北米の軍用ヘリコプター:市場シェア分析、産業動向、成長予測(2025~2030年)

North America Military Helicopters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 146 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693571

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

北米の軍用ヘリコプター市場規模は2025年に33億7,000万米ドルと推定・予測され、2030年には35億9,000万米ドルに達し、予測期間(2025~2030年)のCAGRは1.27%で成長すると予測されます。

地政学的課題と防衛予算の増加がロータークラフト市場の促進要因

- 北米全体での国防費の増加は、軍用ヘリコプター市場に大きな影響を与えています。各国政府は、ヘリコプターのアップグレードなど、軍事力の近代化に多額の予算を割いています。戦争の性質が進化するにつれて、国防費は最新のアビオニクス、センサ、兵器を装備した最先端のヘリコプターの獲得に向けられています。北米の国防費は2021年から約1%急増し、2022年には9,040億米ドルに達します。

- さらに、米国、カナダ、メキシコは多くの地政学的課題に直面し、対テロ作戦を行っています。したがって、これらの国々は、これらの脅威に効果的に対応するために航空能力を強化しようとしており、これが軍用ヘリコプターの需要に寄与しています。2022年現在、北米で使用されている回転翼機は米国が92%を占め、カナダが2%、メキシコが3%、その他の中東・アフリカが3%となっています。最も多く調達されたヘリコプターの機種は、AH-64アパッチ攻撃ヘリコプター824機、CH-47D/F/MH-47G 513機以上、H145(UH-72A/B)383機、S-70/EH/H/MH/UH-60 2,312機、MV-22 289機、S-70/MH-60R/S 489機です。

- 国境警備を改善し、最先端の兵器や技術を購入するため、この地域のいくつかの国は軍事予算を増額しており、これは将来の軍用回転翼航空機の調達拡大に役立つ可能性があります。例えば、米国は2023年に、CH-47チヌーク、UH-60ブラックホーク、CH-53K、AH-1Z、MH-139Aを含む119機の回転翼航空機の調達を計画しています。メキシコ政府は、メキシコ空軍用に11機(H225M 4機、UH-60M 7機)のヘリコプターを発注しました。これらの進歩の結果、この地域の国々は588機の回転翼機を納入する見込みです。

国防予算の増加と地政学的紛争が、この地域のヘリコプター調達需要を牽引

- 北米諸国、特に米国は、地政学的紛争に対抗するため、先進的なヘリコプターをいち早く開発してきました。南北アメリカ地域の軍事費の94%近くは北米からのものです。2022年、同地域の国防費は総額9,120億米ドルに達しました。北米の軍事費の大部分は米国(96%)が占め、カナダが3%、メキシコが1%と続きます。

- 軍事予算の増加に伴い、同地域の各国は今後、軍用回転翼機の調達拡大を促進する可能性があります。2023年、米国はCH-47チヌーク、UH-60ブラックホーク、CH-53K、AH-1Zを含む119機の回転翼機を購入する予定です。メキシコ政府はメキシコ空軍用に11機のヘリコプター(H225M 4機、UH-60M 7機)を発注しました。

- 2022年現在、北米が保有する回転翼機は、全世界の回転翼機総数の約29%を占めています。その内訳は、マルチミッションヘリコプターが38%、輸送ヘリコプターが58%、その他のヘリコプターが4%となっています。次いでメキシコが3%の固定翼機を運航しており、そのうち56%がマルチミッションヘリコプター、39%が輸送用ヘリコプター、31%がその他のヘリコプターです。カナダはメキシコに次いで固定翼機を2%保有し、そのうち64%がマルチミッションヘリコプター、21%が輸送用ヘリコプター、16%がその他のヘリコプターです。

- 現在進行中の調達と近代化計画により、米国は引き続き市場をリードし、新型回転翼機の大きな需要を生み出す可能性があります。予測期間中、同国では合計588機の航空機が調達される見込みです。

北米の軍用ヘリコプター市場の動向

地政学的脅威が同地域の防衛費増加の主因

- 2022年、米国は世界の国防支出の39%を占める軍事支出は2022年に8,770億米ドル(0.7%)増加。この合計には、199億米ドルと推定されるウクライナへの軍事援助が含まれます。2022年、米国は空軍省予算を発表し、2023年度の予算要求額は約202億米ドル、2022年度の要求額から11.7%増の約1,940億米ドルと概算しました。この予算には、航空機の研究開発、航空機の取得、初期予備品、航空機の支援装備が含まれます。2023年度の資金には、F-35 61機、F-15EX 24機、兵站支援機79機、回転翼機119機、UAV/UAS 12機の購入が含まれます。

- 過去数年間、カナダは安全保障上の懸念の高まりに対処し、軍備を近代化するために国防支出を増やすというコミットメントも示してきました。カナダは、従来の防衛能力を維持しつつ、サイバー戦争や非対称的な課題といった新たな脅威に適応する必要性を認識しています。カナダの2022年の軍事費は269億米ドルで、前年比3.0%増でした。政府支出全体のうち、軍事費に割り当てられた割合は1.2%です。2022年予算案によると、政府は今後5年間でカナダの国防に80億米ドル以上の新たな資金を提供すると発表しています。

- メキシコでは、犯罪行為に対抗するための軍事力の使用が、サブリージョンにおける軍事支出の主要原動力となっています。2022年のメキシコの国防支出は85億米ドルで、2021年に比べて9.7%減少しました。国家警備隊への支出は2021年に35%増加し、軍事費全体の16%を占めました。2022年の国防費はGDPの0.6%でした。

艦隊の近代化と航空機の近代化ニーズの高まりが北米の促進要因

- 2022年12月現在、北米では13,676機の航空機とヘリコプターが活躍しています。中国と米国は、将来の戦争に備えるため、新興技術の研究開発にますます力を入れており、技術面での競合が加速しています。米国は、この地域でも世界でも最大の軍用機保有国であり、合計1万3,300機が運用されています。この艦隊のかなりの部分は、戦闘ヘリコプター(42%)と戦闘機(21%)で占められています。一方、訓練機とヘリコプターは20%を占め、輸送機はわずか7%にすぎないです。一方、タンカーと特殊任務機はそれぞれ5%を占めています。

- 2022年末までに、カナダは約356機の航空機と回転翼機を保有することになります。これら356機のうち、最も多く調達されているのは訓練機/ヘリコプターで132機、次いで戦闘ヘリコプター120機、戦闘機63機、輸送機28機、特殊任務機27機、タンカー6機となっています。カナダは、2032年までに退役が予定されているCF-18戦闘機の後継機としてF-35を選定しました。F-35の契約が成立すれば、カナダは2025年に新型機の調達を開始する予定です。メキシコは2022年12月現在、468機の航空機を保有しています。この合計468機のうち、最も多く調達されているのは訓練機で、ヘリコプターが203機、次いで戦闘ヘリコプター157機、輸送機46機、特殊任務機25機、戦闘機36機となっています。同国は国際犯罪組織や麻薬カルテルが大部分を占めているため、麻薬密売組織と戦うために軍用ヘリコプターを活用しています。

北米の軍用ヘリコプター産業概要

北米の軍用ヘリコプター市場はかなり統合されており、上位5社で99.96%を占めています。この市場の主要企業は、Airbus SE、Leonardo S.p.A、Lockheed Martin Corporation、Textron Inc.、The Boeing Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 国内総生産

- アクティブフリートデータ

- 国防支出

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- 機体タイプ

- マルチミッションヘリコプター

- 輸送用ヘリコプター

- その他

- 国

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Leonardo S.p.A

- Lockheed Martin Corporation

- MD Helicopters LLC.

- Textron Inc.

- The Boeing Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92665

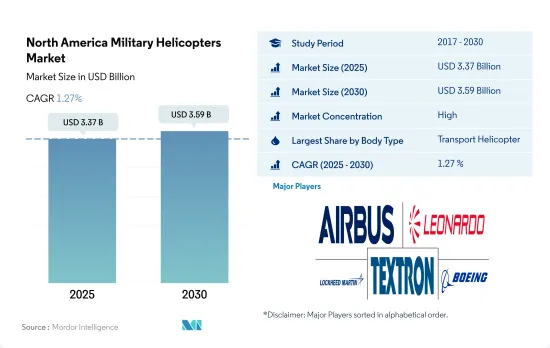

The North America Military Helicopters Market size is estimated at 3.37 billion USD in 2025, and is expected to reach 3.59 billion USD by 2030, growing at a CAGR of 1.27% during the forecast period (2025-2030).

Geopolitical challenges and rising defense budgets are the driving factors of the rotorcraft market

- The increase in defense spending across North America has significantly impacted the military helicopter market. Governments are allocating substantial resources to modernize their military capabilities, including upgrading helicopter fleets. As the nature of warfare evolves, defense spending is being directed toward acquiring cutting-edge helicopters equipped with the latest avionics, sensors, and weaponry. The defense expenditure of North America surged around 1% from 2021 to USD 904 billion in 2022.

- Additionally, the United States, Canada, and Mexico face numerous geopolitical challenges and perform counter-terrorism operations. Hence, these countries seek to enhance their aerial capabilities to respond effectively to these threats, which has contributed to the demand for military helicopters. As of 2022, in terms of the active fleet, the US accounted for 92% of the total rotorcraft in North America, while Canada, Mexico, and the Rest of North America accounted for 2%, 3%, and 3%, respectively. Some of the most procured helicopter models are 824 AH-64 Apache attack helicopters and over 513 CH-47D/F/MH-47G, 383 H145 (UH-72A/B), 2,312 S-70/EH/HH/MH/UH-60, 289 MV-22, and 489 S-70/MH-60R/S.

- To improve border security and buy cutting-edge weaponry and technologies, several countries in the region have increased their military budget, which may aid the future expansion of military rotorcraft procurement. For instance, in 2023, the United States planned to procure 119 rotorcraft, including CH-47 Chinook, UH-60 Black Hawk, CH-53K, AH-1Z, and MH-139A. The Mexican government ordered 11 helicopters (four H225M and seven UH-60M) for its Mexican Air Force. As a result of these advancements, the countries in the region are expected to take delivery of 588 rotorcraft.

Rising defense budgets and geopolitical conflicts are driving the demand for helicopter procurement in the region

- Countries in North America, particularly the United States, have been among the first to develop advanced helicopters to counter geopolitical conflicts. Nearly 94% of the military expenditures in the Americas region come from North America. In 2022, the region's defense expenditure totaled USD 912 billion. North America's military expenditures were largely accounted for by the United States (96%), followed by Canada and Mexico, with 3% and 1%, respectively.

- With increased military budgets, various countries in the region may facilitate the expansion of military rotorcraft procurement in the future. In 2023, the United States plans to purchase 119 rotorcraft, including the CH-47 Chinook, the UH-60 Black Hawk, the CH-53K, and the AH-1Z. The Mexican government ordered 11 helicopters (four H225M and seven UH-60M) for the Mexican Air Force.

- As of 2022, in terms of active fleet size, North America held approximately 29% of the total rotorcraft worldwide. Out of the entire region, the United States stood first, operating 92% of rotorcraft, of which 38% are multi-mission helicopters, 58% are transport helicopters, and 4% are other helicopters. The country was followed by Mexico, which operates 3% of fixed-wing aircraft, of which 56% are multi-mission helicopters, 39% are transport helicopters, and 31% are other helicopters. Canada followed Mexico, operating 2% of fixed-wing aircraft, of which 64% are multi-mission helicopters, 21% are transport helicopters, and 16% are other helicopters.

- With the ongoing procurements and modernization plans, the United States may continue to lead the market and generate significant demand for new rotorcraft. During the forecast period, a total of 588 aircraft are expected to be procured by the country.

North America Military Helicopters Market Trends

Geopolitical threats are the main reason behind the increase in defense spending in the region

- In 2022, the US accounted for 39% of global defense spending military spending increased by USD 877 billion in 2022, or 0.7%. The total includes military assistance to Ukraine, estimated at USD 19.9 billion. In 2022, the US released the Department of the Air Force budget, which outlined that for FY 2023, the budget request is approximately USD 194.0 billion, a USD 20.2 billion or 11.7% increase from the FY 2022 request. This funding includes aircraft R&D, aircraft acquisition, initial spares, and aircraft support equipment. The funding for FY 2023 includes the purchase of 61 F-35, 24 F-15EX, 79 logistics and support aircraft, 119 rotary wing aircraft, and 12 UAV/UAS.

- Over the past few years, Canada also has demonstrated a commitment to increase defense spending to address growing security concerns and modernize its military equipment. The country recognizes the need to adapt to emerging threats, such as cyber warfare and asymmetric challenges, while maintaining conventional defense capabilities. Canada spent USD 26.9 billion on its military in 2022, which was 3.0 % higher than the previous year. Out of the total government spending, the country has allocated 1.2% of its share to the military. As per the Budget 2022, the announcement government will offer more than USD 8 billion for new funding to Canada's national defense over the next five years.

- In Mexico, the use of military forces to combat criminal activity remains the primary driver of military spending in the sub-region. Mexico's defense spending in 2022 was USD 8.5 billion, a decrease of 9.7% compared to 2021. Spending on the National Guard increased by 35% in 2021, accounting for 16% of total military spending. The country's defense expenditure was 0.6% of its GDP in 2022.

Fleet modernization and the rising need for modernization of aircraft are the driving factors in North America

- As of December 2022, North America had an active fleet of 13,676 aircraft and helicopters. Competition in technology is accelerating between China and the United States as both countries are increasingly focused on the R&D of emerging technologies to prepare for future warfare. The United States has the biggest fleet of military aircraft in the region and globally, with a total of 13,300 operational fleets. A considerable chunk of this fleet is made up of combat helicopters (42%) and combat planes (21%). In contrast, training planes and helicopters account for 20%, while transport planes make up only 7%. Meanwhile, tankers and special mission aircraft each represent 5% of the fleet.

- By the end of 2022, Canada had an active fleet of about 356 aircraft and rotorcraft. Of these total 356 aircraft, the most procured fleet is training aircraft/helicopters, accounting for 132, followed by 120 combat helicopters, 63 combat aircraft, 28 transport aircraft, 27 special mission aircraft, and 6 tanker aircraft. Canada has selected F-35s to replace its CF-18 fighter jets, which are scheduled to retire by 2032. If the F-35 deal is finalized, Canada plans to start procuring the new jets in 2025. Mexico had an active fleet of 468 aircraft as of December 2022. Of these total 468 aircraft, the most procured fleet is training aircraft, and helicopters accounted for 203 aircraft, followed by 157 combat helicopters, 46 transport aircraft, 25 special mission aircraft, and 36 combat aircraft. As transnational criminal organizations and drug cartels largely occupy the country, the country utilizes military helicopters to fight drug traffickers.

North America Military Helicopters Industry Overview

The North America Military Helicopters Market is fairly consolidated, with the top five companies occupying 99.96%. The major players in this market are Airbus SE, Leonardo S.p.A, Lockheed Martin Corporation, Textron Inc. and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Gross Domestic Product

- 4.2 Active Fleet Data

- 4.3 Defense Spending

- 4.4 Regulatory Framework

- 4.5 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Multi-Mission Helicopter

- 5.1.2 Transport Helicopter

- 5.1.3 Others

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 Mexico

- 5.2.3 United States

- 5.2.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Leonardo S.p.A

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 MD Helicopters LLC.

- 6.4.5 Textron Inc.

- 6.4.6 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

北米の軍用ヘリコプター:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 146 Pages

- 納期

- 2~3営業日