|

市場調査レポート

商品コード

1693991

米国のキャットフード:市場シェア分析、産業動向、成長予測(2025~2030年)US Cat Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のキャットフード:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 269 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

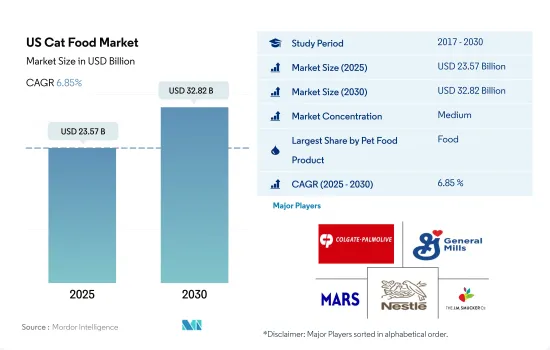

米国のキャットフード市場規模は2025年に235億7,000万米ドルと推定され、2030年には328億2,000万米ドルに達し、市場推定・予測期間(2025~2030年)のCAGRは6.85%で成長すると予測されています。

特定の健康ニーズと特定のソリューションを求めるペットの親が、国内における猫用動物用飼料の利用を促進しています。

- 2022年、キャットフードは米国ペットフード市場の29%を占め、2017年と比較して69%増加しました。この成長は主に猫の飼育数増加とペットオーナーの増加に起因します。例えば、2022年には、猫の飼育数は2017年と比較して11%増加しました。ペットフードは米国のキャットフード市場で最大のセグメントであり、2022年の市場規模は138億6,000万米ドルです。ウェットペットフードは猫の消費量が多く、2022年には75億米ドルと評価されました。

- トリーツは米国のキャットフード市場で2番目に大きいセグメントで、2022年の市場規模は21億7,000万米ドルでした。スナックは、消化を助けたり皮膚や被毛の健康を促進したりといったその他の特典を与えるために、通常のフードに加えて猫に与えられます。

- 2022年には、動物用飼料セグメントは21億4,000万米ドルと評価されました。このセグメントは最も急成長しており、予測期間中にCAGR 8.0%を記録すると予想されています。猫の動物用飼料セグメントでは、尿路疾患サブセグメントが最も高い市場シェアを占めています。2022年の市場規模は4億9,380万米ドルでした。猫の健康状態の有病率の増加がこのセグメントの成長に寄与しました。

- 米国のキャットフード市場における猫用栄養補助食品の市場規模は5億1,550万米ドルで、2017~2022年にかけて3.1%増加しました。この増加は、特に猫に関する健康への懸念の高まりにより、健康的な食生活への意識が高まったことによる。

- キャットフード市場は、猫の飼育数の増加、猫特有の健康ニーズ、ペットオーナーの健康意識の高まりにより、今後も成長が見込まれます。予測期間中のCAGRは7.3%と予測されます。

米国のキャットフード市場動向

ミレニアル世代の間でコンパニオンペットとして猫を求める人が増えていることが、同国における猫の飼育数の伸びにつながっています。

- 米国の猫の飼育数は増加しています。コンパニオンペットとしての需要が高く、他のペットよりもペットフードへの支出が少ないことから、同国では猫のペット化が進んでいます。同国では、ペットのヒューマニゼーションが進み、また、猫は犬よりも居住面積を必要としないため、ペットとしての猫のシェアは2017~2022年の間に10.8%増加しました。例えば米国では、2020年には26%の世帯が猫をペットとして飼っていたが、2022年には53.5%に増加しました。

- 米国では、在宅勤務の文化があるため、ペットとして猫を飼う割合が高く、同伴者の需要が高まり、ミレニアル世代がペットを飼うようになりました。例えば、2022年には米国ではミレニアル世代がペットを飼う人の33%を占め、2020年には猫の飼育数の40%が動物保護施設から飼われるようになりました。2020年には、米国の高所得に伴い、ペット保護者の43%がペットショップから猫を購入しています。したがって、2020~2022年にかけて、同国のペットとしての猫は4.5%増加しました。

- 猫を家族の一員として扱う猫の親は、2017~2018年にかけて猫の飼い主の76%を占めました。これは、ペットの親が栄養価の高い専門的なペットフードをペットに与えたいと考えているため、ペットフードを含むペット用品の成長に役立つと予想されます。また、人々は愛する人に猫を贈与しており、2021年には米国における猫の飼い主の3%を占めます。

- 猫の養子縁組や購入の増加、ペットの人間化の進展といった要因が、ペット数の増加を後押しすると予想されます。ペット数の増加は、同国のペットフード市場の成長を促進すると予想されます。

さまざまなチャネルを通じて市販のペットフードを入手できるようになり、プレミアム化が進んでいることが、ペットの親による支出の増加につながっています。

- 米国では、ペットの飼い主の猫への支出は2019~2022年にかけて一貫して約23.7%増加しました。この支出の増加傾向は、ペットの猫の所有率の増加、キャットフードの選択肢の多様化、プレミアム化の動向など様々な要因によるものです。国内のペット飼育世帯数は、2020年の8,490万世帯から2022年には8,690万世帯に増加します。

- 米国でペットを飼うのにかかる費用といえば、猫の飼い主は通常、犬の飼い主よりも少ないです。平均すると、猫1匹あたりの年間支出は犬1匹あたりの年間支出より12.2%低いです。これは、犬の方が猫よりも多くの餌を必要とするため、犬の餌代が多くなるためです。さらに、2022年時点で犬の飼育頭数は9,240万頭、猫の飼育頭数は6,470万頭で、犬の飼育頭数より猫の飼育頭数の方が42.8%少ないです。

- 米国では、ペットの飼い主は犬に年間平均1,480米ドル、猫に年間902米ドルを費やしています。これらの費用には、フード、スナック、獣医の診察、グルーミングなど、さまざまなアイテムやサービスが含まれます。特に、ペットフードとスナックはこれらの支出の約40%を占めています。米国の飼い主は通常、スーパーマーケット、ペットショップ、オンラインショップでペットフードを購入します。特にパンデミック(世界的大流行)時には、ペットフードのオンライン販売が大幅に増加しました。2022年には、ペットフードのオンライン販売は、ペットフード販売全体の18.0%を占めました。この動向に拍車をかけたのは、高品質のペットフードの利点に対する意識の高まりと、ペットフードのプレミアム化の進展です。この動向は今後も同国のペット支出を促進すると予想されます。

米国のキャットフード産業概要

米国のキャットフード市場は適度に統合されており、上位5社で53.95%を占めています。この市場の主要企業は、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、General Mills Inc.、Mars Incorporated、Nestle(Purina)、The J. M. Smucker Companyです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブ製品別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブ製品別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

- The J. M. Smucker Company

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The US Cat Food Market size is estimated at 23.57 billion USD in 2025, and is expected to reach 32.82 billion USD by 2030, growing at a CAGR of 6.85% during the forecast period (2025-2030).

Specific health needs and pet parents seeking specific solutions are driving the usage of veterinary diets for cats in the country

- In 2022, cat food accounted for 29% of the US pet food market, with a 69% increase compared to 2017. This growth can be primarily attributed to the rising cat population and the increasing number of pet owners. For instance, in 2022, the cat population grew by 11% compared to 2017. Pet food is the largest segment in the US cat food market, valued at USD 13.86 billion in 2022. Wet pet food is highly consumed by cats and was valued at USD 7.50 billion in 2022.

- Treats comprise the second-largest segment in the US cat food market, valued at USD 2.17 billion in 2022. Treats are given to cats in addition to regular food to provide additional health benefits, such as aiding digestion and promoting healthy skin and coat.

- In 2022, the veterinary diets segment was valued at USD 2.14 billion. It is the fastest-growing segment, expected to register a CAGR of 8.0% during the forecast period. The urinary tract diseases sub-segment holds the highest market share in the cat veterinary diet segment. It was valued at USD 493.8 million in 2022. The increasing prevalence of health conditions in cats contributed to the growth of the segment.

- Nutraceuticals for cats were valued at USD 515.5 million in the US cat food market, with a 3.1% increase between 2017 and 2022. This increase was driven by the increased awareness of healthy diets, particularly due to growing health concerns regarding cats.

- The market for cat food is expected to continue growing due to the increasing cat population, their specific health needs, and greater health awareness among pet owners. It is projected to register a CAGR of 7.3% during the forecast period.

US Cat Food Market Trends

The increase in the number of people seeking cats as companion pets among millennials is leading to the growth of cat adoption in the country

- The cat population in the United States is increasing. Cats as pets are being adopted in the country due to the high demand for companionship and less expenditure on pet food than other pets. In the country, the share of cats as pets increased by 10.8% between 2017 and 2022 due to a rise in pet humanization and because cats require less area to live than dogs. For instance, in the United States, 26% of households owned a cat as a pet in 2020, which increased to 53.5% in 2022.

- The United States witnessed higher adoption of cats as pets during the pandemic because of the work-from-home culture, leading to a demand for companionship and a higher number of millennials becoming pet owners. For instance, in 2022, millennials comprised 33% of pet parents in the United States, and in 2020, 40% of the cat population was adopted from animal shelters. In 2020, 43% of pet parents purchased cats from pet stores in line with high incomes in the United States. Therefore, cats as pets in the country increased by 4.5% between 2020 and 2022.

- Cat parents treating their cats as a part of their family accounted for 76% of cat owners between 2017 and 2018. This is expected to help in the growth of pet products, including pet food, as pet parents want to provide their pets with nutritious, specialized pet food. People also gifted cats to their loved ones, accounting for 3% of cat owners in the United States in 2021.

- Factors such as an increase in the adoption and purchase of cats and an increase in pet humanization are expected to boost the growth of the pet population. The increase in pet population is expected to drive the growth of the pet food market in the country.

The availability of commercial pet food through different channels and rising premiumization are leading to an increase in expenditure by pet parents

- In the United States, pet owners' spending on cats increased consistently by about 23.7% between 2019 and 2022. This upward trend in expenditure is attributed to various factors, including the growing ownership of pet cats, the greater diversity of cat food options, and the trend toward premiumization. The number of households in the country with pets rose from 84.9 million in 2020 to 86.9 million in 2022.

- When it comes to the cost of pet ownership in the United States, cat owners typically spend less than dog owners. On average, the yearly expenditure per cat is 12.2% lower than the yearly expenditure per dog. This is because dogs require more food than cats, leading to more spending on food for dogs. Furthermore, the population of dogs in the country is higher than that of cats, with 92.4 million pet dogs and 64.7 million pet cats as of 2022, representing a 42.8% lower population of cats compared to dogs.

- In the United States, pet owners spend an average of USD 1,480 annually on dogs and USD 902 annually on cats. These expenses cover various items and services, such as food, treats, vet visits, and grooming. Notably, pet food and treats account for about 40% of these expenditures. Pet owners in the United States typically purchase pet food from supermarkets, pet stores, and online retailers. There was a significant increase in online pet food sales, particularly during the pandemic. In 2022, online pet food sales accounted for 18.0% of total pet food sales. This trend was fueled by the rising awareness of the benefits of high-quality pet food and the growing premiumization of pet food. It is expected that this trend will continue to drive pet expenditure in the country.

US Cat Food Industry Overview

The US Cat Food Market is moderately consolidated, with the top five companies occupying 53.95%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 General Mills Inc.

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 PLB International

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 The J. M. Smucker Company

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms