北米のキャットフード:市場シェア分析、産業動向、成長予測(2025~2030年)

North America Cat Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 297 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693978

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

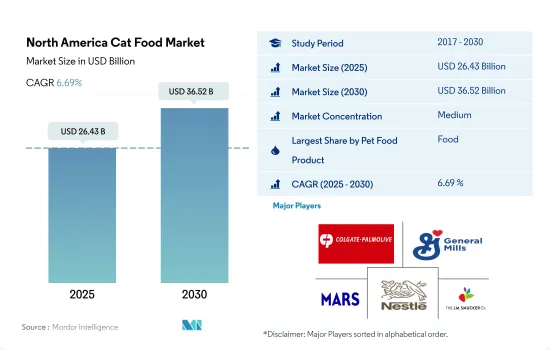

北米のキャットフード市場規模は2025年に264億3,000万米ドルと推定・予測され、2030年には365億2,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは6.69%で成長すると予測されています。

強力な流通網と幅広いキャットフードブランドが市場を牽引

- 北米のキャットフード市場規模は2022年に211億4,000万米ドルに達し、世界最大のキャットフード市場となりました。これは、猫の飼育数が多く、飼い主が猫に多額の支出をしているためです。

- 北米ではペットフードが最大の市場シェアを占め、2022年の市場規模は155億7,000万米ドルでした。ペットフードのうち、ウェットフードは2022年の金額シェアで52.5%と大半を占め、ドライフードは47.5%でした。ペットフードのシェアが大きいのは、ペットフードの複数の利点と、主流ブランドとニッチブランドの両方でドライフードとウェットフードの幅広い選択肢が利用可能であることが、この地域の猫用ペットフード市場全体の成長を牽引しているためと考えられます。

- スナックセグメントは北米のキャットフード市場で2番目に大きいセグメントであり、2022年の市場規模は25億6,000万米ドルでした。猫用スナックの中では、フリーズドライスナックとカリカリスナックが主要セグメントで、2022年の金額シェアはそれぞれ24.9%と22.3%です。これらのスナックには様々な原料が使用され、ビタミン、ミネラル、その他のサプリメントが添加されていることが、キャットフード市場におけるこのセグメントの成長を促進すると推定されます。

- 動物用飼料セグメントは、キャットフード市場で最も急速に成長しているセグメントです。2017~2022年の間に81.8%の伸びを示し、2022年には24億2,000万米ドルに達します。予防医療としての動物用飼料の利用が増加していることが、予測期間中にCAGR 9.1%の速さでこのセグメントを牽引すると推定されます。

- 様々な流通チャネルを通じて様々な形態のペットフードが入手可能になりつつあることが、予測期間中のキャットフード市場の成長を促進すると推定されます。

米国は2022年に88%以上のシェアを占め、この地域のキャットフード市場を独占しました。

- 北米は、2022年のキャットフードの世界市場で最大のシェアを占め、その金額は約211億4,000万米ドルでした。米国とカナダは北米のキャットフード市場に大きく貢献しており、これらの国ではペットの飼育率が高いため、ペットフード製品に対する需要が高いです。

- 北米のキャットフード市場は米国が支配しており、2022年の市場規模は186億9,000万米ドルでした。この背景には、2022年には6,460万頭を超えると推定される同国の猫ペット数の多さなど、いくつかの要因があります。さらに、同国の高い生活水準と可処分所得も一役買っており、ペットの飼い主は予算の多くを猫のフードやケア用品に充てることができます。

- カナダのキャットフード市場は、犬に比べて猫の飼育数が増加しているため、大きな成長を遂げています。猫の飼育数は2017~2022年の間に1.7%増加し、合計820万人に達しました。その結果、カナダのキャットフード市場規模は2022年に16億6,000万米ドルに達し、同年のカナダのペットフード市場規模の36.7%を占めます。

- キャットフード市場はメキシコと北米以外の国々で急成長を遂げており、予測期間中のCAGRはそれぞれ7.2%と9.9%を記録すると予測されています。これは、これらの国々で猫の飼育数が増加していることに起因しています。例えば、北米以外の地域では、猫の飼育数は2017~2022年の間に23.4%増加し、2022年には合計1,670万人に達します。

- 猫の飼育数の増加とペットフードを与えることの利点に関する意識の高まりが、予測期間中の市場を牽引すると推定されます。

北米のキャットフード市場動向

若年層とミレニアル世代からの導入増加がキャットフード市場を牽引

- 北米ではペットとしての猫の飼育が増加しているが、これは同伴者としての需要が高く、犬よりも猫のペットフードへの支出が少ないためです。同地域では、ペットの人間化が進んでいること、また、猫は犬よりも飼育面積が少なくて済むことから、ペットとしての猫は2017~2022年にかけて13.6%増加しました。例えば米国では、猫をペットとして飼っている世帯は2020年には26%だったが、2022年には53.5%に増加しました。

- 米国、カナダ、メキシコでは、在宅勤務の文化が同伴者の需要につながり、ペットを飼う人の多くがミレニアル世代であることから、流行期にペットとしての猫の採用が増加しました。例えば、2022年には、米国ではミレニアル世代がペットの親の33%を占め、2020年には、猫のペット数の40%が国内の動物保護施設から引き取られました。さらに、ペットの親は高収入のため、ペットショップから猫を購入しました。例えば、2020年には、米国の猫の親の43%がペットショップから猫を購入しています。したがって、この地域のペットとしての猫は2020~2022年の間に5.34%増加しました。

- 同地域では成猫よりも若い猫が多く飼われており、その数では米国がリードしています。例えば、2021年の米国の猫の飼育数は684,144頭で、若い猫が53.5%を占めています。若い猫の飼育数が増え、ミレニアル世代がペットの親となることで、予測期間中のペットフード製品の成長に貢献すると予想されます。猫の養子縁組と購入の増加、ペットの人間化の増加がペット数の増加に貢献すると予想されます。ペット数の増加は、同地域のペットフード市場の成長に寄与するであると考えられます。

プレミアムキャットフード製品に対する需要の高まりが市場を牽引する

- 北米ではペットの支出が増加しています。ペットの支出が増加しているのは、さまざまな種類のペットフードが入手可能になったことと、米国とカナダでペットフード製品のプレミアム化が進んでいるためです。北米では、猫の飼い主はペットに高級ペットフードを与えることを好み、エコフレンドリーペットケア製品を採用することを望んでいます。例えば、2022年には、50%以上のペットの親が、プレミアム価格を支払うことで、猫を含むペットにエコフレンドリーペットケア製品を与えたいと考えており、猫の飼い主の42%が猫にプレミアムペットフードを与えています。

- ペットの親の出費が最も多いのはペットフードとスナックで、予測期間中に増加すると予測されています。例えば、キャットフードとスナックは、2022年に猫にかかった費用の22.7%を占めています。このシェアは、ペットを家族の一員として扱うペットペアレントが増え、専用ペットフードに対する認識が高まるにつれて増加すると予測されます。この地域ではミレニアル世代のペットペアレンツが多いため、猫の親は猫に自然なペットフードやスナックを与えたいと考えています。

- また、ペット保険、グルーミング、社会化のためのしつけといったサービスにも投資しています。緊急の獣医療は非常に高額になるため、ペットの親は猫に保険をかけています。これは、米国で猫の親を含むペットの親が2020年にペット保険に20億米ドル(前年比27.5%増)を投資したことからも明らかです。

- 保険料化と高品質フードの利点に関する意識の高まりが、この地域におけるペット支出の増加に役立つと予想される要因です。

北米のキャットフード産業概要

北米のキャットフード市場は適度に統合されており、上位5社で55.47%を占めています。この市場の主要企業は、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、General Mills Inc.、Mars Incorporated、Nestle(Purina)、The J. M. Smucker Companyです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブ製品別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブ製品別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

- The J. M. Smucker Company

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The North America Cat Food Market size is estimated at 26.43 billion USD in 2025, and is expected to reach 36.52 billion USD by 2030, growing at a CAGR of 6.69% during the forecast period (2025-2030).

The availability of a strong distribution network and a wide range of cat food brands is driving the market

- In North America, the value of the cat food market reached USD 21.14 billion in 2022, making it the largest market for cat food in the world. This is due to the substantial cat population and the significant spending on cats by their owners.

- In North America, pet food held the largest market share, with a market value of USD 15.57 billion in 2022. Among pet food, wet food represented the majority share of 52.5% by value in 2022, while dry food accounted for 47.5%. The large share of pet food can be attributed to the multiple benefits of pet food and the availability of a wide range of dry and wet food choices in both mainstream and niche brands, which is driving the overall growth of the pet food market for cats in the region.

- The treats segment is the second-largest segment in the cat food market in North America; it was valued at USD 2.56 billion in 2022. Among cat treats, freeze-dried and crunchy treats are the primary segments, accounting for major shares of 24.9% and 22.3% by value, respectively, in 2022. The use of various ingredients and the presence of added vitamins, minerals, and other supplements in these treats are estimated to drive the growth of this segment in the cat food market.

- The veterinary diets segment is the fastest-growing segment in the cat food market. It witnessed an 81.8% increase between 2017 and 2022, reaching USD 2.42 billion in 2022. The increasing usage of veterinary diets as preventative care is estimated to drive the segment at a faster CAGR of 9.1% during the forecast period.

- The growing availability of various forms of pet food through different distribution channels is estimated to drive the growth of the cat food market during the forecast period.

The United States dominated the cat food market in the region with more than an 88% share in 2022

- North America accounted for the largest share of the global cat food market in 2022, with a value of around USD 21.14 billion. The United States and Canada are the major contributors to the cat food market in North America, with a high demand for pet food products due to the high pet ownership rates in these countries.

- The North American cat food market is dominated by the United States, which accounted for a market value of USD 18.69 billion in 2022. This can be attributed to several factors, including the large population of pet cats in the country, which was estimated to be over 64.6 million in 2022. Additionally, the country's high standard of living and disposable income also play a role, allowing pet owners to allocate a greater portion of their budget toward their cats' food and care products.

- The cat food market in Canada is experiencing significant growth due to the growing population of cats compared to dogs in the country. The cat population grew by 1.7% between 2017 and 2022, reaching a total of 8.2 million. As a result, the Canadian cat food market reached a value of USD 1.66 billion in 2022, representing 36.7% of the Canadian pet food market value in the same year.

- The cat food market is experiencing rapid growth in Mexico and countries in the Rest of North America, which are projected to record CAGRs of 7.2% and 9.9%, respectively, during the forecast period. This can be attributed to the growing cat population in these countries. For instance, in the Rest of North America, the cat population increased by 23.4% between 2017 and 2022, reaching a total of 16.7 million in 2022.

- The growing cat population and the increasing awareness about the benefits of feeding pet foods are estimated to drive the market during the forecast period.

North America Cat Food Market Trends

Increasing adoptions from young adults and millennials are driving the cat food market

- There is an increase in the adoption of cats as pets in North America, owing to the high demand for companionship and less expenditure on pet food for cats than dogs. In the region, cats as pets increased by 13.6% between 2017 and 2022 due to the rise in pet humanization and because cats require less area to live than dogs. For instance, in the United States, households owning a cat as a pet was 26% in 2020, which increased to 53.5% in 2022.

- The United States, Canada, and Mexico witnessed higher adoption of cats as pets during the pandemic because of the work-from-home culture leading to a demand for companionship and a higher number of pet owners being millennials. For instance, in 2022, millennials were 33% of pet parents in the United States, and in 2020, 40% of the cat pet population was adopted from animal shelters in the country. Additionally, pet parents purchased cats from pet stores due to high income. For instance, in 2020, 43% of cat parents in the United States purchased cats from pet stores. Therefore, cats as pets in the region increased by 5.34% between 2020 and 2022.

- Young cats are being adopted more than adult cats in the region, with the United States leading in terms of that number. For instance, in 2021, the adopted cat population in the United States was 684,144, and young cats accounted for 53.5% of the cats adopted. The higher population of young cats and millennials being pet parents is expected to help in the growth of pet food products during the forecast period. An increase in the adoption and purchase of cats and an increase in pet humanization are expected to help in the growth of the pet population. The increasing pet population will help in the growth of the pet food market in the region.

The surging demand for premium cat food products is driving the market

- Pet expenditure is increasing in North America. The rise in pet expenditure is due to the availability of different types of pet food and the growing premiumization of pet food products in the United States and Canada. In North America, cat owners prefer to provide their pets with premium pet food and are willing to adopt eco-friendly pet care products. For instance, in 2022, more than 50% of pet parents were willing to provide their pets, including cats, with eco-friendly pet care products by paying a premium price; 42% of cat owners provided cats with premium pet food.

- The highest expenses of pet parents are on pet food and treats, which are estimated to increase during the forecast period. For instance, cat food and snacks accounted for 22.7% of expenses incurred for cats in the United States in 2022. The share is projected to increase as more pet parents treat their pets as family members and the awareness about specialized pet food increases. Cat parents are willing to provide their cats with natural pet food and treats as a high number of millennials are pet parents in the region.

- Pet parents are also investing in other services such as pet insurance, pet grooming, and pet training for socialization. Pet parents are getting their cats insured as emergency veterinary care can be very expensive. This is evident as pet parents, including cat parents, in the United States invested USD 2 billion in pet insurance in 2020, an increase of 27.5% from the previous year; 17% of the cat population was insured in 2020.

- Premiumization and rising awareness about the benefits of quality food are factors anticipated to help in increasing pet expenditure in the region.

North America Cat Food Industry Overview

The North America Cat Food Market is moderately consolidated, with the top five companies occupying 55.47%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 General Mills Inc.

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 PLB International

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 The J. M. Smucker Company

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 297 Pages

- 納期

- 2~3営業日