南米のキャットフード:市場シェア分析、産業動向、成長予測(2025~2030年)

South America Cat Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 280 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693985

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

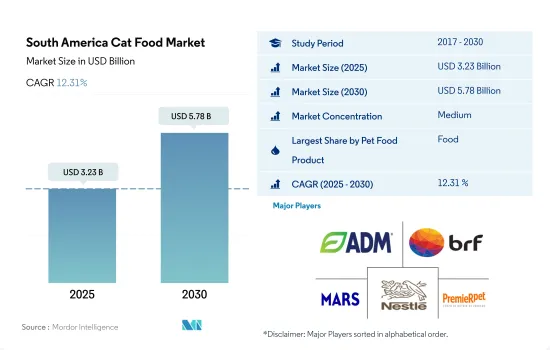

南米のキャットフード市場規模は2025年に32億3,000万米ドルと推定・予測され、2030年には57億8,000万米ドルに達し、予測期間(2025~2030年)のCAGRは12.31%で成長すると予測されています。

ペットの健康に対する飼い主の関心の高まりと市販ペットフードの潜在的利益が市場を牽引

- 南米では近年、都市部を中心に猫の飼育数が着実に増加しています。猫は独立心が強く、気難しい性格で知られているため、犬よりも飼育スペースや世話の手間がかからないペットを好む飼い主に人気があります。2022年には、南米のペットフード市場の19.5%を猫が占め、2017~2021年の間に46.2%増加し、同期間に猫の飼育数は13.6%増加しました。

- ウェットフードは水分と肉の含有量が高く、猫の自然食と栄養要件に合致しているため、猫に好まれる選択肢として浮上しています。そのため、2022年にはウェットフードが南米の猫用ペットフード市場の52.9%を占めています。

- ペット用スナックセグメントは猫用ペットフード市場で第2位のシェアを占めています。2022年には、南米で2億5,680万米ドルを占めています。スナックはご褒美として、また特に新しく飼い始めた猫との絆を深めるために広く使われています。フリーズドライのスナックは大きな人気を集めており、2022年にはスナックセグメントの24.6%を占めます。肉の魅力的な香りと味が、フリーズドライのスナックを猫にとって非常に魅力的なものにしています。

- 猫の飼育率の上昇に伴い、スナックの利用はさらに増加すると予想され、感染症やアレルギーを持つ猫用の動物用食事も成長すると予測されます。予測期間中、南米ではスナックと動物用食餌のCAGRはそれぞれ16.4%と16.2%を記録すると予測されます。

- 猫の飼育数の増加、ペットの健康に対する関心の高まり、市販のペットフードが提供する潜在的な利益を考慮すると、南米のキャットフード市場は予測期間中にCAGR 12.8%を記録すると予測されます。

ブラジルとアルゼンチンは南米の主要キャットフード市場です。

- 世界的に見て、南米は市場の一つです。この地域は、猫の飼育数が多いこと、特殊なペットフードに対する意識が高まっていること、キャットフード製品の需要増に対応するために企業が製造施設を拡大していることから、予測期間中に成長する可能性が高いです。例えば、2017~2020年にかけて、Agroindustrias BairesとEmpresas Carozzi SAが製造施設を拡大しました。

- ブラジルはこの地域で大きな市場シェアを有しており、南米のキャットフード産業の市場開拓にとって重要な国の一つです。ブラジルの2022年の市場規模は13億米ドルで、同地域で最も猫の飼育数が多いため、地域市場で大きなシェアを占めています。2022年の猫の飼育数は2,870万人で、南米の猫の飼育数の55.5%を占めています。

- アルゼンチンは、プレミアム化の進展、消費者の嗜好の変化、Molino ChacabucoやBaires SAなどの国内企業が顧客に新しいプレミアム製品を提供していることから、推定・予測期間中にCAGR 14.8%を記録するとみられます。2022年には、これらの企業が新しいスナック、ウェットフード、動物用飼料を製品に追加しました。

- 南米の企業は、獣医師、専門店、ペットショップを通じて、現地の味とレシピの猫用プレミアムペットフードを顧客に提供することに注力しています。さらに、利便性と製品の保存性を高めるトリラミネート包装でこれらの製品を提供しています。

- 製品提供の増加、プレミアム化、猫の飼育数の多さなどの要因が、予測期間中の南米のキャットフード市場の開拓に役立つと予想されます。

南米のキャットフード市場動向

ブラジルは、狭い居住空間への適応性と低メンテナンス性により、この地域で最大の猫の飼育数を占める

- 南米のペット猫の飼育数は着実に増加しており、2019~2022年の間に13.3%増加しました。この増加動向は、パンデミックによってもたらされた長期の自宅監禁期間中に、コンパニオンとしての猫の採用率が高まったことに起因すると考えられます。この地域の国々の中では、ブラジルが最も猫の数が多く、2022年時点で猫の総個体数の約55.5%を占めていました。南米では、2022年のペット数全体に占める猫の割合は19.3%でした。このように猫の割合が相対的に低いのは、犬がより実用的で価値のあるペットであるという文化的認識に起因している可能性があります。その結果、猫の数は同地域の犬の総個体数の50.0%に過ぎなかりました。

- しかし、猫は狭い居住空間でも窮屈さを感じることなく適応できること、犬に比べて維持費が安いことが、猫飼育への嗜好を高める一因となりました。この動向により、この地域全体で猫のペット数が大幅に増加しました。ブラジルだけでも、2020年時点で約1,430万世帯が猫をペットとして飼っています。同様にアルゼンチンでも猫の飼育率は高く、31.4%、460万世帯が猫をペットとして飼っています。

- この地域の重要な新たな動向は、猫カフェの設立です。2021年現在、ブラジルには約20の猫カフェがあり、客に快適な環境で猫と触れ合いながら飲み物を楽しむというユニークな機会を提供しています。このような猫カフェの動向の高まりと、猫が小さな居住空間を採用する能力は、この地域で人気のペットとしての猫の採用をさらに促進する可能性があります。

高所得の飼い主による天然材料のキャットフードへの嗜好と製品のプレミアム化の進展がペットへの支出を促進

- 南米における猫のペットへの支出は、2019~2022年にかけて着実に約22.3%増加しました。この増加は主に、同地域全体でのペット飼育率の上昇によるものです。例えば、ブラジルでペットの猫を所有している世帯数は2016~2020年の間に約11.1%増加し、アルゼンチンでは約10.3%増加しました。同地域のペットオーナーは、ペットのヒューマニゼーションにますます注力するようになっており、高所得のペットオーナーは、天然成分の使用や製品のプレミアム化を通じて売上成長を促進しています。例えば、ブラジルのプレミアムドライキャットフードの小売販売額は、2016年の1億20万米ドルから2022年には1億2,240万米ドルに増加し、CAGRは3.4%となりました。

- しかし、この地域全体が景気後退に見舞われているため、価格への敏感さがキャットフードのブランドを選択する際の重要な要因となっています。アルゼンチンでは、ペットの飼い主は出費を管理するため、頻繁にブランドを変更したり、最も手頃な価格の選択肢を選んだりしています。2020年の売上高の大部分は「エコノミー」フードブランドに属し、ドライ・キャットフードの総売上高の49.5%を占めました。この動向は、費用対効果の高いキャットフードを好む傾向が強いことを示しています。

- この地域では、ペットショップ、動物病院、スーパーマーケットといったオフラインの小売チャネルが、ペットフード製品の購入に好まれる流通チャネルです。しかし、COVID-19の大流行中、ペットフード流通におけるeコマースのシェアは2022年時点で11.1%に達しました。プレミアムペットフードの消費量の増加と、健康的で栄養価の高いペットフードの利点に関する意識の高まりが、この地域におけるペット支出を増加させました。

南米のキャットフード産業概要

南米のキャットフード市場は適度に統合されており、上位5社で50.26%を占めています。この市場の主要企業は、ADM、BRF Global、Mars Incorporated、Nestle(Purina)、PremieRpetです。

その他の特典

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブ製品別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブ製品別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Alltech

- BRF Global

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- Farmina Pet Foods

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PremieRpet

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001467

The South America Cat Food Market size is estimated at 3.23 billion USD in 2025, and is expected to reach 5.78 billion USD by 2030, growing at a CAGR of 12.31% during the forecast period (2025-2030).

Increasing focus of pet owners on their pet health and the potential benefits of commercial pet foods are driving the market

- The cat population in South America has been steadily growing in recent years, particularly in urban areas. Cats are known for their independent nature and finicky behavior, making them a popular choice for pet owners who prefer pets requiring less space and attention than dogs. In 2022, cats accounted for 19.5% of the South American pet food market, which increased by 46.2% between 2017 and 2021, with a rise in the cat population by 13.6% over the same period.

- Wet food has emerged as the preferred choice for cats due to its high moisture and meat content, which aligns with their natural diet and nutritional requirements. Therefore, in 2022, wet food accounted for 52.9% of the South American cat pet food market.

- The pet treats segment holds the second-largest share in the cat pet food market. In 2022, it accounted for USD 256.8 million in South America. Treats are widely used as rewards and for developing a bond, particularly with newly adopted cats. Freeze-dried treats have gained significant popularity, accounting for 24.6% of the treats segment in 2022. The irresistible aroma and flavor of meat make freeze-dried treats highly attractive to cats.

- The usage of treats is expected to increase further with the rise in cat adoption, while veterinary diets for cats with infections or allergies are also anticipated to grow. During the forecast period, treats and veterinary diets are projected to record CAGRs of 16.4% and 16.2%, respectively, in South America.

- Considering the growing cat population, increasing concerns about pet health, and the potential benefits offered by commercial pet foods, the cat food market in South America is estimated to register a CAGR of 12.8% during the forecast period.

Brazil and Argentina are major cat food markets in South America due to the higher cat population in these countries

- Globally, South America is one of the developing cat food markets. The region has a high potential to grow during the forecast period as there is a high population of cats, growing awareness about specialized pet food, and companies expanding their manufacturing facilities to meet the growing demand for cat food products. For instance, from 2017 to 2020, Agroindustrias Baires and Empresas Carozzi SA expanded their manufacturing facilities.

- Brazil has a significant market share in the region and is one of the important countries for the development of the South American cat food industry. The country had a market value of USD 1.3 billion in 2022 and a significant share of the regional market due to the highest cat population in the region. It had a cat population of 28.7 million in 2022 and accounted for 55.5% of the cat population in South America.

- Argentina is estimated to register a CAGR of 14.8% during the forecast period as there is an increase in premiumization, changing consumer preferences, and domestic companies such as Molino Chacabuco and Baires SA offering new premium products to their customers. In 2022, these companies added new treats, wet food, and veterinary diets to their product offerings.

- The companies in South America are focusing on providing their customers with premium pet food for cats in the local flavors and recipes through veterinarians, specialty stores, and pet shops. Additionally, they are offering these products in trilaminate packaging that ensures greater convenience and preservation of products.

- Factors such as an increase in product offerings, premiumization, and high cat population are expected to help in the development of the South American cat food market during the forecast period.

South America Cat Food Market Trends

Brazil accounted for the largest cat population in the region owing to their adaptability to smaller living spaces and lower maintenance

- The pet cat population in South America has been steadily increasing, and it increased by 13.3% between 2019 and 2022. This upward trend could be attributed to the higher adoption rates of cats as companions during the extended periods of home confinement brought on by the pandemic. Among the countries in the region, Brazil had the largest cat population, accounting for about 55.5% of the total cat population as of 2022. In South America, cats comprised 19.3% of the overall pet population in 2022. This relatively lower proportion of cats could be attributed to the cultural perception that dogs are more practical and valued pets. As a result, the number of cats represented only 50.0% of the total dog population in the region.

- However, the adaptability of cats to smaller living spaces, without feeling confined, coupled with their lower maintenance costs compared to dogs, contributed to an increased preference for cat ownership. This trend led to a significant rise in the pet cat population across the region. In Brazil alone, as of 2020, about 14.3 million households owned cats as pets. Similarly, in Argentina, the rate of cat ownership was higher, with 31.4% of households, or 4.6 million households, having cats as pets.

- An important emerging trend in the region is the establishment of cat cafes. As of 2021, around 20 cat cafes were in Brazil, providing customers with a unique opportunity to enjoy a drink while interacting with cats in a comfortable setting. This growing trend of cat cafes and the cat's ability to adopt smaller living spaces can further enhance the adoption of cats as popular pets in the region.

Higher-income pet owners' preference for natural ingredient cat food and growing product premiumization driving pet expenditure

- The expenditure on pet cats in South America steadily increased by about 22.3% between 2019 and 2022. This increase was mainly due to the rising pet ownership across the region. For instance, the number of households owning a pet cat in Brazil increased by about 11.1% between 2016 and 2020, while in Argentina, it increased by about 10.3%. Pet owners in the region are increasingly focused on pet humanization, and higher-income pet owners are driving sales growth through the use of natural ingredients and product premiumization. For instance, the retail sales value of premium dry cat food in Brazil saw a rise from USD 100.2 million in 2016 to USD 122.4 million in 2022, with a CAGR of 3.4%, reflecting the rising demand for premium cat products.

- However, with an economic downturn prevailing across the region, price sensitivity has become a crucial factor in choosing cat food brands. In Argentina, pet owners frequently switch brands or opt for the most affordable options to manage their expenses. The largest portion of sales in 2020 belonged to 'Economy' food brands, which accounted for 49.5% of the total dry cat food sales value. This trend indicates the leading preference for cost-effective cat food options.

- Offline retail channels such as pet shops, vet clinics, and supermarkets are the preferred distribution channels for purchasing pet food products in the region. However, during the COVID-19 pandemic, e-commerce's share in pet food distribution reached 11.1% as of 2022. The higher consumption of premium pet food and growing awareness about the benefits of healthy, nutritious pet food helped increase pet expenditure in the region.

South America Cat Food Industry Overview

The South America Cat Food Market is moderately consolidated, with the top five companies occupying 50.26%. The major players in this market are ADM, BRF Global, Mars Incorporated, Nestle (Purina) and PremieRpet (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Alltech

- 6.4.3 BRF Global

- 6.4.4 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.5 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.6 Farmina Pet Foods

- 6.4.7 General Mills Inc.

- 6.4.8 Mars Incorporated

- 6.4.9 Nestle (Purina)

- 6.4.10 PremieRpet

- 6.4.11 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

南米のキャットフード:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 280 Pages

- 納期

- 2~3営業日