と医薬品グレードのバリデーションの境界が狭まりつつあることから、バイアル・アンプル供給業者はプレミアムなポジショニングを求める飲料顧客の獲得に注力しています。原料供給業者は、無菌加工による長期保存性により、保存料を減らし有効成分を増やすことが可能となり、クリーンラベル化と小売価格の上昇を支えると指摘しています。

新興アジアにおける常温保存乳製品の流通拡大

インド、ベトナム、インドネシアでは、管理が緩い冷蔵サプライチェーンから、無菌常温保存可能な牛乳やヨーグルトへの移行が急速に進んでいます。都市部の乳製品加工業者は、電力網の不安定さにより冷蔵コストが高騰する地方地域へ供給するため、UHT殺菌装置やブリックパック充填機に投資しています。中国では、2024年に常温保存飲料への再構成粉乳使用禁止が決定されたことを受け、純乳無菌ラインへの設備投資が相次ぎ、135℃の殺菌に耐えられる低酸性カートンラミネートの需要が高まっています。多国籍ブランドは、生乳の確保と農場近隣へのモジュール式無菌マイクロプラント導入を目的として、現地協同組合との合弁事業を展開しています。これにより、道路輸送コストの大幅削減と腐敗防止が実現しています。結果として、無菌包装市場はアジア新興国政府の長期的な食料安全保障政策において不可欠な要素となりつつあります。

多層ポリマー価格の変動性

ポリエチレンおよびポリプロピレンの価格は2024年に1ポンドあたり5セント上昇し、コンバーターの利益率を圧迫するとともに四半期ごとの追加料金の発生を促しました。ナフサやエタンといった原料市場の変動は、カートンの注ぎ口、キャップ、バリアフィルムの予算策定を複雑化させています。大規模な購入者は複数年契約による樹脂のヘッジを行いますが、小規模な充填業者はスポット価格の変動による痛手を被り、ホットフィルラインを無菌設備に置き換える資本プロジェクトが遅延しています。クラッカー複合施設の予期せぬ操業停止や輸送のボトルネックなど、世界の樹脂供給の構造的制約により、価格変動は当面続く見込みです。

セグメント分析

無菌包装市場において、カートンは乳製品、ジュース、RTDコーヒー分野での高い浸透率により、2025年売上高の63.30%を占めました。その長方形の形状はパレット効率と店頭陳列面積を最大化し、新たなストローレスキャップはプラスチック削減目標にも合致します。一方、バイアル・アンプルは、注射用バイオ医薬品、ワクチン、細胞療法の普及に伴い、2031年までCAGR12.98%で拡大しています。バイアル・アンプルの無菌包装市場規模は、人間用・動物用医薬品の両分野での採用を反映し、2031年までに109億4,000万米ドルに達すると予測されています。ボトルは、スムージーなどの高粘度飲料や、再封可能な大型フォーマットが消費の利便性を高めるフレーバーミルクにおいて、依然として重要な役割を担っています。缶は、高い耐穿刺性により、UHTココナッツウォーターや高酸性フルーツピューレといったニッチ市場で地位を確立していますが、アルミニウム価格の変動や、若い消費者が紙ベースの包装を好む傾向により、成長は抑制されています。パウチベースのバッグインボックスシステムは、コンパクトな輸送と開封後の長期保存性を求める外食産業事業者に支持されています。また、単回用スパウト付きパウチは、幼児向け飲料やスポーツ栄養ゼルの携帯性を提供します。

カーボンフットプリント削減の追求が製品レベルの革新を促進しています。SIG社が2025年に発売した、完全リサイクル可能でアルミニウム不使用の1リットルカートンは、常温保存で12ヶ月の賞味期限を維持し、欧州の主要乳製品ブランドから早期採用されました。一方、ガラスバイアルメーカーは、不活性接触面を維持しつつ重量を30%削減したポリマーオーバーガラス複合容器を開発し、世界のワクチンキャンペーンにおける輸送時の排出量削減に貢献しています。新素材の登場に伴い、バリア性能、リサイクル性、充填速度における製品レベルの差別化が、無菌包装市場における競争優位性を引き続き形作っていくでしょう。

地域別分析

アジア太平洋地域は2025年に売上高の38.05%を占め、中国、インド、インドネシアが牽引しました。インドの国家栄養プログラムは2027年までに包装牛乳の普及率を15%以上に引き上げる目標を掲げ、無菌包装能力への官民投資を促進しています。SIG社がグジャラート州に建設した9,000万ユーロの新規工場は、年間40億パックの生産能力を追加し、現地の乳製品および飲用ヨーグルト向けに供給されます。中国では、UHTカートンへの再構成粉乳充填を禁止する政策により、加工業者はより信頼性の高い製造業者へ移行を迫られており、価格規律の強化と利益率の向上が進んでいます。東南アジアの新興企業は、外出先での消費を捉えるため、250mLスリムカートン入りビタミン強化茶を発売しています。

南米は最も成長が著しい地域であり、2031年までCAGR14.02%で拡大が見込まれます。ブラジルではインフレ圧力により消費者が大容量・常温保存可能な商品を選択する傾向が強まり、2024年の包装食品市場規模は1,136億米ドルに達しました。ディーゼル燃料と電力コストの高騰により、内陸部物流センターへの投資は常温保存製品を優先しています。アルゼンチンの乳製品輸出業者は、冷蔵不要で乳糖フリーミルクをチリやペルーへ輸送するため、フレキシブルパウチラインを活用しています。北米と欧州では、数量拡大ではなく持続可能性を重視した素材転換により、1桁台半ばの成長が見込まれます。EUのPFAS禁止措置はシリコン酸化物ベースの紙容器バリア材の商業化を促進し、米国充填業者は労働力不足を補うため、高注意区域でのロボット導入を進めています。中東・アフリカ地域は規模こそ小さいもの、人口増加と政府の食料安全保障戦略に連動した長期的な成長余地を有しております。エジプトの工業地帯には、地域供給を目的としたUFlex社の2億米ドル規模ラミネートボード複合施設が立地しております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- RTD機能性飲料の急速な成長

- 新興アジア地域における常温乳製品の流通拡大

- 厳格な食品安全規制が滅菌包装の採用を促進

- インフレ連動によるコールドチェーンから常温物流への移行(報告不足)

- 持続可能で軽量な包装への移行が必須となる

- D2Cブランド向けデジタル印刷対応の短SKUの台頭(報告不足)

- 市場抑制要因

- 多層ポリマー価格の変動性

- 無菌充填ラインの高額な初期設備投資

- アルミ箔積層材のリサイクルインフラが限定的(報告不足)

- PFASバリアコーティングに関する規制の不確実性(報告不足)

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 価格分析

- 飲料用無菌包装- 需要洞察

第5章 市場規模と成長予測

- 製品別

- カートン

- ボトル

- 缶詰

- 袋およびパウチ

- バイアルおよびアンプル

- 素材組成別

- 紙および板紙

- プラスチック(ポリプロピレン、ポリエチレン、ポリエチレンテレフタレート)

- ガラス

- 金属(アルミニウム、鉄鋼)

- 複合積層材

- 用途別

- 飲料

- レディ・トゥ・ドリンク(RTD)飲料

- 乳製品ベースの飲料

- 食品

- 加工食品

- 果物と野菜

- 乳製品

- 医薬品

- パーソナルケア・化粧品

- 飲料

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Tetra Pak International SA

- SIG Combibloc Group

- Amcor PLC

- Elopak ASA

- IPI SRL(Coesia Group)

- DS Smith PLC

- Smurfit Kappa Group

- Mondi PLC

- Uflex Limited

- Schott AG

- Gerresheimer AG

- Toyo Seikan Group

- CDF Corporation

- BIBP Sp. z o.o.

- Nampak Ltd

- Greatview Aseptic Packaging

- Liqui-Box(Graphic Packaging)

- OPLATEK Group

- Sealed Air Corporation

- ProAmpac

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日