イタリアのオペレーションサービスコンサルティング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Italy Operations Service Consulting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 109 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693575

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

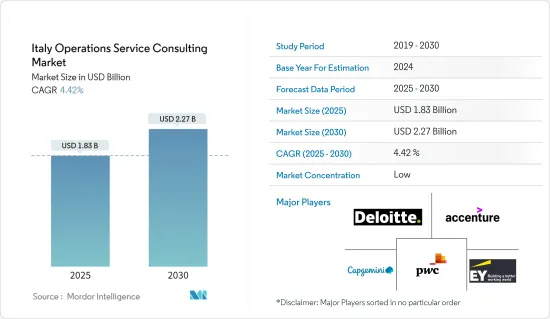

イタリアのオペレーションサービスコンサルティング市場規模は、2025年に18億3,000万米ドルと推計され、2030年には22億7,000万米ドルに達すると予測され、市場推計・予測期間(2025-2030年)のCAGRは4.42%です。

オペレーションマネジメントは、オペレーションコンサルティングと呼ばれることもあり、バリューチェーン全体で企業の内部オペレーションとパフォーマンスを改善するためのアドバイスと実施サービスを提供します。

主なハイライト

- 継続的な技術革新と社会のデジタル化により、イタリアは急速な成長期にあります。変化を受け入れ、機会を発見し、新たな戦略を策定し、計画を明確にし、目標達成のために計画を実行するために、企業はオペレーション・コンサルティング会社という形の戦略的パートナーを必要としています。

- エンドユーザー別に見ると、市場は金融サービス、製造、エネルギー・公益事業、公共部門、小売、その他のエンドユーザーに分けられます。2021年の市場シェアは26.91%で、金融業界が大半を占めています。1990年代を通じて国内の銀行資産の60%を占めていた銀行の合併、買収、資産譲渡、清算、転換により、イタリアの銀行数は激減しました。イタリアには約1000の銀行があります。政府は、イタリアの銀行セクターの国際競争力を高めるため、いくつかのプログラムを通じて統合を推進しています。

- デジタル化が進むと、ユニークなビジネスモデルや戦略をもった新しいビジネスが出現するため、市場は大きな影響を受ける。新しいフリーランスのウェブサイト、バーチャルネットワーク、専門チームの継続的な出現は、クライアントが利用できる選択肢を増やしました。大企業は中小企業と競合します。独立請負業者やゆるやかに確立された専門家ネットワークは、中小企業に負担をかける。海外からの人材流入により、独立請負業者でさえも市場への参入を迫られています。

- 予測期間中、イタリアの公共部門は健全なペースでオペレーションサービスコンサルティングを導入すると予想されます。公共部門は、デジタル技術の破壊的可能性を活用することで、市民、地域社会、労働者、企業を進歩の中心に据えており、同国の市場ベンダーにチャンスをもたらしています。

- イタリア各地の組織は、COVID-19の流行により、地域社会と労働者の安全を守るために必要なあらゆる予防措置を講じた。多くの組織がデジタルトランスフォーメーションを終え、完全なリモートワーク、またはデジタルとオフィスワークを組み合わせたハイブリッドモデルを選択しました。さらに、COVID-19の出現により、サプライチェーンはより脆弱になりました。大半のIT企業にとって、エコシステムは脆弱であり、重要な業務コンサルティング・サービス・プロバイダーで構成されています。また、リモートワークを奨励する法令により、サービスプロバイダーは、ミッションクリティカルな企業顧客が、提供するサービスのスピード、セキュリティ、品質、全体的な有効性を可能にするために必要なツールやテクノロジーへのアクセスを保証するよう求められています。

イタリアのオペレーションサービスコンサルティング市場動向

金融サービス部門が大きなシェアを占める

- 金融機関に影響を及ぼすテクノロジーの急速な進歩により、金融サービス企業は今後ますます、イノベーション、オペレーショナルリスクの低減、コスト削減、顧客ロイヤルティの向上、業績改善、オペレーショナルリスクの低減、コスト削減、顧客に対する魅力的な価値提案の創出が求められるようになります。

- テクノロジーと消費者行動の改善は、イタリアにおける決済セクターの発展を後押しし続けています。金融サービス各社は、変化する決済環境に対応し、可能性をつかむため、オペレーションサービスコンサルティングをいち早く導入しています。これはリテール決済サービス、キャッシュマネジメント、決済テクノロジーに影響を与えます。

- イタリアでは金融サービスのデジタル化が進んでいるため、世界市場のベンダーが金融改革、再編、ターンアラウンド、取引の顧客となっています。例えば、国際的なコンサルティング会社であるFTIコンサルティングは、2022年6月にイタリアでコーポレートファイナンスとリストラクチャリングサービスの提供を拡大しました。イタリアで事業を展開する複数の市場ベンダーは、金融サービスを求める顧客により良いサービスを提供するため、合併・提携業務に取り組んでいます。

- さらに、COVID-19の大流行がイタリアの銀行セクターを大きくデジタル化する原動力となっています。例えば、デジタル・チャネルの利用が増加し、必要な金融サービスをすべて単一のプラットフォームで提供するワンストップショップに対する顧客の嗜好が変化しています。例えば、デジタル決済、オンライン保険、オンラインショッピングのオンライン決済などです。

- 金融分野のコンサルティングサービスを提供するパルヴァ・コンサルティングのような地域コンサルティング会社は、その独創的なサービスで銀行、資産運用、保険業界から大きな関心を集めています。パルヴァ・コンサルティングは、銀行業界における顧客体験と営業効率を向上させるため、流通網を分析し、業務手順を再設計することで、業務品質の時間を確保しています。

- アキュリスグローバルの調査によると、JPモルガンは2021年の合併・買収(M&A)契約においてイタリアでトップの財務アドバイザリー会社でした。取引総額は970億米ドルに迫り、同社は国内のM&A案件のトップアドバイザーとなりました。ゴールドマン・サックス証券は910億米ドルの取引額で2位につけています。

新興テクノロジーへの投資動向の急増

- イタリア政府は、新興企業モデルを構築し、その他欧州の注目を集めようと懸命に努力しています。最近の経済情勢は芳しくないが、起業家を支援する雰囲気は進化しています。かつてイタリアは税金が高いことで知られていました。そのため、多くのイタリア人は、より自由で柔軟性のある場所で起業するために定期的に国を離れていました。政府は、イノベーションとテクノロジーへの支援を強化し、研究と技術移転の促進により大きな権限を与えることで、このサイクルを終わらせることに注力しています。

- 地域の新興企業エコシステムを後押しするため、イタリア政府は10億ユーロ(10億4,000万米ドル)の投資プログラムを導入し、CDPベンチャーキャピタルという名の新しいベンチャー部門を設立しました。CDPベンチャーキャピタルは、アクセラレーターファンド、VCファンドオブファンズ、「シリーズA/Bマッチング」ファンドなど、7種類のファンドを運営しています。また、中小企業や起業家にメンターシップ、ネットワーキング、支援サービスを提供する2つのアクセラレーション・プログラムも開始しました。

- 新しい国家移行計画4.0は、イタリア復興基金の基盤となっています。すべての控除率を強化し、利用を大幅に増やす構造改革に約240億ユーロ(246億米ドル)が投資されます。これは民間投資を増やし、企業に安定性と予測可能性を提供することを目的としています。

- 世界最大級かつ最も包括的な人工知能博士号である「人工知能」の国家博士号が2021年にイタリアで発足しました。イタリアの研究者たちは、CLAIREやELLISといった最も権威あるEUネットワークを含む、世界の主要なAI研究ネットワークすべてに参加しています。また、人工知能に関するグローバルパートナーシップ(GPAI)の創設メンバーの1つでもあります。

- 経済開発省によると、2021年第1四半期のイタリアにおけるビジネスサービス起業数は9,377社でした。製造業、エネルギー、鉱業部門では2,138件の新規起業がありました。ビジネスサービスの起業数が最も多く、運輸・ロジスティクスが最も少なかったのとは対照的です。

イタリアのオペレーションサービスコンサルティング業界概要

イタリアのオペレーションサービスコンサルティング市場は競争が激しく、多くの世界企業や地域企業で構成されています。これらの企業はかなりの市場シェアを占め、世界な顧客基盤の拡大に注力しています。また、研究開発活動、戦略的提携、その他の有機的・無機的成長戦略に注力し、市場においてより強固な地位を維持しています。

- 2022年10月:アーンスト・アンド・ヤングは、テクノロジー、戦略、人材に3年間で100億米ドルを投資し、金融サービス向けのEYネクサスを全世界で正式に発表しました。EYネクサスの立ち上げにより、同社は、金融サービス向けの新製品やソリューションを迅速に展開することを目的としたビジネストランスフォーメーションプラットフォームを導入し、技術的エコシステムの量を拡大しました。

- 2022年9月:アクセンチュアは、世界トップクラスの製造、トレーニング、コンサルティング事業を展開するステランティスの買収計画を発表しました。この買収により、アクセンチュアは顧客向けソリューションにワールドクラス・マニュファクチャリング(WCM)アプローチを取り入れ、生産・サプライチェーンネットワークの有効性、持続可能性、回復力の向上を支援できるようになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 新興テクノロジーへの投資拡大

- BIと高度データ管理戦略の採用

- 市場抑制要因

- コンサルティングマーケットプレースの変化

- ケーススタディ VIS-A-VISオペレーションズ・コンサルティング

第6章 市場セグメンテーション

- エンドユーザー別

- 金融サービス

- 製造業

- エネルギー・公益事業

- 公共部門

- 小売業

- その他エンドユーザー産業

第7章 競合情勢

- 企業プロファイル

- Deloitte Touche Tohmatsu Limited

- Accenture PLC

- PricewaterhouseCoopers LLP

- Ernst & Young ITALY Limited

- Capgemini SE

- KPMG International

- Boston Consulting Group Inc.

- A. T. Kearney Inc.(Kearney)

- Mckinsey & Company Inc.

- Bain & Company Inc.

- Roland Berger GmbH

- Simon-Kucher & Partners

- OC&C Strategy Consultants

第8章 投資分析

第9章 市場の将来

目次

The Italy Operations Service Consulting Market size is estimated at USD 1.83 billion in 2025, and is expected to reach USD 2.27 billion by 2030, at a CAGR of 4.42% during the forecast period (2025-2030).

Operations management sometimes referred to as operations consulting, provides advice and implementation services to improve a company's internal operations and performance across the value chain.

Key Highlights

- Due to continued technological breakthroughs and the digitization of society, Italy is undergoing a rapid growth period. To embrace change, discover opportunities, develop new strategies, articulate a plan, and implement plans to achieve their goals, businesses need strategic partners in the form of operations consulting firms.

- By end-user, the market is divided into financial services, manufacturing, energy and utilities, the public sector, retail, and other end users. With a share of 26.91%, the financial industry controlled most of the market in 2021. Due to bank mergers, acquisitions, asset transfers, liquidations, and conversions that accounted for 60% of all banking assets in the nation throughout the 1990s, the number of banks in Italy has drastically declined. There are about a thousand banks in Italy. The government is promoting consolidation through several programs to make the Italian banking sector more competitive abroad.

- The market is greatly impacted by increased digitization since it makes it possible for new businesses to emerge with unique business models and strategies. The ongoing appearance of new freelancing websites, virtual networks, and specialty teams has increased the options available to clients. Greater firms compete with smaller ones. Independent contractors and loosely established expert networks put a strain on smaller enterprises. Due to the influx of overseas talent, even independent contractors are under pressure to enter the market.

- Over the forecast period, the public sector in Italy is anticipated to adopt operations consulting services at a healthy rate. Public sector organizations are keeping citizens, communities, workers, and businesses at the center of progress by utilizing the disruptive potential of digital technologies, which opens up opportunities for market vendors in the nation.

- Organizations around Italy took all required precautions to safeguard the safety of communities and workers due to the COVID-19 outbreak. Many organizations finished their digital transformation and have chosen to operate entirely remotely or in a hybrid model that combines digital and in-office work. In addition, the emergence of COVID-19 has made supply chains more vulnerable. For the majority of IT firms, the ecosystem is fragile and comprises important operations consulting service providers. Mandates encouraging remote work have also prompted service providers to guarantee that mission-critical corporate clients have access to the tools and technology required to allow the speed, security, quality, and overall effectiveness of services offered.

Italy Operations Service Consulting Market Trends

Financial Service Sector to Hold Significant Share

- Due to the quick technological advancements affecting financial institutions, financial services companies will increasingly need to innovate, reduce operational risk, cut costs, increase customer loyalty, improve business performance, reduce operational risk, reduce costs, and create compelling value propositions for their clients.

- Improvements in technology and consumer behavior continue to propel the development of the payments sector in Italy. Financial services companies are quickly introducing operations consulting services to stay up with the changing payment landscape and seize the possibilities. This has ramifications for retail payments services, cash management, and payments technology.

- Global market vendors are customers for financial transformations, restructurings, turnarounds, and transactions in Italy because of the country's growing digitalization of financial services. For instance, the international consulting company FTI Consulting extended its corporate finance and restructuring service offerings in Italy in June 2022. Several market vendors operating in Italy are engaging in merger and collaboration operations to offer better services to their clients who want financial services.

- Furthermore, the COVID-19 pandemic has driven the banking sector in Italy to undergo significant digital transformation. For instance, the usage of digital channels has increased, along with changing customer preferences toward a one-stop shop with a single platform for obtaining all necessary financial services. Examples include digital payments, online insurance, online payments for online shopping, etc.

- Regional consulting companies like Parva Consulting, which provides consulting services in the financial sector, are attracting much interest from the banking, asset management, and insurance industries with their creative services. To improve customer experience and sales effectiveness in banking, the organization analyses distribution networks and redesigns operational procedures to free up commercial quality time.

- As per research by Acuris Global, JPMorgan was Italy's top financial advisory company for merger and acquisition (M&A) agreements in 2021. With a total deal value close to USD 97 billion, the company became the top advisor to M&A deals in the nation. Goldman Sachs & Co. is placed second in the leaderboard with a deal value of USD 91 billion.

Surged Investment Trends in Emerging Technologies

- The Italian government is working hard to build up its start-up model and draw the rest of Europe's attention to it. Despite the unfavorable recent economic climate, the atmosphere is evolving to support entrepreneurs. Italy used to be known for having high taxes. Hence, many Italians would regularly leave the nation to start their enterprises in places with more freedom and flexibility. The government has been focusing on ending this cycle by increasing its support for innovation and technology and granting greater power to advance research and tech transfer.

- To boost the regional start-up ecosystem, the Italian government introduced a EUR 1 billion (USD 1.04 billion) investment program and established a new venture arm named CDP Venture Capital. This manages seven different funds, including an accelerator fund, a VC fund-of-funds, and "Series A/B matching" funds. It also launched two acceleration programs to provide SMEs and entrepreneurs mentorship, networking, and support services.

- The new National Transition Plan 4.0 serves as the foundation for the Italian Recovery Fund. About EUR 24 billion (USD 24.6 billion) is being invested in a structural change that strengthens all deduction rates and significantly increases usage. It aims to increase private investment and provide businesses with stability and predictability.

- One of the world's biggest and most comprehensive artificial intelligence doctorates, the National Doctorate in "Artificial Intelligence" was launched in Italy in 2021. Italian academics are participating in all key worldwide AI research networks, including the most prestigious EU networks, such as CLAIRE and ELLIS. It is also one of the founding members of the Global Partnership on Artificial Intelligence (GPAI).

- According to the Ministry of Economics Development, the number of business services start-ups in Italy for 1Q 2021 was 9,377. There were 2,138 new start-ups in the manufacturing activities, energy, and mining sector. Business services had the highest number of start-ups, in contrast to transportation and logistics, which had the lowest.

Italy Operations Service Consulting Industry Overview

The Italian operations service consulting market is highly competitive and consists of many global and regional players. These players account for a considerable market share and focus on expanding their global client base. They focus on research and development activities, strategic alliances, and other organic and inorganic growth strategies to stay stronger in the market.

- October 2022: Ernst & Young unveiled the worldwide official launch of EY Nexus for financial services, a three-year, USD 10 billion investment in technology, strategy, and people. With the launch of EY Nexus, the company has expanded the amount of its technological ecosystem by introducing a business transformation platform intended to deploy new products and solutions quickly for financial services.

- September 2022: Accenture announced its plan to acquire Stellantis, a world-class manufacturing, training, and consulting business. By way of this takeover, Accenture could include the World Class Manufacturing (WCM) approach into its solutions for customers, assisting them in improving the effectiveness, sustainability, and resilience of their production and supply chain networks.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Investment in Emerging Technologies

- 5.1.2 Adoption of BI and Advanced Data Management Strategies

- 5.2 Market Restraints

- 5.2.1 Shift in the Consulting Marketplace

- 5.3 Case Studies VIS-A-VIS Operations Consultancy

6 MARKET SEGMENTATION

- 6.1 By End-user

- 6.1.1 Financial Services

- 6.1.2 Manufacturing

- 6.1.3 Energy and Utilities

- 6.1.4 Public Sector

- 6.1.5 Retail

- 6.1.6 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Deloitte Touche Tohmatsu Limited

- 7.1.2 Accenture PLC

- 7.1.3 PricewaterhouseCoopers LLP

- 7.1.4 Ernst & Young ITALY Limited

- 7.1.5 Capgemini SE

- 7.1.6 KPMG International

- 7.1.7 Boston Consulting Group Inc.

- 7.1.8 A. T. Kearney Inc. (Kearney)

- 7.1.9 Mckinsey & Company Inc.

- 7.1.10 Bain & Company Inc.

- 7.1.11 Roland Berger GmbH

- 7.1.12 Simon-Kucher & Partners

- 7.1.13 OC&C Strategy Consultants

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 109 Pages

- 納期

- 2~3営業日