中東・アフリカのビジネスジェット市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Middle-East and Africa Business Jet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 178 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693586

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

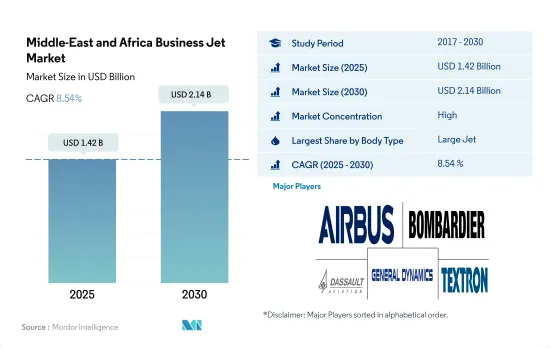

中東・アフリカのビジネスジェット市場規模は2025年に14億2,000万米ドルと推定・予測され、2030年には21億4,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは8.54%で成長すると予測されます。

大型ジェット機が市場の需要を牽引

- 中東・アフリカは、2017~2022年までの世界のビジネスジェット機納入台数の約3%を占めています。パンデミック後、同地域のビジネスジェット需要は2021年に26%減少し、特に大型ビジネスジェットセグメントで減少しました。

- 中東・アフリカのゼネラル・アビエーション市場における大型ジェット機セグメントは、現在の運航機数の大半を占めており、全588機のうち293機を占めています。中東・アフリカでは、大型ジェット機の採用がより一般的です。2022年7月現在、大型ジェット機は中東のビジネスジェット機全体の約50%を占め、アフリカ地域では36%を占めています。

- 2022年、エア・チャーターサービスプロバイダは、ビジネスアビエーションの新規加盟が急増し、地域全体で高い需要を目の当たりにしました。例えば、2021年には、アラブ首長国連邦を拠点とするエア・チャーターサービスプロバイダのVistaJetが、2021年1月から6月にかけて新規会員数で約100%の伸びを記録しました。

- 2022年7月現在の中東のビジネスジェット機保有率は、ボンバルディアが23%でトップ、次いでガルフストリームが21%、Boeingが14%でした。アフリカでは、ボンバルディアが現在の運航機数の22%を占めてトップで、セスナ、BAE、ガルフストリームがそれぞれ21%、15%、13%で続きました。この地域におけるUHNWIの急増は、同国のビジネスジェットセグメントを後押しすると予想されます。2022~2028年にかけて、およそ200機以上の航空機が納入される見込みです。

プライベートジェットを初めて利用する人の数が増加し、市場の成長をさらに後押し

- 中東・アフリカは、2017~2022年までの世界のビジネスジェット納入数の約3%を占めます。COVID-19パンデミック後、この地域のビジネスジェット需要は、特に大型ビジネスジェットセグメントにおいて、2020年と比較して2022年には42%急増しました。COVID-19パンデミック後、プライベートジェットを初めて利用する人が増加しました。また、地域企業は欧州諸国からの長距離移動の増加を目の当たりにしています。

- 中東・アフリカでは、大型ジェット機の導入が進んでいます。2022年12月現在、中東のビジネスジェット機保有台数全体では、大型ジェット機が約65%を占め、次いで中型ジェット機が19%、小型ジェット機が13%となっています。ガルフストリームは、ガルフストリームG450やG650ERなどの大型ジェット機でこの地域の成長機会に注力しています。

- 2021年、航空チャーターサービスプロバイダは、中東・アフリカ全域でビジネス航空の新規会員数が急増し、高い需要があることを目の当たりにしました。例えば、アラブ首長国連邦を拠点とするエア・チャーターサービスプロバイダのVista Jetは、2021年1月から6月までの新規会員数が2020年上半期と比較して約100%の伸びを記録しました。

- 2022年12月現在、中東のビジネスジェット機保有台数に占めるシェアは、ガルフストリームが15%でトップ、次いでセスナが13%、リアジェットが10%となっています。さらに、同地域のHNWI数は2017年の70万人から2022年には120万人に増加し、2017~2022年の間に72%の伸びを示しました。2023~2030年の間に約241機のビジネスジェットが納入される見込みです。

中東・アフリカのビジネスジェット市場動向

中東では石油・ガスと不動産がHNWIの成長を後押しする主要産業となった

- 2017~2022年にかけて、同時期にUHNWIの数が約4.4%しか急増しなかったアフリカと比較して、中東ではUHNWI人口が約118%急増しました。2022年、中東のUHNWI数は8%増加したが、アフリカは2021年比で0.8%減少しました。

- 中東のHNWIに優しい施策により、多くのHNWIがこれらの国々に移住しました。例えば、2022年にはアラブ首長国連邦が最も多くの富裕層を惹きつけると予想されました。同国には約4,000人の億万長者が流入すると予想されています。富裕層の多くは、インド、ロシア、アフリカ、その他の中東諸国に属しています。サウジアラビア、アラブ首長国連邦、トルコはUHNWI人口の点で主要国であり、2017~2022年の成長率はそれぞれ98%、57%、59%でした。

- 中東では、ハイテク産業への関心の高まりにより、HNWI人口の伸びは主にアラブ首長国連邦とイスラエルが牽引しました。原油価格の回復も中東・北アフリカのGDP成長を後押しし、2021年の3.9%の縮小に対し、2022年は4.3%に達しました。金融サービス、基礎材料、不動産、運輸、物流は、この地域で多くのHNWIを占める主要産業でした。アフリカでは、南アフリカ、エジプト、ケニア、ナイジェリア、モロッコが地域全体の富裕層(HNWI)の55%以上を占めています。

中東・アフリカのビジネスジェット産業概要

中東・アフリカのビジネスジェット市場はかなり統合されており、上位5社で116.69%を占めています。この市場の主要企業は、Airbus SE、Bombardier Inc.、Dassault Aviation、General Dynamics Corporation、Textron Inc.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 富裕層(HNWI)

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- ボディタイプ

- 大型ジェット機

- 小型ジェット機

- 中型ジェット機

- 国名

- アルジェリア

- エジプト

- カタール

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Bombardier Inc.

- Cirrus Design Corporation

- Dassault Aviation

- Embraer

- General Dynamics Corporation

- Honda Motor Co., Ltd.

- Pilatus Aircraft Ltd

- Textron Inc.

- The Boeing Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92736

The Middle-East and Africa Business Jet Market size is estimated at 1.42 billion USD in 2025, and is expected to reach 2.14 billion USD by 2030, growing at a CAGR of 8.54% during the forecast period (2025-2030).

Large jets are driving the demand in the market

- Middle East & Africa accounted for around 3% of the global business jet deliveries from 2017 to 2022. After the pandemic, the demand for business jets in the region declined by 26% in 2021, specifically in the large business jet segment.

- The large jet segment in the Middle East & African general aviation market dominates the current operational fleet, accounting for 293 aircraft out of the total 588 aircraft. Adopting large jets is more prevalent in the Middle East & Africa. In terms of the current operational fleet, the large jets accounted for around 50% of the overall Middle East business jet fleet and 36% in the African region of July 2022.

- In 2022, air charter service providers witnessed high demand in the entire region, with a surge in new memberships for business aviation. For instance, in 2021, the UAE-based air charter service provider VistaJet registered a growth of around 100% in new memberships during January and June 2021.

- Bombardier was the leading OEM, with 23% of the current operational fleet size, followed by Gulfstream and Boeing, with 21% and 14%, respectively, in the Middle Eastern business jet fleet as of July 2022. In Africa, Bombardier was the leading player in terms of the current operational fleet, with 22% of the jets, followed by Cessna, BAE, and Gulfstream with 21%, 15%, and 13% of the current fleet, respectively. The surge in UHNWIs in the region is expected to aid the business jet segment in the country. Around 200+ aircraft are expected to be delivered during 2022-2028.

The number of first-time flyers of private jets has increased, further aiding market growth

- The Middle East & Africa accounted for around 3% of the global business jet deliveries from 2017 to 2022. After the COVID-19 pandemic, business jet demand in this region surged by 42% in 2022 compared to 2020, specifically in the large business jet segment. The number of first-time flyers in private jets has increased after the COVID-19 pandemic. Regional companies have also witnessed increased long-distance travel from European countries.

- Adopting large jets is more prevalent in the Middle East & Africa. In terms of the current operational fleet, large jets accounted for around 65%, followed by mid-size jets and light jets with shares of 19% and 13%, respectively, of the overall Middle Eastern business jet fleet as of December 2022. Gulfstream has focused on growth opportunities in this region with its large jet offerings, such as Gulfstream G450 and G650ER.

- In 2021, air charter service providers witnessed high demand in the whole Middle East & Africa with the surge in new memberships for business aviation. For instance, in 2021, UAE-based air charter service provider Vista Jet registered a growth of around 100% in new memberships from January to June 2021 compared to the first half of 2020.

- Gulfstream is the leading original equipment manufacturer, with 15% of the operational fleet size, followed by Cessna and Learjet, with shares of 13% and 10%, respectively, in the Middle Eastern business jet fleet as of December 2022. Furthermore, the number of HNWIs in the region increased from 0.7 million in 2017 to 1.2 million in 2022, with a growth of 72% between 2017 and 2022. Around 241 business jets are expected to be delivered between 2023 and 2030.

Middle-East and Africa Business Jet Market Trends

Oil and gas and real estate were the major industries that boosted the growth of HNWIs in the Middle East

- From 2017 to 2022, there was a surge of around 118% in the UHNWI population in the Middle East compared to Africa, where the number of UHNWIs surged only by around 4.4% in the same period. In 2022, the number of UHNWIs in the Middle East increased by 8%, while Africa experienced a 0.8% decrease compared to 2021.

- The HNWI-friendly policies of the Middle East led to the migration of a large number of HNWIs into these countries. For instance, in 2022, the United Arab Emirates was expected to attract the largest number of high-net-worth individuals. An inflow of around 4,000 millionaires is expected in the country. Most of the HNWIs belong to India, Russia, Africa, and other Middle Eastern countries. Saudi Arabia, the United Arab Emirates, and Turkey were the major countries in terms of the UHNWI population, witnessing growth rates of 98%, 57%, and 59%, respectively, during 2017-2022.

- In the Middle East, the growth in the HNWI population was majorly led by the United Arab Emirates and Israel due to an increase in tech industrial focus. The recovery in oil prices also helped the GDP growth of the Middle East and North Africa, reaching 4.3% in 2022 compared to a contraction of 3.9% in 2021. Financial services, basic materials, real estate, transportation, and logistics were the major industries that accounted for a large number of HNWIs in the region. In Africa, South Africa, Egypt, Kenya, Nigeria, and Morocco account for over 55% of the overall region's high-net-worth individuals (HNWIs).

Middle-East and Africa Business Jet Industry Overview

The Middle-East and Africa Business Jet Market is fairly consolidated, with the top five companies occupying 116.69%. The major players in this market are Airbus SE, Bombardier Inc., Dassault Aviation, General Dynamics Corporation and Textron Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 High-net-worth Individual (hnwi)

- 4.2 Regulatory Framework

- 4.3 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Large Jet

- 5.1.2 Light Jet

- 5.1.3 Mid-Size Jet

- 5.2 Country

- 5.2.1 Algeria

- 5.2.2 Egypt

- 5.2.3 Qatar

- 5.2.4 Saudi Arabia

- 5.2.5 South Africa

- 5.2.6 United Arab Emirates

- 5.2.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Bombardier Inc.

- 6.4.3 Cirrus Design Corporation

- 6.4.4 Dassault Aviation

- 6.4.5 Embraer

- 6.4.6 General Dynamics Corporation

- 6.4.7 Honda Motor Co., Ltd.

- 6.4.8 Pilatus Aircraft Ltd

- 6.4.9 Textron Inc.

- 6.4.10 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

中東・アフリカのビジネスジェット市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 178 Pages

- 納期

- 2~3営業日