アジア太平洋のオートミルク:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Oat Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 183 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693880

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

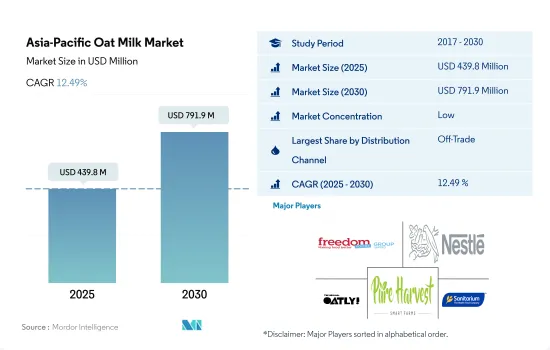

アジア太平洋のオートミルク市場規模は2025年に4億3,980万米ドルと推定され、2030年には7億9,190万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは12.49%で成長します。

人気チェーンの幅広い存在が市場成長を支える

- アジア太平洋のオートミルク販売は、他の流通チャネルに比べ、オフチャネルが支配的です。スーパーマーケットとハイパーマーケットが2022年のオートミルク販売シェアのほとんど、すなわち57.8%を占めました。この成長は、これらの店舗で国際ブランドや地元ブランドを入手できることによるものです。

- コンビニエンスストアは、オートミールの販売において2番目に広く選ばれている小売チャネルです。コンビニエンスストアを通じたオートミルクの販売額は、2022年と比較して2025年には31.5%の成長が見込まれます。Easy Joy、Meiyijia、7-Eleven Inc.、Lawsonのようなトップクラスのコンビニエンスストアは、消費者を引き付けるために、オートミルクのような代替乳製品を年会費やまとめ買い割引で提供しています。この動向は予測期間中、オートミルクの売上を牽引すると予想されます。2021年現在、Easy Joyは中国に2万7,600以上の店舗を持つ最大のコンビニエンスストアです。2位はMeiyijiaで2万2,394店舗、3位はセブンイレブンで2万988店舗です。

- 外食チャネルからのオートミルク飲料の需要が増加しており、市場の成長をさらに後押ししています。この地域では多くのコーヒーチェーンやレストランがメニューにオートミルクを提供しています。オンチャネルからのオートミルク売上は2020~2022年にかけて11.3%増加したが、これは消費者がレストランでの外食時やテイクアウトの注文時など、自宅から離れた場所でオートミルクのような代替乳製品を好むことに起因しています。2021年現在、インドの消費者は月に7回近く外食をし、回答者の80%以上が手頃なカジュアルダイニングやファーストサービスレストランを好むと回答しています。

オートミルク消費への消費者志向の高まりにより中国が大きなシェアを占める

- 西洋文化の普及に伴い、フレキシタリアンやヴィーガンのライフスタイルの採用が大きく伸びています。2021年、韓国では約250万人が菜食主義を実践し、過去2-3年で大幅に増加しました。この動向の高まりがオートミールの消費を促進する大きな要因となっています。

- 健康とウェルネスに対する意識の高まりと、心臓病、高血圧、糖尿病、喘息といった消費者の健康問題の増加が、この地域全体でオートミルクを含む植物由来の代替乳製品の消費を促進しています。乳糖不耐症の消費者の多くは牛乳や乳製品を摂取しないため、オートミルクの需要が増加しています。アジア太平洋におけるオートミルクの販売額は、2021年と比較して10.82%成長すると予測されています。

- 乳糖不耐症は、アジア諸国、特に東アジアで増加しているもう一つの懸念であり、人口の70%近くが乳糖不耐症です。牛乳アレルギーは幼児によく見られる食物アレルギーのひとつです。日本の消費者の多くも乳糖不耐症で、牛乳や乳製品を摂取していないです。2022年の時点で、オーストラリアでは乳幼児の約50人に1人に牛乳アレルギーの兆候が見られました。そのため、オートミールの需要は地域全体で徐々に増加しています。

- 同地域の消費者の栄養選択に対する意識は高まっています。多忙なライフスタイルのため、消費者の購買決定は製品の栄養価に左右されます。特に乳製品にアレルギーのある消費者は、代替品としてオートミルクの消費に熱心です。

アジア太平洋のオートミルク市場動向

菜食主義者の増加がオートミルクの消費を促進

- ヴィーガン人口の増加により、一人当たりのオートミルク消費量はここ数年増加しています。ヴィーガン音楽フェスティバルは、人口一人当たりのヴィーガン人口比率が世界で3番目に高いオーストラリアのような数多くの国で実施されています。2022年現在、同国には250万人のヴィーガンとベジタリアンがいます。同様に、韓国では約280万人が菜食主義者です。これは過去2~3年で大幅に増加し、植物性ミルク(オートミルク)を含む乳製品代替製品の消費を促進する大きな要因と考えられています。

- 乳糖不耐症はアジア諸国、特に東アジアで最も多く、人口の70~100%近くが乳糖不耐症です。この地域で乳糖不耐症の消費者が増加していることも重要な点です。しかし、牛乳アレルギーは幼児によく見られる食物アレルギーでもあります。日本の消費者の多くは乳糖不耐症で、牛乳や牛乳関連製品を摂取していないです。2022年現在、オーストラリアでは、乳幼児の約50人に1人に牛乳アレルギーの兆候が見られました。そのため、オートミルクの需要はアジア太平洋で大幅に増加しています。

- 豆乳に含まれるホルモン(植物性エストロゲンまたはイソフラボン)を懸念したサステイナブル原料調達に対する消費者の嗜好により、オート麦乳の一人当たり消費量は常に増加しています。オートミルクはまた、遺伝子組み換え作物不使用、低脂肪、アレルゲン不使用をうたっており、消費者の食生活を多様化する植物由来の選択肢を増やしています。この地域におけるオートミルクの一人当たり消費量は、2023~2024年にかけて10.22%増加すると推定されます。

アジア太平洋のオートミルク産業概要

アジア太平洋のオートミルク市場は細分化されており、上位5社で26.07%を占めています。この市場の主要企業は、Freedom Foods Group Ltd、Nestle SA、Oatly Group AB、PureHarvest、Sanitarium Health、Wellbeing Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原料/商品生産量

- オート麦

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 流通チャネル

- オフトレード

- サブ流通チャネル別

- コンビニエンスストア

- オンライン小売

- 専門店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- パキスタン

- 韓国

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Califia Farms LLC

- Danone SA

- Freedom Foods Group Ltd

- Milkin Oats

- Minor Figures Limited

- Nestle SA

- Oatly Group AB

- PureHarvest

- Ripple Foods PBC

- Sanitarium Health and Wellbeing Company

- SunOpta Inc.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50000749

The Asia-Pacific Oat Milk Market size is estimated at 439.8 million USD in 2025, and is expected to reach 791.9 million USD by 2030, growing at a CAGR of 12.49% during the forecast period (2025-2030).

Wide presence of popular chains is supporting the market growth

- The off-trade channel dominates oat milk sales in Asia-Pacific compared to other distribution channels. Supermarkets and hypermarkets accounted for most of the share of oat milk sales in 2022, i.e., 57.8%. This growth was due to the availability of international and local brands at these stores.

- Convenience stores are the second most widely preferred off-trade retail channel for oat milk sales. The sales value of oat milk through convenience stores is anticipated to grow by 31.5% in 2025 compared to 2022. Top convenience stores like Easy Joy, Meiyijia, 7-Eleven Inc., and Lawson are offering dairy alternatives, such as oat milk, with annual memberships and discounts on bulk purchases to attract consumers. This trend is expected to drive oat milk sales during the forecast period. As of 2021, Easy Joy was the largest convenience store, with more than 27,600 outlets in China. Meiyijia and 7-Eleven stood second and third with 22,394 and 20,988 stores, respectively.

- There is an increasing demand for oat milk drinks from foodservice channels, further boosting the market's growth. Many coffee chains and restaurants in the region offer oat milk on their menus. Oat milk sales from the on-trade channel grew by 11.3% from 2020 to 2022, attributed to consumers preferring dairy alternatives, such as oat milk, away from home, whether while dining out at a restaurant or ordering takeout. As of 2021, Indian consumers ate out nearly seven times a month, and over 80% of the respondents stated that they would prefer affordable casual dining options and fast-service restaurants.

China holds significant share due to growing increases consumers inclination towards oat milk consumption

- With the growing adoption of Western culture, there is a significant growth in the adoption of flexitarian and vegan lifestyles. In 2021, around 2.5 million people in South Korea followed a vegan diet, which increased significantly in the past 2-3 years. This growing trend is a major factor driving the consumption of oat milk..

- Rising awareness of health and wellness and the growing health problems among consumers, such as heart diseases, high blood pressure, diabetes, and asthma, are driving the consumption of plant-based dairy alternatives, including oat milk, across the region. Many lactose-intolerant consumers do not consume milk or milk products, leading to increased demand for oat milk. The sales value of oat milk in the Asia-Pacific region is anticipated to grow by 10.82% compared to 2021.

- Lactose intolerance is another growing concern in Asian countries, particularly in East Asia, where nearly more than 70% of the population has lactose intolerance. Cow milk allergy is one of the common food allergies in young children. Many Japanese consumers are also lactose-intolerant and do not consume milk or milk products. As of 2022, around 1 in 50 babies and young children in Australia showed signs of an allergy to cow's milk. Therefore, oat milk demand is increasing gradually across the region.

- Consumers in the region are becoming increasingly aware of their nutritional choices. Owing to their busy lifestyles, their purchasing decision depends on a product's nutritional value, thus driving the demand for plant-based milk in the region. Consumers, especially those allergic to dairy milk, are keen on consuming oat milk as a substitute.

Asia-Pacific Oat Milk Market Trends

The rising vegan population drives the consumption of oat milk

- Oat milk consumption per person has increased for the past few years due to the growing vegan population. Vegan music festivals are being conducted in numerous countries like Australia, which has the third-highest percentage of vegans per capita globally. As of 2022, the country had 2.5 million vegans and vegetarians. Similarly, around 2.8 million people in South Korea follow a vegan diet. This increased significantly in the past 2-3 years and was considered a major factor driving the consumption of dairy alternative products, including plant-based milk (oat milk).

- Lactose intolerance is most common in Asian countries, particularly in East Asia, where nearly 70-100% of the population is lactose intolerant. The growing volume of lactose-intolerant consumers in the region has been another important aspect. However, cow milk allergy is also a common food allergy in young children. Many Japanese consumers are lactose intolerant and do not consume milk or milk-related products. As of 2022, in Australia, around one in 50 babies and young children showed signs of an allergy to cow's milk. Thus, the demand for oat milk is increasing significantly across the Asia-Pacific region.

- There is a constant rise in the per capita consumption of oat milk due to consumer preference toward sustainable ingredient sourcing, which is concerned with the hormones (plant estrogen or isoflavones) found in soy milk. Oat milk also comes with GMO-free, low-fat, and allergen-free claims, giving consumers more plant-based options to choose from to diversify their diets. The per capita consumption of oat milk in the region is estimated to increase by 10.22% from 2023 to 2024.

Asia-Pacific Oat Milk Industry Overview

The Asia-Pacific Oat Milk Market is fragmented, with the top five companies occupying 26.07%. The major players in this market are Freedom Foods Group Ltd, Nestle SA, Oatly Group AB, PureHarvest and Sanitarium Health and Wellbeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Oats

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Japan

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Distribution Channel

- 5.1.1 Off-Trade

- 5.1.1.1 By Sub Distribution Channels

- 5.1.1.1.1 Convenience Stores

- 5.1.1.1.2 Online Retail

- 5.1.1.1.3 Specialist Retailers

- 5.1.1.1.4 Supermarkets and Hypermarkets

- 5.1.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.1.2 On-Trade

- 5.1.1 Off-Trade

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 China

- 5.2.3 India

- 5.2.4 Indonesia

- 5.2.5 Japan

- 5.2.6 Malaysia

- 5.2.7 New Zealand

- 5.2.8 Pakistan

- 5.2.9 South Korea

- 5.2.10 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Califia Farms LLC

- 6.4.2 Danone SA

- 6.4.3 Freedom Foods Group Ltd

- 6.4.4 Milkin Oats

- 6.4.5 Minor Figures Limited

- 6.4.6 Nestle SA

- 6.4.7 Oatly Group AB

- 6.4.8 PureHarvest

- 6.4.9 Ripple Foods PBC

- 6.4.10 Sanitarium Health and Wellbeing Company

- 6.4.11 SunOpta Inc.

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アジア太平洋のオートミルク:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 183 Pages

- 納期

- 2~3営業日