|

市場調査レポート

商品コード

1637758

北米の無菌包装:市場シェア分析、産業動向、成長予測(2025~2030年)North America Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の無菌包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

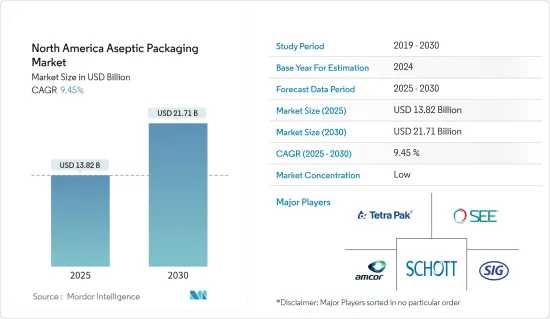

北米の無菌包装市場規模は2025年に138億2,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは9.45%で、2030年には217億1,000万米ドルに達すると予測されます。

同市場は、保存期間の延長や冷蔵を必要としない飲食品の保存に対するニーズの高まりによって、著しい成長を遂げています。さらに、製品の安全性と品質を強化する包装の技術的進歩は、市場を前進させる上で極めて重要な役割を果たしています。

主要ハイライト

- 長距離輸送の需要が急増するにつれ、賞味期限の延長が最重要課題となっています。製造現場とエンドユーザーとの距離が遠くなるにつれ、包装は耐久性と保護機能を強化しなければならないです。北米では、包装されたそのまま食べられる食事を好む傾向があり、無菌包装の採用を促進しています。

- 飲食品などのエンドユーザー産業は、サステイナブル包装と賞味期限の延長を優先しています。多くの地域の飲食品ベンダーは、特に常温出荷と保存のために、コストと環境の両方の利点を考慮し、無菌包装に傾いています。さらに、無菌包装はリサイクル可能なカートンや環境に優しいパウチを利用しています。こうした選択肢は、少量でより頻繁に購入することを好む消費者にアピールすることが多く、この地域におけるこうした製品に対する大きな需要を牽引しています。

- 消費者の健康志向は高まっています。消費者は、朝のジュースからエナジードリンクに至るまで、このウェルネス志向に沿った製品により積極的に投資しています。そのため、飲料包装セグメントでは費用対効果の高い包装ソリューションに対する需要が急増しています。さらに、特に牛乳・乳飲料セグメントで無菌カートンを好む傾向が強まっており、市場を活性化させると考えられます。これらのカートンは積み重ねを容易にし、製品の賞味期限を延ばします。

- 包装加工技術協会(PMMI)の飲料レポートによると、北米の飲料産業は2028年までに約4.5%拡大すると予測されています。この急成長する飲料市場は、研究市場の成長を促進する態勢を整えています。この地域の医薬品セグメント、特に米国では、無菌包装の需要が大幅に急増しています。この増加は主に、バイオテクノロジーによる医薬品の入手可能性と消費の増加、様々な液体医薬品の無菌充填ニーズによってもたらされています。

- 顧客の要求の高まりや保管・流通コストの抑制の必要性に対応するため、企業はセンサ、RFID、NFCのようなコネクテッド技術を活用し、先端技術への投資を行っています。これらの投資は、製造業者から小売業者までの製品管理に関連するコストを大幅に削減または排除することを目的としています。

- しかし、無菌包装市場にはいくつかの課題が立ちはだかっており、収益成長の妨げになる可能性があります。無菌包装の初期資本支出は、従来の生鮮食品製造方法よりも2~3倍高くなる可能性があります。さらに、無菌処理に特化した配合の微調整を可能にするため、最初から研究チームを参加させることが重要です。しかし、この必要性は、従来の方法と比較した場合、無菌包装のコストを大幅に上昇させる可能性があります。

北米の無菌包装市場の動向

飲料セグメントが大きな市場シェアを占める見込み

- 消費者がますます健康とウェルネスを優先するようになるにつれて、特に費用対効果の高い包装に重点を置いたフルーツベースのレディトゥドリンク飲料の需要が急増しています。この動向は予測期間中にさらに強まると予想されます。無菌包装はこれらの飲料の保存期間を延ばすだけでなく、保存可能なフルーツジュースのようなイノベーションも導入します。

- 利便性は、北米全域でレディトゥドリンク飲料や健康志向のカテゴリーで支配的な動向として台頭しています。自家製飲料には大掛かりな準備が必要なことから、消費者はレディトゥドリンクカクテルに引き寄せられます。このシフトは重要な傾向を浮き彫りにしています。消費者はこうしたカクテルのユニークな風味に惹かれ、家庭外で手軽に楽しめることに価値を感じているのです。

- 乳製品産業の世界の動向は、革新的な包装による製品の差別化を推し進めていることを明らかにしています。今日の乳製品包装は、人目を引くデザインと先進的な無菌機能を誇ることが多いです。このような包装革新の重視は、北米の主要市場における熾烈な競争への対応です。

- 超高温殺菌で処理された無菌牛乳は、有害な細菌を効果的に除去します。乳製品のカテゴリーは多様で、白乳やその製品別であるギー、バターミルク、ヨーグルトベースの飲料だけでなく、フレーバーミルクの有望な領域も含まれます。保存料を使わない無菌処理と包装は、牛乳のような生鮮食品にとって重要な保存期間と鮮度を大幅に向上させる。

- 無菌包装に対する乳産業の意欲の高まりは、より広範な動向を示唆しています。生乳生産量の増加に伴い、新たな世界的市場機会が視野に入ってきています。背景として、米国農務省は米国の牛乳生産量が2018年の2,176億ポンドから2024年には約2,282億ポンドに増加すると予測しています。さらに、消費者の顕著な変化として、保存期間が長いことで珍重されるUHT牛乳の需要が急増しており、消費者は来店回数を減らすことができます。さらに、パンデミックの影響により、従来のパック入り生乳やバルク牛乳よりもUHT牛乳の無菌包装が好まれる傾向が顕著になり、乳製品の消費パターンが大きく変化したことが浮き彫りになりました。

市場の成長が期待されるカナダ

- カナダの酪農セクターへの投資は続いており、国の経済を強化しています。地域の需要に応えるため、カナダ政府は先進包装技術、特に無菌包装の採用を推進しています。健康志向の高いミレニアル世代やカナダの若い世代は、過度のお菓子や炭酸ソーダ、人工甘味料のリスクに対する意識の高まりから、牛乳やジュース、エナジードリンクを好む傾向が強まっています。

- カナダでは、消費者がガラス瓶やプラスチックの代替品よりも牛乳パックを選ぶ傾向が強まっています。2024年5月にStatCanが発表したレポートによると、カナダの標準的な3.25%牛乳の生産量は2020年の約43万8,380キロリットルから2023年には46万8,070キロリットルに増加しました。乳製品をベースとする飲料セクターでは、腐敗しやすい品目には無菌液体包装が好まれます。乳製品の性質を考えると、これらの非常に腐りやすい液体食品や飲食品にとって、包装の品質は最も重要です。

- 無菌ソリューションプロバイダーは乳製品包装セグメントの課題に取り組んでいます。無菌包装を使用する製品の60%近くが乳製品で、これにはスプーンで食べるヨーグルト、チーズ、クリーム、アイスクリームなどが含まれます。乳製品の消費は天然チーズ、粉末チーズ、プロセスチーズと多岐にわたるが、腐敗性は依然として喫緊の課題です。無菌包装は、チーズの賞味期限を60日間も延ばすことができます。

- そのため、エンドユーザーは包装に多額の投資を行っています。乳製品は香りの移ろいや酸素暴露による分解に弱いため、包装には優れたバリア性が求められます。StatCanのデータから、カナダの乳製品売上高が顕著に増加していることが明らかになりました。2024年1月から5月までの月次メーカー売上高は、13億9,000万カナダドル(10億3,000万米ドル)から16億7,000万カナダドル(12億4,000万米ドル)に急増しました。

- さらに、無菌医薬品製造(しばしば充填仕上げ製造と呼ばれる)は、ワクチン、生物製剤、注射薬、がん治療、さまざまな形態の点耳・点鼻・点眼薬の製造において極めて重要です。この方法によって、医薬品が細菌やその他の有害物質で汚染されるリスクが大幅に軽減されます。カナダでは、製薬部門は国内で最も革新的な産業の一つとして際立っています。市販薬に加え、独創的なジェネリック医薬品を開発・製造する企業も含まれています。

北米の無菌包装産業概要

無菌包装はカートンや環境に優しいパウチを利用し、少量でより頻繁な購入を好む消費者に対応し、需要を牽引しています。さらに、消費者が防腐剤を使用しないオーガニック製品を求めるようになっているため、メーカーは鮮度を保ち賞味期限を延長する高級包装ソリューションに投資することで対応しています。

北米の無菌包装市場は、複数のベンダーが国内外市場に製品を供給しているため競合が激しいです。市場はセグメント化されており、大手企業は参入範囲を拡大し競合を維持するために様々な戦略を採用しています。市場の主要参入企業としては、Amcor Group、DS Smith Plc、Schott AGなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

第5章 市場力学

- 市場促進要因

- コールドチェーン物流のコスト削減に対する需要の高まり

- 製品の長期保存に対する需要の高まり

- 市場抑制要因

- 製造の複雑化と投資収益率の低下

第6章 市場セグメンテーション

- 製品タイプ

- プラスチックボトル

- プレフィラーシリンジ

- バイアルとアンプル

- バッグとパウチ

- カートン

- カップ

- ガラス瓶

- エンドユーザータイプ

- 医薬品

- 飲料

- フルーツ系

- 乳飲料

- レディトゥドリンク

- その他の飲料

- 食品

- フルーツベース

- 乳製品

- 加工食品

- ベビーフード

- スープ・ブロス

- その他の食品産業

- 国名

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Tetra Pak International S.A.

- Amcor Group

- Sealed Air Corporation

- SIG Combibloc Group

- WestRock Company

- Schott AG

- Scholle IPN

- DS Smith PLC

- Elopak AS

- Mondi PLC

第8章 投資分析

第9章 市場機会と今後の動向

The North America Aseptic Packaging Market size is estimated at USD 13.82 billion in 2025, and is expected to reach USD 21.71 billion by 2030, at a CAGR of 9.45% during the forecast period (2025-2030).

The market is witnessing significant growth, driven by the rising need for extended shelf life and the preservation of food and beverages without refrigeration. Furthermore, technological advancements in packaging that bolster product safety and quality play a pivotal role in propelling the market forward.

Key Highlights

- As demand for long-distance transportation surges, extending shelf life has become paramount. Packaging must enhance its durability and protective features with growing distances between manufacturing sites and end users. North America's penchant for packaged and ready-to-eat meals is driving the adoption of aseptic packaging.

- The end-user industries, such as food and beverage, prioritize sustainable packaging and extended shelf life. Many regional food and beverage vendors are leaning towards aseptic packaging, weighing both cost and environmental benefits, particularly for ambient shipping and storage. Furthermore, aseptic packaging utilizes recyclable cartons and eco-friendly pouches. These options often appeal to consumers favoring smaller quantities and more frequent purchases, driving significant demand for such products in the region.

- Consumer health and wellness consciousness is on the rise. They are willing to invest more in products that align with this wellness trend, from morning juices to energy drinks. Therefore, there's a surging demand for cost-effective packaging solutions in the beverage packaging segment. Furthermore, the growing preference for aseptic cartons, especially from the milk and dairy beverage sectors, is set to invigorate the market. These cartons facilitate easy stacking and extend the product's shelf life.

- As per the Beverage Report by the Association for Packaging and Processing Technologies (PMMI), North America's beverage industry is projected to expand by approximately 4.5% by 2028. This burgeoning beverage market is poised to propel the growth of the studied market. In the region's pharmaceutical sector, particularly in the United States, there's been a significant surge in demand for aseptic packaging. This uptick is primarily driven by the increasing availability and consumption of biotechnology-based drugs and various liquid pharmaceuticals' aseptic filling needs.

- In response to rising customer demands and the imperative to control storage and distribution costs, companies are leveraging connected technologies like sensors, RFID, and NFC and channeling investments into advanced technologies. These investments aim to substantially cut down or eliminate costs associated with managing products from manufacturers to retailers.

- However, several challenges loom over the aseptic packaging market, potentially hindering its revenue growth. The initial capital outlay for aseptic packaging can be two to three times higher than that of conventional fresh production methods. Furthermore, involving research teams from the beginning is crucial, enabling formula tweaks specific to aseptic processing. Yet, this necessity can significantly escalate the costs of aseptic packaging when posed with traditional methods.

North America Aseptic Packaging Market Trends

Beverages Segment is Expected to Hold a Significant Market Share

- As consumers increasingly prioritize health and wellness, the demand for fruit-based ready-to-drink beverages is surging, especially with a focus on cost-effective packaging. This trend is expected to intensify over the forecast period. Aseptic packaging not only extends the shelf life of these beverages but also introduces innovations like shelf-stable fruit juices.

- Convenience is emerging as a dominant trend in ready-to-drink beverages and health-focused categories across North America. Given the extensive preparation required for homemade beverages, consumers gravitate towards ready-to-drink cocktails. This shift highlights a significant trend: consumers are drawn to the unique flavors of these cocktails and value the ease of enjoying them outside the home.

- Global trends in the dairy industry reveal a push towards product differentiation through innovative packaging. Today's dairy product packaging often boasts eye-catching designs and advanced aseptic features. This emphasis on packaging innovation is a response to fierce competition in key North American markets.

- Aseptic milk, treated with ultra-high-temperature pasteurization, effectively eliminates harmful bacteria. The dairy category is diverse, encompassing not just white milk and its byproducts like ghee, buttermilk, and yogurt-based beverages but also the promising realm of flavored milk. Aseptic processing and packaging, free from preservatives, significantly enhance shelf life and freshness-vital attributes for perishable items like milk.

- The dairy industry's growing appetite for aseptic packaging signals a broader trend. With rising milk production, new global market opportunities are on the horizon. For context, the USDA projects U.S. cow milk production to increase from 217,600 million pounds in 2018 to approximately 228,200 million in 2024. Additionally, a notable consumer shift has been the surging demand for UHT milk, prized for its extended shelf life, allowing consumers to reduce store visits. Furthermore, with the effect pandemic, there was a marked preference for the sterile packaging of UHT milk over traditional packaged fresh and bulk milk, underscoring a significant evolution in dairy consumption patterns.

Canada is Expected to Witness Growth in the Market

- Investments continue to flow into the Canadian dairy sector, bolstering the nation's economy. Responding to regional demands, the Canadian government is championing the adoption of advanced packaging technologies, particularly aseptic packaging. Health-conscious millennials and the younger generation in Canada increasingly gravitate towards milk, juices, and energy drinks, driven by a heightened awareness of the risks of excessive sweets, carbonated sodas, and artificial sugars.

- In Canada, consumers are increasingly opting for milk cartons over glass bottles and plastic alternatives, driven by eco-friendly concerns and the cost-effectiveness of cartons. A report from StatCan in May 2024 highlighted that Canada's production of standard 3.25% milk rose from about 438.38 thousand kiloliters in 2020 to 468.07 thousand kiloliters in 2023. Aseptic liquid packaging is preferred for perishable items in the dairy-based beverages sector. Given the nature of dairy products, the quality of packaging is paramount for these highly perishable liquid foods and beverages.

- Aseptic solution providers are addressing challenges in the dairy packaging arena. Nearly 60% of products using aseptic packaging are dairy items, including spoonable yogurt, cheese, cream, and ice cream. Dairy consumption spans natural, powdered, and processed cheese, but perishability remains a pressing concern. Aseptic packaging can extend cheese's shelf life by an impressive 60 days.

- Consequently, end users are channeling substantial investments into packaging. Given dairy's vulnerability to fragrance transfer and decomposition from oxygen exposure, packaging must boast superior barrier qualities. Data from StatCan reveals a notable uptick in Canada's dairy product sales: from January to May 2024, monthly manufacturer sales surged from CAD 1.39 billion (USD 1.03 billion) to CAD 1.67 billion (USD 1.24 billion).

- Further, aseptic pharmaceutical manufacturing, often termed fill-finish manufacturing, is crucial in producing vaccines, biologics, injectable drugs, cancer treatments, and various forms of ear, nasal, and eye drops. This method significantly reduces the risk of contaminating medications with germs or other harmful substances. In Canada, the pharmaceutical sector stands out as one of the nation's most innovative industries. It encompasses companies developing and producing creative and generic medicines alongside over-the-counter drug products.

North America Aseptic Packaging Industry Overview

Aseptic packaging utilizes cartons and eco-friendly pouches and caters to consumers who favor smaller, more frequent purchases, driving demand. Furthermore, as consumers increasingly seek organic products without preservatives, manufacturers are responding by investing in premium packaging solutions that preserve freshness and extend shelf life.

The North America Aseptic Packaging Market is competitive owing to the presence of multiple vendors in the market supplying their products in domestic and international markets. The market appears fragmented, with major players adopting various strategies to expand their reach and stay competitive. Some of the major players in the market are Amcor Group, DS Smith Plc, Schott AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness- Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand to Reduce the Cost of Cold Chain Logistics

- 5.1.2 Increasing Demand for the Longer Shelf Life of Products

- 5.2 Market Restraint

- 5.2.1 Manufacturing Complications and Lower Return on Investments

6 MARKET SEGMENTATION

- 6.1 Product Type

- 6.1.1 Plastic Bottles

- 6.1.2 Prefillabe Syringes

- 6.1.3 Vials and Ampoules

- 6.1.4 Bags and Pouches

- 6.1.5 Cartons

- 6.1.6 Cups

- 6.1.7 Glass Bottles

- 6.2 End- User Type

- 6.2.1 Pharmaceutical

- 6.2.2 Beverage

- 6.2.2.1 Fruit-based

- 6.2.2.2 Milk and Other Dairy Beverages

- 6.2.2.3 Ready-to-Drink

- 6.2.2.4 Other Beverage Industry Types

- 6.2.3 Food

- 6.2.3.1 Fruit-based

- 6.2.3.2 Dairy Food

- 6.2.3.3 Processed Foods

- 6.2.3.4 Baby Foods

- 6.2.3.5 Soups and Broths

- 6.2.3.6 Other Food Industry Types

- 6.3 Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tetra Pak International S.A.

- 7.1.2 Amcor Group

- 7.1.3 Sealed Air Corporation

- 7.1.4 SIG Combibloc Group

- 7.1.5 WestRock Company

- 7.1.6 Schott AG

- 7.1.7 Scholle IPN

- 7.1.8 DS Smith PLC

- 7.1.9 Elopak AS

- 7.1.10 Mondi PLC