|

市場調査レポート

商品コード

1637849

中東・アフリカのアセプティック包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Middle East And Africa Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカのアセプティック包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 102 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

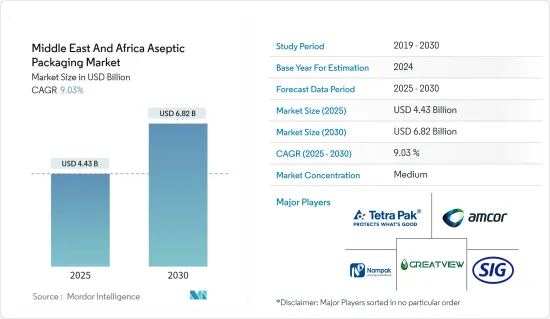

中東・アフリカのアセプティック包装市場規模は2025年に44億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは9.03%で、2030年には68億2,000万米ドルに達すると予測されます。

主なハイライト

- アセプティック包装市場の主な成長促進要因は、一貫した高い製品品質と栄養保持に対する要求を満たす包装材料の能力です。また、缶ライナーなど他の包装タイプで頻繁に見られるビスフェノールA(BPA)の論争を回避する能力もあります。アセプティック包装は、これらの要件をすべて満たし、冷蔵なしで推定6~12ヶ月間賞味期限を延長する製品もあります。

- 急速な都市化と消費財の多様化は、アセプティック包装の開発を促進する主な要因です。加工食品や使い捨て医療用品に対する需要の高まりも、同地域におけるアセプティック包装の採用を後押ししています。

- 人々のライフスタイルの変化は、家庭料理から調理済み製品へのシフトをもたらしました。こうしたライフスタイルの変化と、それに伴う消費者の加工食品、包装食品、調理済み食品への依存が、無菌カートン包装ソリューションへの需要を高めています。スーパーマーケット文化の出現もまた、買い物の風景を変え、特に飲食品において包装の必要性を高めています。

- アセプティック包装は製品に保存料を添加する必要性を減らし、自然で保存料無添加の製品に注目する消費者の間で注目を集めています。また、アセプティック包装は出荷・流通時に冷蔵されたよりリラックスした環境を必要としないため、出荷・流通コストの削減にも役立ちます。

- 地域のアセプティック包装市場は初期段階にあります。しかし、健康や製品の賞味期限に関する懸念の高まりは、同地域の成長に影響を与える主な要因のひとつです。

中東・アフリカのアセプティック包装市場の動向

製品の賞味期限を延ばすためのアセプティックカートン包装の採用増加

- 消費者は賞味期限が長く、より効率的に使用できる製品を求めています。このため、企業は従来の包装に代わる包装ソリューションを考案する必要に迫られています。高度な低温貯蔵チェーンに依存することなく製品の提供を拡大しようとする企業にとって、より長い賞味期限を提供するパッケージの製造は極めて重要になっています。

- 酸素、湿気、微生物などの潜在的な劣化要因から製品を保護することで、賞味期限を延ばすことができます。企業は、同じことを達成するために、費用対効果の高いパッケージング・ソリューションを必要としています。食品サプライチェーン全体の無駄を削減することは、農業が環境に与える影響を軽減し、増大する食品需要に対応するために極めて重要な活動であろう。効率的で低コストの持続可能な加工・包装ソリューションに投資して製品の保存期間を延ばすことは実行可能な解決策であり、アセプティックカートン包装の需要を高めています。

- 食品包装はもはや、食品を保護し販売するための受動的な役割だけではなくなっています。保存料を減らすことが重視されていることもアセプティック包装の促進要因です。無菌食品保存法により、カートンを開封するまで保存料なしで加工食品を長く保存することができるからです。

- アフリカの富の増大が食生活の進化につながることから、酪農産業は繁栄すると予想されます。IFCN酪農研究ネットワークは、2030年までに摂取量が3分の1以上増加すると推定しており、その需要に対応するため、チーズとバターの輸入量は2倍以上になると見込まれています。さらに、ユニリーバ、ネスレ、ディアジオといった世界的大企業はいずれも、急増する人口、中産階級の増加、ラゴス、カイロ、ヨハネスブルグといった都市における都市化の進展に乗じようと、アフリカ全域で大規模な事業を展開しています。

- 統計総局によると、サウジアラビアの飲食品サービス市場の2020年の売上は約144億6,000万米ドルだった。この金額は2025年には約1,603万米ドルに達すると予想されています。この成長は、無菌カートン包装にプラスの影響を与えることができるパッケージ食品や飲料の消費の潜在的急増を示しています。

医薬品・医療セグメントは予測期間中に著しい成長が見込まれる

- プレフィラブルシリンジは、利便性、価格、正確性、無菌性、安全性の欠如といった非経口ドラッグデリバリーの欠点を克服しています。これらのシリンジは、糖尿病や関節リウマチなどの慢性疾患の容易な管理を可能にし、それによって予測期間中に自動注射器やペン型注射器の使用を増加させる。中東・アフリカでは糖尿病やその他の慢性疾患の有病率が高まっており、予測期間中の市場需要につながると予想されます。

- プレフィルドシリンジは、製薬業界がより便利で新しいドラッグデリバリー方法を模索する中で、単位用量投薬の選択肢の一つとして急成長しています。また、製薬会社は薬剤の廃棄を最小限に抑え、製品寿命を延ばし、患者は病院ではなく自宅で注射薬を自己投与できます。

- バイアルやアンプルは、様々な薬剤の組み合わせに適していることから、約80%がガラス製ですが、剥離や破損などの課題に直面しています。サイクルオレフィンポリマー(COP)やサイクルオレフィンコポリマー(COC)のような代替プラスチックバイアルは、今後5年間で大きな市場シェアを獲得すると予想されます。Schott AGやAmcor Group GmbHなどの大手企業は、医薬品用途のCOCに関する専門知識を有しています。このような開発は、この地域におけるアセプティック包装のニーズを促進しています。

- さらに、中東・北アフリカの国際糖尿病連合によると、2021年には約7,300万人(20~79歳)が糖尿病を患っており、2045年には1億3,600万人の成人が糖尿病を患うと予測されています。アフリカでは2021年から2045年の間に、20歳から79歳の糖尿病患者が134%増加すると予測されています。同時に、中東とアフリカでは87%の急増が予測されています。このように、インスリン産業の成長はプレフィラブルシリンジ市場を牽引し、アセプティック包装市場の開拓をさらに後押しすると予想されます。

中東・アフリカのアセプティック包装産業の概観

中東・アフリカのアセプティック包装市場は半固体化しており、国内外のベンダーが数社参入しています。市場の主なプレーヤーには、Tetra Pak International SA、Amcor Group GmbH、SIG Group AG、Mondi PLC、Nampak Ltd、Greatview Aseptic Packaging Company、International Aseptic Paperboard Mfg LLCなどがあります。各プレイヤーは、製品革新、合併、買収など様々な戦略を採用し、主にリーチを拡大し競争力を維持しています。

- 2023年11月、アセプティック包装のシステムとソリューションの大手プロバイダーであるSIGグループAGは、アラブ首長国連邦のF&Bリーダーや新興企業向けに充填機を発売すると発表しました。SIG SmileSmall 24 AsepticとSIG CleanPouch 25 Aseptic充填機は、ドバイ・シリコンオアシスにあるSIGのテクノロジーセンターでご利用いただけます。これらの充填機は、製品テストやイノベーション、性能、容量の柔軟性、SIGのDrinksplus機能など、F&Bイノベーターにさまざまな利点と可能性を提供します。

- 2023年11月、テトラパック・インターナショナルSAは、食品メーカーのラクトガルと共同で、紙ベースのバリアを含むアセプティックカートン「Tetra Brik 200 Slim Leaf」を発売しました。パッケージングにおける再生可能コンテンツの使用を90%に高めるため、このカートンは約80%の板紙から作られています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- 地政学的シナリオが業界に与える影響の評価

第5章 市場力学

- 市場促進要因

- コールドチェーン物流のコスト削減要求の高まり

- 製品の長期保存に対するニーズの急増

- 市場の課題

- 環境問題とリサイクルへの懸念

- 製造の複雑化(原材料コストの上昇など)とROIの低下

第6章 市場セグメンテーション

- 包装材料別

- 金属

- ガラス

- 紙・板紙

- プラスチック

- その他の包装材料

- 包装タイプ別

- カートン

- 袋・パウチ

- カップとトレイ

- ボトルと瓶

- 缶

- その他の包装タイプ

- エンドユーザー産業別

- 食品

- 飲料

- 医薬品・医療

- その他のエンドユーザー産業

- 国別

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第7章 競合情勢

- 企業プロファイル

- Tetra Pak International SA

- Amcor Group GmbH

- Nampak Ltd

- DS Smith PLC

- SIG Group AG

- Uflex Limited

- Mondi PLC

- Greatview Aseptic Packaging Company

- International Aseptic Paperboard Mfg. LLC

- Smurfit Kappa Group PLC

第8章 投資分析

第9章 市場の将来

The Middle East And Africa Aseptic Packaging Market size is estimated at USD 4.43 billion in 2025, and is expected to reach USD 6.82 billion by 2030, at a CAGR of 9.03% during the forecast period (2025-2030).

Key Highlights

- The main growth drivers in the aseptic packaging market are the packaging material's ability to meet the demands for high, consistent product quality and nutrient retention. Also, the capacity to avoid the bisphenol A (BPA) controversy is frequently found in other packaging types, such as can liners. Aseptic packaging has met all these requirements and extends the shelf life of some products by an estimated six to twelve months without refrigeration.

- Rapid urbanization and the variety of consumer goods are key factors promoting the development of aseptic packaging. The rising demand for processed foods and disposable medical supplies also drives the adoption of aseptic packaging in the region.

- The altering lifestyles of people have resulted in the shift from home-cooked to ready-to-eat products. These lifestyle changes and consumers' consequent dependence on processed, packaged, and pre-cooked food are increasing the demand for aseptic carton packaging solutions. The advent of supermarket culture has also altered the shopping landscape and increased the need for packaging, especially in food and beverage products.

- Aseptic packaging reduces the need to add preservatives to the product, which is gaining attention among consumers who are focusing on natural and no-preservative products. Also, aseptic packaging helps reduce shipping and distribution costs by eliminating the need for refrigerated, more relaxed environments during shipping and distribution.

- The regional aseptic packaging market is in its early stages. However, increasing concerns regarding health and product shelf life are some of the major factors affecting its growth in the region.

Middle East And Africa Aseptic Packaging Market Trends

Increasing Adoption of Aseptic Carton Packaging to Increase the Shelf-life of Products

- Consumers have been demanding products with a longer shelf life and more efficient usage. This has necessitated the companies to devise alternative packaging solutions to traditional packaging. With companies seeking to expand their product offerings with less dependence on sophisticated cold storage chains, producing packages that provide longer shelf life has become crucial.

- Protecting products from potential deteriorating agents, such as oxygen, moisture, and microbes, can increase shelf life. Companies need a cost-effective packaging solution to achieve the same. Reducing wastage throughout the food supply chain is likely a crucial activity to reduce the environmental impact of agriculture and serve the increasing food demand. Investing in efficient, low-cost, and sustainable processing and packaging solutions to increase product shelf life is a viable solution, thus increasing the demand for aseptic carton packaging.

- Food packaging is no longer just a passive role in protecting and marketing a food product. The emphasis on decreasing preservatives is also a driving factor for aseptic packaging, as aseptic food preservation methods enable processed food to be kept longer without preservatives until the carton is opened.

- The dairy industry is expected to prosper as Africa's growing wealth translates to evolving diets. The IFCN Dairy Research Network estimates intake will increase by more than a third by 2030, in which time imports of cheese and butter are expected to more than double to meet that demand. Furthermore, global giants like Unilever, Nestle, and Diageo are all running massive operations across Africa as they seek to capitalize on surging population growth, a rising middle class, and increasing urbanization in cities such as Lagos, Cairo, and Johannesburg.

- According to the General Authority for Statistics, the revenue of the food and beverage service activities market in Saudi Arabia was worth about USD 14.46 billion in 2020. This amount is anticipated to reach around USD 16.03 million in 2025. This growth indicates a potential surge in the consumption of packaged foods and beverages, which can positively impact aseptic carton packaging.

The Pharmaceutical and Medical Segment is Expected to Witness Significant Growth During the Forecast Period

- Prefillable syringes overcome the disadvantages of parenteral drug delivery, such as lack of convenience, affordability, accuracy, sterility, and safety. These syringes enable easy management of chronic diseases, such as diabetes and rheumatoid arthritis, thereby increasing the use of auto-injectors and pen injectors over the forecast period. The growing prevalence of diabetes and other chronic diseases in the Middle East and Africa is expected to lead to market demand over the forecast period.

- Prefilled syringes are emerging as one of the fastest-growing choices for unit-dose medication as the pharmaceutical industry seeks new and more convenient drug delivery methods. Also, pharmaceutical companies minimize drug waste and increase product life span, while patients can self-administer injectable drugs in their homes instead of the hospital.

- Around 80% of the vials and ampoules are made from glass, owing to their suitability with varied drug combinations, but they face challenges like delamination, breakage, etc. Alternative plastic vials, like cycle olefin polymer (COP) and cycle olefin copolymer (COC) formats, are expected to gain significant market share over the next five years. Major players such as Schott AG and Amcor Group GmbH possess expertise in COC for pharmaceutical applications. Such developments are driving the need for aseptic packaging in the region.

- Furthermore, according to the International Diabetes Federation in the Middle East and North Africa, in 2021, around 73 million people (20-79) had diabetes, and it is projected that 136 million adults will have diabetes by 2045. People with diabetes are expected to grow by 134% in Africa among those aged 20 to 79 between 2021 and 2045. At the same time, there is projected to be an 87% surge across the Middle East and Africa. Thus, the growing insulin industry is expected to drive the prefillable syringes market, which would further aid the development of the aseptic packaging market.

Middle East And Africa Aseptic Packaging Industry Overview

The Middle East and Africa aseptic packaging market is semi-consolidated, as a few domestic and international vendors operate in the market. Some of the major players in the market include Tetra Pak International SA, Amcor Group GmbH, SIG Group AG, Mondi PLC, Nampak Ltd, Greatview Aseptic Packaging Company, and International Aseptic Paperboard Mfg LLC. Players are adopting various strategies, such as product innovation, mergers, and acquisitions, primarily to expand their reach and stay competitive.

- In November 2023, SIG Group AG, a leading systems and solutions provider for aseptic packaging, announced the launch of filling machines for F&B leaders and startups in the United Arab Emirates. The SIG SmileSmall 24 Aseptic and SIG CleanPouch 25 Aseptic filling machines are available in SIG's Technology Center at Dubai Silicon Oasis. They offer F&B innovators various benefits and possibilities for product testing and innovation, performance, volume flexibility, and SIG's Drinksplus capability.

- In November 2023, Tetra Pak International SA launched the Tetra Brik 200 Slim Leaf aseptic carton, which contains paper-based barriers, in collaboration with food products producer Lactogal. To increase the use of renewable content in the packaging to 90%, the carton is made from approximately 80% paperboard.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

- 4.5 Assessment of the Geopolitical Scenario's Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand to Reduce Cost of Cold Chain Logistics

- 5.1.2 Surge in Need for Longer Shelf Life of Products

- 5.2 Market Challenges

- 5.2.1 Concerns over Environment Problems and Recycling

- 5.2.2 Manufacturing Complications (For Example Increasing Cost of Raw Materials) and Lower ROI

6 MARKET SEGMENTATION

- 6.1 By Packaging Material

- 6.1.1 Metal

- 6.1.2 Glass

- 6.1.3 Paper & Paperboard

- 6.1.4 Plastics

- 6.1.5 Other Packaging Material

- 6.2 By Packaging Type

- 6.2.1 Cartons

- 6.2.2 Bags and Pouches

- 6.2.3 Cups and Trays

- 6.2.4 Bottles and Jars

- 6.2.5 Cans

- 6.2.6 Other Packaging Type

- 6.3 By End-User Industry

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Pharmaceutical and Medical

- 6.3.4 Other End-User Industries

- 6.4 By Country

- 6.4.1 Saudi Arabia

- 6.4.2 South Africa

- 6.4.3 United Arab Emirates

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tetra Pak International SA

- 7.1.2 Amcor Group GmbH

- 7.1.3 Nampak Ltd

- 7.1.4 DS Smith PLC

- 7.1.5 SIG Group AG

- 7.1.6 Uflex Limited

- 7.1.7 Mondi PLC

- 7.1.8 Greatview Aseptic Packaging Company

- 7.1.9 International Aseptic Paperboard Mfg. LLC

- 7.1.10 Smurfit Kappa Group PLC