アジア太平洋のキャットフード:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Cat Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 320 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693973

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

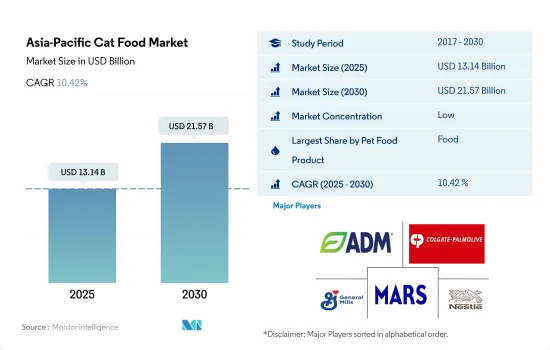

アジア太平洋のキャットフード市場規模は2025年に131億4,000万米ドルと推定され、2030年には215億7,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは10.42%で成長する見込みです。

ペット用スナックが最も急成長しているセグメントであり、愛猫の飼育数の増加がアジア太平洋のキャットフード市場を牽引している

- アジア太平洋のキャットフード市場は上昇傾向にあります。猫は、犬よりも飼育スペースや世話の手間がかからないペットを求めるペットオーナーの間で人気があります。2022年には、アジア太平洋のペットフード市場の34.0%を猫が占め、キャットフード市場は2017~2021年の間に50.3%増加しました。この増加は主に同地域のペット猫の飼育数の増加に起因しており、2017年の1億360万匹から2022年には1億3,320万匹に増加しました。同地域ではペットの人間化が進んでおり、ペットの飼い主がペットを家族の一員と考えていることから、プレミアムキャットフード製品の需要が高まりました。

- 食品とペット用スナックは、2022年にそれぞれ68億6,000万米ドルと16億9,000万米ドルを占める主要セグメントでした。これらのセグメントのシェアが高いのは、猫に定期的な食事を与え、しつけや娯楽の目的で重要な役割を果たしているためです。猫用スナックは、予測期間中にCAGR 12.4%を記録し、最も急成長するセグメントと予想されます。

- フード製品セグメントでは、ウェットフードは水分と肉の含有量が高く、猫の自然な食事と栄養要件に合致しているため、猫に好まれる選択肢として浮上しています。そのため2022年には、アジア太平洋のフード製品セグメントでウェットフードが53.5%を占めています。

- ペット用動物用飼料とペット用栄養補助食品は合計で、2022年の市場全体の14.2%を占めました。これらの製品は、ペットのさまざまな健康状態に的を絞った栄養補給やサポートを提供するために特別に設計されています。

- 猫の飼育数の増加と市販のペットフード製品が提供する様々な利点が、予測期間中の市場を牽引すると予想されます。

中国と日本がアジア太平洋の主要なキャットフード市場であり、猫の飼育数が多く、ペットの人間化が進んでいることがその要因です。

- 2022年、アジア太平洋は世界のキャットフード市場において最大市場のひとつに浮上し、その市場規模は約99億7,000万米ドルでした。中国と日本は、これらの国々で猫の飼育率が高いことから、アジア太平洋のキャットフード市場に大きく貢献しています。キャットフードセグメントは2017~2022年にかけて69.9%成長したが、これは猫の飼育率の増加、猫の健康に対する意識の高まり、この地域におけるペットの人間化の動向の高まりが要因です。

- 中国がアジア太平洋のキャットフード製品市場を独占し、2022年には35億8,000万米ドルに達します。これは主に、2022年に7,850万人に達する同国の巨大な猫ペット数によるものです。中国の可処分所得の増加、人口統計パターンの変化、消費者の嗜好の進化が、市場の存在感を高めています。

- 日本はアジア太平洋で最大の猫好き国のひとつです。猫はペットの主要な選択肢であり、2022年には日本のペット数の43.6%を占めます。このような猫の飼育数の多さが、同国におけるキャットフード製品セグメントの成長に寄与しており、2022年の市場規模は21億4,000万米ドルに達しました。

- インドネシアは最も急成長している猫市場で、インドネシアのキャットフード市場は予測期間中にCAGR 18.8%を記録すると予測されています。同国では、他のペットに比べて猫の維持費が安く、費用対効果が高いため、ペットとしての人気が高まっています。例えば、同国の猫の飼育数は2017~2022年の間に137.6%増加しました。

- 猫の飼育数の増加、可処分所得の増加、猫の健康に対する意識の高まりが、予測期間中のアジア太平洋のキャットフード市場の成長を促進すると推定されます。

アジア太平洋のキャットフード市場動向

同地域では、ペットカフェやペットショップといった新たな購入エコシステムが発展しており、多種多様なキャットフード製品やサービスを通じて、購入から動物の世話までを支援することで、猫の飼育数を増加させています。

- アジア太平洋では、猫は犬に比べシェアが低く、2022年にはペット数の26.1%を占めます。中国、インド、オーストラリアなどの国々では、リラックスしてストレスが少なくなるといった健康上の利点や、ペットを伴侶と考えることから、ペットの飼育が増加しています。そのため、ペットとしての猫の飼育数は2017~2022年の間に0.28%増加しました。

- インドネシアやマレーシアなどの国では、猫の親は犬の親よりも高いです。インドネシアとマレーシアでは、2021年にはそれぞれ47%と34%を占めているが、これはこれらの国の宗教文化のためであり、彼らは犬よりも猫をペットとして飼うことを好みます。このため、これらの国ではドッグフードよりもキャットフードに投資する企業が増えると考えられます。中国では、都市部における猫を含むペットの数が増加しており、猫を含むペット数は2018~2020年にかけて10.2%増加し、2020年には都市部におけるペット数は1億80万人に達します。さらに、パンデミック時の同伴者の増加により、猫の飼育数は2020年の7,440万匹から2022年には8,250万匹に増加。また、猫の寿命は20年以上であるため、長期的な影響もあると考えられます。

- ペットカフェやペットショップが、多種多様なペットフード製品やサービスを通じて、購入から動物の世話までサポートしているため、この地域ではペットの採用と購入の新しいエコシステムが発展しています。例えばベトナムでは、ザ・ニャー・ハウス・バイ・アール・ハウスがベジタリアンやヴィーガン向けの食事を提供する猫カフェであり、猫の家となっています。健康上の利点による猫飼育の増加、アジア太平洋の文化、ペット生態系の変化といった要因が、この地域における猫飼育の促進に役立っています。

プレミアム化の進展、予防医療への需要の高まり、幅広いキャットフード製品の入手可能性が猫のペット支出を促進しています。

- 同地域の猫への支出は過去期間に増加し、2017~2022年の間に24.2%増加しました。支出の増加は、さまざまな種類のペットフードが入手可能になったこと、プレミアム化が進んだこと、猫の幸福のためのサービス需要が伸びたことによる。また、ペットの親はペットの健康を心配しており、猫の健康を維持するための予防措置として、カスタマイズ型獣医食を提供しています。

- アジア太平洋では、ペットの親が良質で高級なペットフードを好むため、ペットの支出が増加しています。例えば、香港のキャットフード市場では、2022年にプレミアムペットフード部門がペットフード売上高の75%を占めました。日本、シンガポール、台湾などの他の国々では、香港のペットの親が猫を含むペットのために支出する額の約50~60%を売上が占めており、2022年の支出額は台湾の1人当たり60米ドルに対し、香港は1人当たり約140米ドルでした。したがって、香港でのプレミアム化の拡大は、予測期間中に地域の他の国々でのプレミアム化を促進すると予想されます。

- 猫の飼い主を含む多くのペットの親は、ペットショップやコンビニエンスストアなどの他のチャネルと比較して、ウェブサイト上の商品数が多く、ペットフードの注文が簡単であることから、専用のペットフードをオンラインで購入します。例えば、2019年、中国のオンラインチャネルによるペットフードの売上は、ペットショップチャネルの売上貢献が21%であったのに比べ、57%でした。したがって、ペットフードに対する一人当たりの支出が高く、ペット数の増加に伴いプレミアム化が進んでいることから、予測期間中、この地域の猫に対するペット支出は増加すると予想されます。

アジア太平洋のキャットフード産業概要

アジア太平洋のキャットフード市場はセグメント化されており、上位5社で14.45%を占めています。この市場の主要企業は、ADM、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、General Mills Inc.、Mars Incorporated、Nestle(Purina)です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブプロダクト別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブプロダクト別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブプロダクト別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブプロダクト別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- 台湾

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Affinity Petcare SA

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- IB Group(Drools Pet Food Pvt. Ltd.)

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The Asia-Pacific Cat Food Market size is estimated at 13.14 billion USD in 2025, and is expected to reach 21.57 billion USD by 2030, growing at a CAGR of 10.42% during the forecast period (2025-2030).

Pet treats are the fastest-growing segment, and the increasing pet cat population is driving the Asia-Pacific cat food market

- The Asia-Pacific cat food market has experienced an upward trend. Cats are popular among pet owners seeking low-maintenance pets that require less space and attention than dogs. In 2022, cats accounted for 34.0% of the pet food market in Asia-Pacific, and the cat food market increased by 50.3% between 2017 and 2021. This increase was mainly attributed to the increasing pet cat population in the region, which increased from 103.6 million in 2017 to 133.2 million in 2022. The increasing pet humanization in the region boosted the demand for premium cat food products, as pet owners consider their pets as family members.

- Food products and pet treats were the major segments that accounted for USD 6.86 billion and USD 1.69 billion in 2022, respectively. The higher share of these segments was because of their significance in providing regular dietary requirements for cats and for training and entertainment purposes. Cat treats are anticipated to be the fastest-growing segment, recording a CAGR of 12.4% during the forecast period.

- In the food product segment, wet food has emerged as the preferred choice for cats due to its high moisture and meat content, which aligns with their natural diet and nutritional requirements. Therefore, in 2022, wet food accounted for 53.5% of the food product segment in Asia-Pacific.

- Pet veterinary diets and pet nutraceuticals collectively accounted for 14.2% of the total market in 2022. These products are specifically designed to provide targeted nutrition or support for various health conditions in pets.

- The increasing cat population and the various benefits offered by commercial pet food products are anticipated to drive the market during the forecast period.

China and Japan are the major cat food markets in Asia-Pacific, driven by the large cat population and the growing pet humanization

- In 2022, Asia-Pacific emerged as one of the largest markets in the global cat food market, with a value of around USD 9.97 billion. China and Japan are major contributors to the cat food market in Asia-Pacific due to the high cat ownership rates in these countries. The cat food segment grew by 69.9% between 2017 and 2022, driven by the increasing adoption of cats, the growing awareness of cat health, and the rising trend of pet humanization in the region.

- China dominates the Asia-Pacific cat food products market, reaching a value of USD 3.58 billion in 2022. This was mainly due to the country's huge pet cat population, which reached 78.5 million in 2022. China's growing disposable income, changing demographic patterns, and evolving consumer preferences have contributed to its strong market presence.

- Japan is one of the biggest cat-loving countries in Asia-Pacific. Cats are the primary choice of pets, accounting for 43.6% of the country's pet population in 2022. This significant cat population has contributed to the growth of the cat food product segment in the country, which reached a market value of USD 2.14 billion in 2022.

- Indonesia is the fastest-growing market for cats, with the Indonesian cat food market projected to register a CAGR of 18.8% during the forecast period. Cats are gaining popularity as pets due to their low maintenance and cost-effectiveness compared to other pets in the country. For instance, the cat population in the country increased by 137.6% between 2017 and 2022.

- The growing cat population, increase in disposable income, and growing awareness of cat health are estimated to fuel the growth of the Asia-Pacific cat food market during the forecast period.

Asia-Pacific Cat Food Market Trends

A new purchase ecosystem is evolving in the region, such as pet cafes and pet stores, providing assistance from purchasing to taking care of the animals through a wide variety of cat food products and services driving population of cats

- In Asia-Pacific, cats have a lower share compared to dogs, and they accounted for 26.1% of the pet population in 2022. Countries such as China, India, and Australia have witnessed an increase in pet ownership due to health benefits such as feeling relaxed and less stressed and considering them as their companions. Therefore, the cat population as a pet increased by 0.28% between 2017 and 2022.

- Cat parents are higher than dog parents in countries such as Indonesia and Malaysia. In Indonesia and Malaysia, it accounted for 47% and 34%, respectively, in 2021 because of the religious culture of these countries, and they prefer to adopt cats as pets than dogs. This will help the companies to invest more in cat food in these countries than dog food. In China, there has been an increase in the number of pets, including cats, in urban areas, and the pet population, including cats, increased by 10.2% between 2018 and 2020 to reach a pet population of 100.8 million in urban areas in 2020. Moreover, the cat population increased from 74.4 million in 2020 to 82.5 million in 2022 because of a rise in companionship during the pandemic. Also, it will have long-term effects as the life span of cats is more than 20 years.

- A new pet adoption and purchase ecosystem is evolving in the region as there are pet cafes and pet stores providing assistance from purchasing to taking care of the animals through a wide variety of pet food products and services. For instance, in Vietnam, The Meow House by R House is a cat cafe that serves vegetarian and vegan food and is a home for cats. Factors such as the rise in the adoption of cats due to health benefits, the culture of the Asia-Pacific, and changes in the pet ecosystem help in enhancing cat adoption in the region.

Growing premiumization, the increasing demand for preventive care, and the availability of a wide range of cat food products are driving pet cat expenditure

- The expenditure on cats in the region increased during the historical period, and it increased by 24.2% between 2017 and 2022. The increased expenditure was because of the availability of different types of pet food, the rise in premiumization, and a growth in demand for services for the cat's well-being. Pet parents are also concerned about their pet's health and are providing customized veterinary diets as a preventive measure to keep the cat healthy.

- In Asia-Pacific, there has been a rise in pet expenditure because pet parents prefer good quality, premium pet food as they are willing to pay premium prices. For instance, in Hong Kong's cat food market, the premium pet food segment accounted for 75% of the pet food sales in 2022. In other countries such as Japan, Singapore, and Taiwan, sales accounted for about 50%-60% of the pet parents' spending in Hong Kong for pets, including cats; the expenditure was about USD 140 per capita compared to Taiwan's per capita of USD 60 in 2022. Therefore, growing premiumization in Hong Kong is expected to boost premiumization in other countries of the region during the forecast period.

- A higher number of pet parents, including cat owners, purchase specialized pet food online compared to other channels, such as pet stores and convenience stores, because of the high number of products on the website and the ease of ordering pet food. For instance, in 2019, China's pet food sales from online channels were 57% compared to pet store channels, which contributed 21% to the sales. Therefore, the higher per capita spending on pet food and growing premiumization with the increase in the pet population are expected to boost pet expenditure on cats in the region during the forecast period.

Asia-Pacific Cat Food Industry Overview

The Asia-Pacific Cat Food Market is fragmented, with the top five companies occupying 14.45%. The major players in this market are ADM, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated and Nestle (Purina) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Philippines

- 5.3.8 Taiwan

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Affinity Petcare SA

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 General Mills Inc.

- 6.4.6 IB Group (Drools Pet Food Pvt. Ltd.)

- 6.4.7 Mars Incorporated

- 6.4.8 Nestle (Purina)

- 6.4.9 PLB International

- 6.4.10 Schell & Kampeter Inc. (Diamond Pet Foods)

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 320 Pages

- 納期

- 2~3営業日