欧州のビジネスジェット機市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Business Jet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693577

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

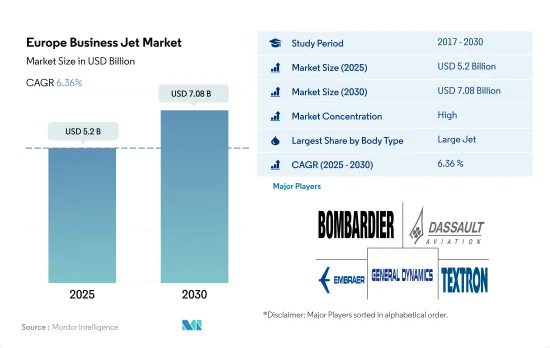

欧州のビジネスジェット機市場規模は2025年に52億米ドルと推定され、2030年には70億8,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは6.36%で成長すると予測されています。

パンデミック後の出張フライト時間の増加がビジネスジェット機への高い需要を生む

- ビジネスジェット機は、欧州のエグゼクティブや企業に小規模空港への直接アクセスを提供し、民間フライトに伴う時間のかかるプロセスを回避します。これらのジェット機によって、多忙なエグゼクティブは生産性を最大限に高め、出張に伴う混乱を軽減することができます。COVID-19の流行は、この地域におけるビジネスジェット機の納入に悪影響を及ぼし、2020年には2021年比で26%減少しました。同地域の富裕層の間では、より安全な移動手段としての自家用飛行機へのシフトが見られ、ビジネスジェット機の調達を後押ししています。しかし、市場はパンデミックから徐々に回復し、2022年には2020年比で34%の成長を記録しました。

- 納入実績では、2017年から2022年にかけて、大型ジェット機セグメントが53%のシェアを占め、次いで小型ジェット機が35%、中型ジェット機が12%でした。同期間中、ビジネスジェット機を最も多く納入したOEMはエンブラエルで、同地域で納入されたジェット機全体の11%を占め、次いでセスナが10%、ボンバルディアが9%、ガルフストリームが7%でした。

- 2022年12月現在の欧州のビジネスジェット機保有台数では、セスナが30%を占め、ボンバルディアが19%、ダッソーが14%と続いた。同地域におけるUHNWI(超富裕層)の急増は、ビジネスジェット機・セグメントを後押しすると予想されます。2023年から2030年の間に約1,244機の航空機が納入される見込みです。

同地域における新規会員の増加とHNWI(富裕層)の増加が、同地域のビジネスジェット機需要を牽引しています。

- 世界の金融、商業、観光のハブとして、欧州のダイナミックなビジネス環境は、ビジネスジェット機が提供する効率性、柔軟性、豪華さに大きく依存しています。2022年12月現在、欧州は世界のビジネスジェット機保有台数の約12%を占めており、ドイツが欧州全体のビジネスジェット機保有台数の18%を占めてこの地域をリードし、英国が約11%、フランスが約9%でこれに続いています。同地域の富裕層の間では、より安全な移動手段として自家用ジェット機への移行が進んでおり、ビジネスジェット機の調達に役立っています。しかし、ワクチン接種率の急速な上昇と国境開放により、2022年には2020年比で28%の成長が記録されました。

- 2023年、エア・チャーター・サービス・プロバイダーは、欧州地域での高い需要とビジネス・アビエーションの新規加盟の急増を目の当たりにしました。2023年5月、ビスタジェット・インターナショナルはVJ25プログラムを欧州、中東・アフリカに導入しました。年間飛行時間が25時間から49時間のフレキシブルなスケジュールを持つ旅行者を対象とし、3年間の定額制で提供されるVJ25は、主力製品である超長距離機ボンバルディア・世界7500を含む世界360機以上のビスタ航空機をオンデマンドで確実に利用できます。

- 欧州のビジネスジェット機需要は、COVID-19パンデミックとロシア・ウクライナ紛争の影響を受け続け、特に中長距離路線では、2022年の大半の期間、多くの地域や国への渡航制限が継続されました。前年同期比で機体数が増加していること、長距離用ジェット機や超軽量ジェット機が増加していることは、欧州の航空会社が欧州域内や域外へのフライトでビジネスジェット機を使用する需要が増加していることの表れです。予測期間中、約1,244機のジェット機が調達される見込みです。

欧州のビジネスジェット機市場動向

HNWI人口の増加が市場の主な成長促進要因に

- HNWI(富裕層)やUHNWI(超富裕層)は、個人旅行や出張のためにプライベートジェットを所有することが多いです。欧州には、民間便では簡単にアクセスできないような、風光明媚で高級な目的地が数多くあります。ビジネスジェット機は、混雑した空港や時間のかかる乗り継ぎを避け、HNWIが遠隔地へ直行する機会を提供します。2022年、欧州のUHNWIの数は2021年に比べ5%増加しました。これは、ユーロ圏の公益事業、ハイテク株、高級品セクターが好調に推移し、堅調な伸びを記録したためです。欧州は2017年から2022年にかけて、世界のHNWI人口の67%を記録し、超富裕層の3番目の大幅な増加を記録しました。

- HNWIの数と資産の面で欧州が主導的地位を占めるのは、主にドイツ、フランス、英国に起因します。2022年には、これら3カ国だけで欧州のHNWI総数の67%を記録しました。HNWI人口はドイツが350万人でトップ、次いでフランスが307万人、英国が290万人となっています。英国はアフリカ、アジア、中東からの富裕層を安定的に惹きつけています。HNWI人口の伸びが最も少なかったのはロシアで、2%を記録しました。これは過去10年間、富裕層が毎年ロシア国外に流出しているためで、ロシアが現在直面している問題の表れです。ウクライナ危機は世界経済、特にインフレと金融市場にリスクをもたらしました。しかし、市場は予測期間中に回復すると予想されます。2030年には、HNWI人口は1,840万人増加すると予想されています。

欧州のビジネスジェット機業界の概要

欧州のビジネスジェット機市場はかなり統合されており、上位5社で98.05%を占めています。この市場の主要企業は以下の通り。 Bombardier Inc., Dassault Aviation, Embraer, General Dynamics Corporation and Textron Inc.(アルファベット順)

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 個人富裕層(hnwi)

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- ボディタイプ

- 大型ジェット機

- 小型ジェット機

- 中型ジェット機

- 国名

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Bombardier Inc.

- Cirrus Design Corporation

- Dassault Aviation

- Embraer

- General Dynamics Corporation

- Pilatus Aircraft Ltd

- Textron Inc.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92727

The Europe Business Jet Market size is estimated at 5.2 billion USD in 2025, and is expected to reach 7.08 billion USD by 2030, growing at a CAGR of 6.36% during the forecast period (2025-2030).

Increase in business travel flight hours after the pandemic generated a high demand for business jets

- Business jets offer European executives and corporations direct access to smaller airports and avoid the time-consuming processes associated with commercial flights. These jets enable busy executives to maximize their productivity and reduce travel-related disruptions. The COVID-19 pandemic adversely impacted business jet deliveries in the region, with a decline of 26% in 2020 compared to 2021. There has been a shift toward private flying as a safer mode of transportation among the HNWI population in the region, aiding in procuring business jets. However, the market gradually recovered from the pandemic, and in 2022, the region recorded 34% growth compared to 2020.

- In terms of deliveries, during 2017-2022, the large jet segment dominated the region with 53% of the share, followed by light and mid-size jets with 35% and 12%, respectively. During the same period, the OEM that delivered most of the business jets was Embraer, with 11% of the total jets delivered in the region, followed by Cessna with 10% of jets delivered, Bombardier delivered 9% of the jets, and Gulfstream delivered 7% of the jets.

- Cessna was the leading OEM, with 30% of the current operational fleet size, followed by Bombardier and Dassault, with 19% and 14%, respectively, in the European business jet fleet as of December 2022. The surge in UHNWI individuals in the region is expected to aid the business jet segment. Around 1,244 aircraft are expected to be delivered between 2023 and 2030.

An increase in new memberships and rising HNWI wealth in the region is driving the demand for business jets in the region

- As a hub for global finance, commerce, and tourism, Europe's dynamic business landscape relies heavily on the efficiency, flexibility, and luxury that business jets provide. As of December 2022, Europe accounted for around 12% of the global business jet fleet, with Germany leading the region with 18% of the total European business jet fleet, followed by the United Kingdom and France, with around 11% and 9%. There has been a shift toward private flying as a safer mode of transportation among the HNWI population in the region, aiding in procuring business jets. However, with the rapid vaccination rates and opening of borders, in 2022, a growth of 28% was recorded compared to 2020.

- In 2023, air charter service providers witnessed high demand in the European region and a surge in new memberships for business aviation. In May 2023, VistaJet International recently introduced its VJ25 program to Europe, the Middle East, and Africa. Aimed at travelers with flexible schedules flying 25 to 49 hours per year and offered as a three-year subscription, VJ25 provides guaranteed on-demand access to the Vista fleet of more than 360 aircraft worldwide, including its flagship ultra-long-range Bombardier Global 7500.

- Business jet demand in Europe continued to be affected by the COVID-19 pandemic and the Russia-Ukraine conflict, especially for medium and long-haul flights, as travel restrictions to many regions and countries remained in place during much of 2022. The Y-o-Y fleet growth and an increasing number of long-range and very light jets are signs of increased demand for European operators to use business jets inside Europe and on flights to destinations outside the region. During the forecast period, around 1,244 jets are expected to be procured.

Europe Business Jet Market Trends

Rise in the HNWI population acting as the major growth driver for the market

- HNWIs and UHNWIs often own private jets for personal or business travel. Europe is home to a multitude of scenic and exclusive destinations that may not be easily accessible through commercial flights. Business jets provide the opportunity for HNWIs to fly directly to remote locations, avoiding congested airports and time-consuming connections. In 2022, the number of UHNWIs in Europe increased by 5% compared to 2021. This was because the Eurozone utilities, tech stocks, and luxury goods sectors performed well, registering solid gains. Europe recorded the third significant rise in the ultra-wealthy population, which recorded 67% of the global HNWI population during 2017-2022.

- The leading position of Europe in terms of the number and assets of HNWIs is mainly attributed to Germany, France, and the United Kingdom. In 2022, these three countries alone recorded 67% of the total HNWIs in Europe. Germany led the HNWI population with 3.5 million HNWIs, followed by France with 3.07 million and the United Kingdom with 2.9 million. The United Kingdom attracts a steady stream of high-net-worth individuals from Africa, Asia, and the Middle East. Russia saw the least growth in the HNWI population, which recorded 2%. This was because well-off people have been moving out of Russia every year for the past 10 years, a sign of the current issues the country is facing. The crisis in Ukraine posed risks to the global economy, especially to inflation and financial markets. However, the market is expected to recover during the forecast period. In 2030, the HNWI population is expected to grow by 18.4 million.

Europe Business Jet Industry Overview

The Europe Business Jet Market is fairly consolidated, with the top five companies occupying 98.05%. The major players in this market are Bombardier Inc., Dassault Aviation, Embraer, General Dynamics Corporation and Textron Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 High-net-worth Individual (hnwi)

- 4.2 Regulatory Framework

- 4.3 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Large Jet

- 5.1.2 Light Jet

- 5.1.3 Mid-Size Jet

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Italy

- 5.2.4 Netherlands

- 5.2.5 Russia

- 5.2.6 Spain

- 5.2.7 Turkey

- 5.2.8 UK

- 5.2.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Bombardier Inc.

- 6.4.2 Cirrus Design Corporation

- 6.4.3 Dassault Aviation

- 6.4.4 Embraer

- 6.4.5 General Dynamics Corporation

- 6.4.6 Pilatus Aircraft Ltd

- 6.4.7 Textron Inc.

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

欧州のビジネスジェット機市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日