|

市場調査レポート

商品コード

1683834

米国のオートミルク:市場シェア分析、産業動向、成長予測(2025年~2030年)United States Oat Milk - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のオートミルク:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

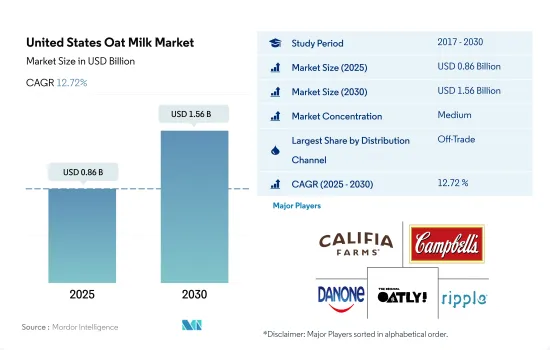

米国のオートミルク市場規模は2025年に8億6,000万米ドルと推定され、2030年には15億6,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは12.72%で成長する見込みです。

オムニチャネル戦略を採用する人気のオートミルク小売業者と相まってブランド・ロイヤルティが市場を牽引

- 米国のオートミルク市場は、オートミルクを含む幅広い植物性ミルクが小売店や外食チャネルで容易に入手できるようになったことが要因で、2022年には金額ベースで2021年比8.54%のプラス成長を記録しました。スーパーマーケットは、2022年には92.06%と、非売品セグメントのシェアの大半を占めました。これは、Lidl、Aldi、Walmart、Kroger、Targetといった人気チェーンが強力に浸透しており、輸入品と国産のオートミルクの幅広い品揃えを提供しているためです。

- オンライン小売は最も急成長するチャネルであり、2023年と比較して2029年には133.9%成長すると予想されます。大手小売企業が採用するオムニチャネル・アプローチもオートミルク市場を牽引しています。コストコ(Costco)、トレーダー・ジョーズ(Trader Joe's)、ウォルマート(Walmart)などの小売業者はオムニチャネル・ショッピングに力を入れており、特にオンライン機能を実店舗に拡大・統合しています。買い物客にとって、利便性は主要な動機のひとつです。そのため、食料品を含む生活必需品のオンライン・ショッピングへの移行が進んでいます。

- オーツミルクは牛乳に似たテクスチャーとニュートラルな風味から、植物性ミルクへの切り替えを望む消費者に好まれています。米国では2022年、プラネット・オートがオートミルクのトップブランドで、オートリー、チョバーニがこれに続いた。2022年9月現在、Planet Oatはオン・トレードおよびオフ・トレード・チャネルを通じて4,490万米ドル以上の売上をあげています。オフトレード・チャネルの多くも国内でプライベート・ブランドのオートミルクを発売しています。米国のプライベート・ラベルのオートミルク・ブランドは、2022年半ばまでに362万米ドル以上の売上を上げました。

米国のオートミルク市場動向

肥満率の上昇と相まって、製品イノベーションと投資の増加がオートミルクの消費を促進しています。

- 米国では、投資と技術革新に支えられてオートミルクの一人当たり消費量が大幅に増加しており、その結果、米国の消費者の52%以上が植物性食品を好むようになっています。この成長は主に、米国では動物が人道的に扱われない工場畜産が主流であるため、動物福祉を支援するために菜食主義に転向する人が増えていることによる。多くのアメリカ人は、一般的に乳製品やその他の動物性食品の摂取量を減らしているが、完全にそれらを排除しているわけではないです。ヴィーガンやベジタリアンに比べ、フレキシタリアンの数は多いです。2022年現在、米国の消費者の7%がフレキシタリアンであるのに対し、植物性の食事を好む消費者は12%を超えています。あらゆる年代のアメリカ人が植物性食品に関心を持っているが、20代と30代が最も関心を持っています。

- 米国は世界で最も肥満率が高い国のひとつです。2021年11月現在、米国の成人肥満率は30%以上で、19の州が35%以上を維持しています。同国では乳糖不耐症の消費者が増加していることも、オートミルクを含む植物性ミルク市場を牽引しています。2022年には、3,000万~5,000万人のアメリカ人が乳糖不耐症となります。こうした問題に対処するため、人々は健康を維持する方法を模索し、健康的なライフスタイルを選ぶようになっています。オートミールは、減量と乳糖不耐症のために2番目に多く消費されている植物性ミルクです。

- 豆乳に含まれるホルモン(植物性エストロゲンやイソフラボン)を懸念し、持続可能な原料調達を求める消費者の嗜好により、オートミルクの一人当たりの消費量は増加の一途をたどっています。オートミルクには遺伝子組み換え作物不使用、低脂肪、アレルゲン不使用の表示もあり、消費者の食生活を多様化する植物由来の選択肢が増えました。ホルモン剤や抗生物質不使用と表示された製品は、過去4年間で2桁成長を記録し、昨年の売上高は114億米ドルに達しました。

米国オートミルク産業の概要

米国のオートミルク市場は適度に統合されており、上位5社で60.71%を占めています。この市場の主要企業は以下の通りです。 Califia Farms LLC, Campbell Soup Company, Danone SA, Oatly Group AB and Ripple Foods Pbc.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原材料/商品生産量

- オート麦

- 規制の枠組み

- 米国

- バリューチェーンと流通経路分析

第5章 市場セグメンテーション

- 流通チャネル

- オフ・トレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オン・トレード

- オフ・トレード

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)。

- Betterbody Foods & Nutrition LLC

- Califia Farms LLC

- Campbell Soup Company

- Danone SA

- Elmhurst Milked LLC

- Green Grass Foods Inc.(Nutpods)

- HP Hood LLC

- Oatly Group AB

- Ripple Foods Pbc

- The Rise Brewing Co.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50000719

The United States Oat Milk Market size is estimated at 0.86 billion USD in 2025, and is expected to reach 1.56 billion USD by 2030, growing at a CAGR of 12.72% during the forecast period (2025-2030).

Market is driven by the brand loyalty coupled with popular oat milk retailers adopting omnichannel strategies

- The US oat milk market witnessed a positive growth of 8.54% by value in 2022 compared to 2021, attributed to the easy availability of a wide range of plant-based milk, including oat milk, across retail and foodservice channels. Supermarkets accounted for most of the share in the off-trade segment, i.e., 92.06% in 2022, attributed to the strong penetration of popular chains such as Lidl, Aldi, Walmart, Kroger, and Target, which provide a wide selection of oat milk varieties that are both imported and made locally.

- Online retail is anticipated to be the fastest-growing channel, growing by 133.9% in 2029 compared to 2023. The omnichannel approach adopted by major retailers is also driving the market for oat milk. Retailers such as Costco, Trader Joe's, and Walmart focus on omnichannel shopping, particularly expanding and integrating online capabilities into brick-and-mortar stores. Convenience is one of the primary motivations for shoppers. Thus, they are transitioning to online shopping for daily essentials, including groceries.

- Due to its similar texture to cow's milk and neutral flavor, oat milk is well-liked by consumers who want to switch to plant-based milk. In the United States, Planet Oat was the leading brand of oat-based milk in 2022, followed by Oatly and Chobani. As of September 2022, Planet Oat generated sales of over USD 44.9 million via on-trade and off-trade channels. Many off-trade channels have also launched oat milk under their private labels in the country. Private-labeled oat milk brands in the United States generated sales of over USD 3.62 million by mid-2022.

United States Oat Milk Market Trends

Increased product innovations and investments, coupled with rising obesity rate, are driving the consumption of oat milk

- The per capita consumption of oat milk is rising significantly in the United States, supported by investments and innovations, resulting in more than 52% of US consumers preferring plant-based food. This growth is primarily due to the growing number of people turning to veganism to support animal welfare, as factory farming, where animals are not treated humanely, is the norm in the United States. Most Americans generally consume less dairy and other animal products, but they are not doing away with them entirely. In comparison to vegans or vegetarians, there are more flexitarians in the country. As of 2022, 7% of US consumers adopted a flexitarian diet, compared to over 12% who prefer a plant-based diet. Although Americans of all ages are interested in plant-based foods, people in their 20s and 30s are the most interested.

- The United States has one of the highest obesity rates in the world. As of November 2021, the United States had adult obesity rates of 30% or higher, with 19 states maintaining rates of 35% or higher. The growing number of lactose-intolerant consumers in the country is also driving the plant-based milk market, including oat milk. In 2022, 30-50 million Americans were lactose intolerant. To counter these problems, people are exploring ways to stay fit and opting for healthy lifestyles. Oat milk is the second most consumed plant milk for weight loss and lactose intolerance.

- There is a constant rise in the per capita consumption of oat milk due to consumer preference for sustainable ingredient sourcing, which is concerned with hormones (plant estrogen or iso-flavones) found in soy milk. Oat milk also comes with GMO-free, low-fat, and allergen-free claims, giving consumers more plant-based options to diversify their diets. Products labeled hormone- or antibiotic-free posted double-digit growth in the past four years, generating USD 11.4 billion in sales last year.

United States Oat Milk Industry Overview

The United States Oat Milk Market is moderately consolidated, with the top five companies occupying 60.71%. The major players in this market are Califia Farms LLC, Campbell Soup Company, Danone SA, Oatly Group AB and Ripple Foods Pbc (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Oats

- 4.3 Regulatory Framework

- 4.3.1 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Distribution Channel

- 5.1.1 Off-Trade

- 5.1.1.1 Convenience Stores

- 5.1.1.2 Online Retail

- 5.1.1.3 Specialist Retailers

- 5.1.1.4 Supermarkets and Hypermarkets

- 5.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.1.2 On-Trade

- 5.1.1 Off-Trade

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Betterbody Foods & Nutrition LLC

- 6.4.2 Califia Farms LLC

- 6.4.3 Campbell Soup Company

- 6.4.4 Danone SA

- 6.4.5 Elmhurst Milked LLC

- 6.4.6 Green Grass Foods Inc. (Nutpods)

- 6.4.7 HP Hood LLC

- 6.4.8 Oatly Group AB

- 6.4.9 Ripple Foods Pbc

- 6.4.10 The Rise Brewing Co.

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms