アジア太平洋地域のビジネスジェット機:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Asia-Pacific Business Jet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693581

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

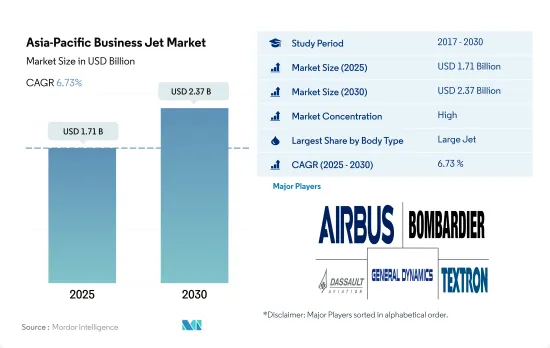

アジア太平洋地域のビジネスジェット機市場規模は、2025年に17億1,000万米ドルと推計され、2030年には23億7,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは6.73%で成長すると予測されています。

多くのビジネスジェット機はチャータージェット、プライベートジェット、コーポレートジェットに分類されるため、大型ジェット機セグメントが最も顕著です。

- ビジネスジェット機は、少人数を運ぶために設計されたプライベートジェット機です。その他にも様々な用途に使用することができます。2022年7月現在、アジア太平洋地域のビジネスジェット機は世界の保有機数の6%を占めています。このうち、大型ジェット機が52%のシェアを占め、次いで小型ジェット機が22%、中型ジェット機が17%となっています。

- 多くのビジネスジェット機がチャーター、プライベート、企業用として使用されているため、大型ジェット機セグメントが圧倒的なシェアを占めています。UHNWI(超富裕層)は、主にその航続距離、技術、キャビンの大きさ、効率性からこれらのジェット機を高く評価する主要ユーザーです。最も多く納入されているジェット機には、ガルフストリームG500/550/650/650ER、世界6000/7500エクスプレス、チャレンジャー604/605/650、ダッソー・アビエーションSAのファルコンシリーズなどがあります。

- 調査期間中、セスナ(Textron Inc.の子会社)は、21機のジェット機を納入し、ライトジェット・セグメントの主要OEMでした。ボンバルディアは6機のジェット機で中型セグメントの主要OEMであり、ゼネラル・ダイナミクスの完全子会社であるガルフストリーム・エアロスペース・コーポレーションが6機で続いた。ガルフストリーム・エアロスペース・コーポレーションは97機を保有し、ボンバルディアの45機がこれに続きます。

- ガルフストリーム・エアロスペース・コーポレーション、ボンバルディア、セスナの3社がビジネスジェット機市場を独占しており、2017年から2022年にかけてのビジネスジェット機新規納入機総数の60%を占めています。アジア太平洋地域で運航されているビジネスジェット機全体のうち、98%は完全所有であり、残りは共有と分数所有です。

プライベート・アビエーション業界は、南アジアの堅調な景気回復により、需要が大幅に増加しています。

- COVID-19パンデミック(世界的大流行)の最中、同地域の経済活動の縮小と旅行関連の制限は、ビジネスジェット機の需要と利用に影響を与えました。しかし、パンデミック後は、力強い経済回復と渡航制限の撤廃により、特に東南アジアでプライベート・ジェットの需要が高まりました。特にシンガポール、タイ、カンボジア、マレーシアでは外国からの投資が急増し、プライベート・チャーターの需要が高まりました。顧客基盤が大きいため、ビジネスジェット機OEMは主にこの地域をターゲットとしており、今後10年間は新型ビジネスジェット機に対する高い需要が見込まれています。2022年、この地域の成長率は2021年比でマイナス10%でした。

- 富裕層(HNWI)と超富裕層(UHNWI)は、個人旅行や出張にプライベートジェットを好みます。アジア太平洋地域におけるHNWIの増加は、新しいビジネスジェット機の調達に貢献しました。2017年と比較すると、この地域のHNWI人口は2022年に68%増加しました。

- アジア太平洋地域で現在運用されている1,279機のジェット機を見ると、中国が21%を占め、オーストラリア、インド、日本がそれぞれ約17%、13%、9%と続きます。セスナ、ボンバルディア、ガルフストリームを合わせると、この地域で現在運航されているビジネスジェット機の51%を占めています。2022年には、中国、オーストラリア、日本がビジネスジェット機の新規納入の主要国となります。

- 2023年から2030年にかけて、この地域では362機以上のビジネスジェット機が新たに納入される見込みです。中国や東南アジアなどの新興経済諸国における景気回復が、予測期間中のビジネスジェット機市場の成長を後押しすると予想されます。

アジア太平洋地域のビジネスジェット機市場動向

HNWI人口が急増しており、市場の最大の成長促進要因になる見込み

- HNWIは100万米ドル以上の流動性金融資産を有し、UHNWIは少なくとも3,000万米ドルの純資産を有します。2017年から2022年にかけて、この地域のHNWI人口は約90%急増しました。2022年には、アジア太平洋地域のHNWI数は2020年比で2%増加します。

- 日本は2022年に15%の成長率を記録しました。主要国におけるHNWI人口の伸びの鈍化は、アジア太平洋地域全体の富の増加に影響を及ぼしています。中国では、平均的な富の増加により、億万長者の数が70%以上増加しました。アジア太平洋地域は、同地域における富の増加、HNWI人口の増加、財務アドバイスへのニーズによって、世界的にウェルスマネジメントとプライベートバンキングの主要な目的地として台頭しつつあります。

- 政治指導者の交代やパンデミック時の消費低迷といった要因が日本の株式市場(日経平均株価)に影響を与え、同国のHNWIの成長を阻害しました。インド、ベトナム、タイなどの新興諸国は、アジア太平洋地域の主要国と比べてHNWIの成長を示しました。202年、インドのHNWI人口は292%以上の伸びを示しました。タイとベトナムは、それぞれ約21%と13%の成長を示しました。中央銀行による高い流動性支援、支持的な国内政策、株式市場の安定が、これらの国々のHNWIの成長を後押ししました。テクノロジー、産業コングロマリット、エネルギー、不動産がアジア太平洋地域のHNWIの大半を占める主要セクターでした。

アジア太平洋地域のビジネスジェット機業界の概要

アジア太平洋地域のビジネスジェット機市場はかなり統合されており、上位5社で93.20%を占めています。この市場の主要企業は以下の通り。 Airbus SE, Bombardier Inc., Dassault Aviation, General Dynamics Corporation and Textron Inc.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 富裕層(hnwi)

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- ボディタイプ

- 大型ジェット機

- 小型ジェット機

- 中型ジェット機

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- シンガポール

- 韓国

- タイ

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Bombardier Inc.

- Cirrus Design Corporation

- Dassault Aviation

- General Dynamics Corporation

- Honda Motor Co., Ltd.

- Textron Inc.

- The Boeing Company

- United Aircraft Corporation

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92731

The Asia-Pacific Business Jet Market size is estimated at 1.71 billion USD in 2025, and is expected to reach 2.37 billion USD by 2030, growing at a CAGR of 6.73% during the forecast period (2025-2030).

The large jet segment is the most prominent, as many business jets are classified as charter, private, or corporate jets

- Business jets are private jets designed to carry small groups of people. They can be used for various other roles as well. As of July 2022, business jets in Asia-Pacific accounted for 6% of the active global fleet. Out of these, the large jet segment accounted for a major market share of 52%, followed by 22% for light jets and 17% for mid-size jets.

- The large jet segment dominates as many business jets fall into charter, private, or corporate use. The UHNWIs are the major users who value these jets primarily due to their range, technology, cabin size, and efficiency. Some of the most delivered jets are Gulfstream G500/550/650/650ER, Global 6000/7500 Express, Challenger 604/605/650, and Dassault Aviation SA's Falcon series.

- During the study period, Cessna (a subsidiary of Textron Inc.) was the major OEM for deliveries in the light jet segment, with 21 jets. Bombardier was the major OEM in the mid-size segment with six jets, followed by Gulfstream Aerospace Corporation, a wholly-owned subsidiary of General Dynamics, with six jets. Gulfstream Aerospace Corporation is a major OEM in the large jet segment, with 97 jets, followed by Bombardier with 45 jets.

- Gulfstream Aerospace Corporation, Bombardier, and Cessna dominate the business jet market, accounting for 60% of the total new business jet deliveries between 2017 and 2022. Out of the total operational business jets in Asia-Pacific, 98% are wholly owned, while the remaining are shared and fractional ownership.

The private aviation industry has experienced a significant boost in demand due to the robust economic recovery in South Asia

- During the COVID-19 pandemic, the reduction in economic activities in the region, along with travel-related restrictions, affected the demand for and utilization of business jets. However, post-pandemic, strong economic recovery and the removal of travel restrictions fueled the demand for private jets, especially in Southeast Asia. Foreign investments surged, especially in Singapore, Thailand, Cambodia, and Malaysia, which resulted in higher demand for private charters. Due to the large customer base, business jet OEMs are primarily targeting this region and are expecting high demand for new business jets over the next decade. In 2022, the region witnessed growth of -10 % compared to 2021.

- The HNWIs and UHNWIs prefer private jets for personal or business travel. The rise in the number of HNWI individuals in the Asia-Pacific region aided in the procurement of new business jets. Compared to 2017, the HNWI population in the region increased by 68% in 2022.

- In terms of the current operational fleet of 1,279 jets in Asia-Pacific, China accounts for 21%, followed by Australia, India, and Japan, with around 17%, 13%, and 9%, respectively. Cessna, Bombardier, and Gulfstream together account for 51% of the current operational business jet fleet in the region. In 2022, China, Australia, and Japan were the major countries in terms of new business jet deliveries.

- Over 362 new business jets are expected to be delivered in the region between 2023 and 2030. The economic recovery in the developing economies in the region, such as China and Southeast Asia, is expected to boost the growth of the business jet market during the forecast period.

Asia-Pacific Business Jet Market Trends

The HNWI population is booming and is expected to be the biggest growth driver for the market

- HNWIs have over USD 1 million in liquid financial assets, while UHNWIs have a net worth of at least USD 30 million. From 2017 to 2022, there was a surge of around 90% in the HNWI population in the region. In 2022, the number of HNWIs in Asia-Pacific increased by 2% compared to 2020.

- Japan witnessed a growth rate of 15% in 2022. The slow growth of the HNWI population in major countries has affected the overall wealth growth in Asia-Pacific. In China, the increase in average wealth led to more than 70% in the number of millionaires. Asia-Pacific is emerging as the leading destination for wealth management and private banking globally, driven by the growing wealth in the region, the increasing HNWI population, and its need for financial advice.

- Factors such as a change in political leadership and low consumption during the pandemic impacted the Japanese Stock market, Nikkei 225, and hampered the growth of HNWIs in the country. Developing countries such as India, Vietnam, and Thailand witnessed growth in HNWIs compared to the leading Asia-Pacific countries. In 202, India witnessed a growth of over 292% in its HNWI population. Thailand and Vietnam witnessed a growth of around 21% and 13%, respectively. High liquidity support by central banks, supportive domestic policy, and stability in the stock markets aided the growth of HNWIs in these countries. Technology, industrial conglomerates, energy, and real estate were the major sectors that accounted for most of the Asia-Pacific HNWI population.

Asia-Pacific Business Jet Industry Overview

The Asia-Pacific Business Jet Market is fairly consolidated, with the top five companies occupying 93.20%. The major players in this market are Airbus SE, Bombardier Inc., Dassault Aviation, General Dynamics Corporation and Textron Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 High-net-worth Individual (hnwi)

- 4.2 Regulatory Framework

- 4.3 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Large Jet

- 5.1.2 Light Jet

- 5.1.3 Mid-Size Jet

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 China

- 5.2.3 India

- 5.2.4 Indonesia

- 5.2.5 Japan

- 5.2.6 Malaysia

- 5.2.7 Philippines

- 5.2.8 Singapore

- 5.2.9 South Korea

- 5.2.10 Thailand

- 5.2.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Bombardier Inc.

- 6.4.3 Cirrus Design Corporation

- 6.4.4 Dassault Aviation

- 6.4.5 General Dynamics Corporation

- 6.4.6 Honda Motor Co., Ltd.

- 6.4.7 Textron Inc.

- 6.4.8 The Boeing Company

- 6.4.9 United Aircraft Corporation

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アジア太平洋地域のビジネスジェット機:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日