中東・アフリカの軍用ヘリコプター:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Middle East and Africa Military Helicopters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693561

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

中東・アフリカの軍用ヘリコプター市場規模は2025年に12億5,000万米ドルと推計され、2030年には14億7,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは3.32%で成長する見込みです。

地政学的課題と国防予算の増加がこの地域の軍用回転翼機の促進要因

- この地域の軍隊は、軍事的優位性を得るために、ヘリコプターの能力を最先端技術で近代化しています。予測期間中、マルチミッションヘリコプターが市場の主要シェアを占めると予想されます。マルチミッションヘリコプターは、地上部隊に近接航空支援を行ったり、敵の装甲を破壊する対戦車作戦を行ったりすることができます。この地域の軍隊はこうした能力を必要としており、マルチミッションヘリコプターの調達を後押ししています。

- 中東・アフリカ地域では現在、3,118機の戦闘ヘリコプターが運用されています。474機のヘリコプターを運用するトルコは、この地域で最も多くの戦闘ヘリコプターを保有しています。トルコに次いでエジプトが313機、アルジェリアが276機の戦闘ヘリコプターを保有しています。

- 予測期間中、トルコ、アルジェリア、エジプトがヘリコプターの大半を購入すると予想されます。エジプトは2024年までにEW-149マルチミッションヘリコプターを24機購入する予定です。アルジェリアは2024年までにMi-28攻撃ヘリコプタ42機の購入を計画しています。トルコでは、109機のS-70ユーティリティ・ヘリコプターを含め、約160機のヘリコプターが購入される見込みです。2026年までに、すべてのヘリコプターが引き渡される予定です。

- 2018年初め、アラブ首長国連邦はボーイング社とアパッチAH-64E攻撃ヘリコプター17機の調達について2億4,200万米ドルの契約を結び、2023年までに引き渡される見込みです。トルコは現在、前身のT129 ATAKよりも軽量な総排気量6トンの新型T629攻撃ヘリコプターを開発中です。2020年後半までに、トルコ航空宇宙産業はATAK FAZ 2ヘリコプターの納入を開始しました。

老朽化が進む機体のアップグレードや機体更新プログラムの需要が、市場の成長を後押しすると予想される

- 中東の国防支出は2022年には約1,840億米ドルとなり、2022年比で3.2%以上減少しました。アフリカの2022年の国防費は約394億米ドルで、2021年比で5%以上減少しました。

- 湾岸地域は、域内諸国間の地理的緊張のため、引き続き断片化されています。サウジアラビア、エジプト、カタール、アラブ首長国連邦、アルジェリアは、世界の主要武器輸入国です。また、回転翼機分野では、戦闘ヘリコプターや実用ヘリコプターの調達計画を積極的に進めています。これらの国々は、予測期間中にフリートのアップグレードのために新型の回転翼機を調達すると予想されます。

- 2022年には、回転翼機はこの地域の航空機納入数全体の41%を占めています。2017~2021年の主な調達には、UAEによるボーイングのAH-64E戦闘ヘリコプター、サウジアラビアによるCH-47Fチヌーク大型ヘリコプター48機の調達があります。

- 2017年から2021年にかけて、現役の回転翼機保有数は中東で約4%、アフリカで約6%増加しました。この成長は、地域大国のあからさまな介入と、イラン、サウジアラビア、アラブ首長国連邦の間で進行中の紛争によってもたらされました。米国、フランス、ロシアは、この地域におけるロータークラフトの主要供給国です。主要国とは別に、モロッコやナイジェリアなどの小国も、アルジェリアとの緊張状態が続いているため、防衛予算を増やしています。こうしたすべての要因が、予測期間中に同地域の各種軍事用回転翼機への支出を促進すると予想されます。2023年から209年にかけて、この地域では約514機の回転翼機が納入される見込みです。

中東・アフリカの軍用ヘリコプター市場の動向

同地域の主要軍事大国は国防費を急増

- 中東地域の2022年の国防費は約1,840億米ドルで、2021年と比較して3.2%以上減少しました。一方、アフリカでは2022年に約394億米ドルで、2021年から5%以上減少しました。サウジアラビア、エジプト、カタール、アラブ首長国連邦、アルジェリアといった国々は、2017年から22年にかけて国防支出が多かった地域の主要国です。これらの国々は、固定翼セグメントのマルチロール機や実用機の積極的な調達プログラムを持っています。

- サハラ以南のアフリカの軍事費の合計は、2022年に203億米ドルとなり、2021年比で7.3%、2013年比で18%減少しました。同地域の2大支出国であるナイジェリアと南アフリカが、2022年の軍事費減少を主導しました。2022年、イスラエルの軍事費は2009年以来初めて減少しました。総額234億米ドルは2021年より4.2%減少しました。

- サウジアラビアの軍事費の前年比(YoY)成長率は、2022年には2021年比で16%増となり、2018年以来の前年比増となりました。サウジアラビアの昨年の軍事費は750億米ドルと見積もられていました。この削減は、サウジアラビアがイエメンから軍人を撤収させ始めたという非難と重なりました。しかし、サウジ政府はこの疑惑を否定し、人員は再配置されているだけだと主張しました。2015年以来、サウジアラビアは戦争で荒廃したイエメンに対する軍事作戦で連合国を率いており、戦闘は2022年まで続いた。サウジアラビアの軍事予算はGDP比7.4%と、2022年のウクライナに次いで世界第2位でした。

旧式航空機の代替計画が中東軍事航空の主な原動力になると予測される

- 2022年現在、中東・アフリカの現役航空機保有数は9,460機。同地域の総活動航空機保有数は、2017年と比較して1%増加しました。南アフリカ、アルジェリア、アラブ首長国連邦、サウジアラビア、トルコ、エジプト、カタールは、この地域の総アクティブフリートの58%を占めました。

- 中東では、2022年の国防費は1,570億米ドルとなり、それぞれ2020年から8.6%、2012年から5.6%増加しました。北アフリカが49%を占めるのに対し、サハラ以南のアフリカは総支出の51%を占める。

- サウジアラビア、カタール、アラブ首長国連邦などの国々は、近代戦の需要を満たすために航空機保有数を拡大しています。予測期間中も、次世代航空機の生産と取得を継続する可能性があります。地域の軍隊はまた、外部の脅威に対する軍事的優位性を獲得するために、最先端技術を駆使してヘリコプターの能力を強化しています。

- アフリカの現役機体数は、2017年と比較して2022年には1%減少しました。南アフリカ、アルジェリア、エジプトがアフリカの総フリートの45%を占めています。アルジェリアやエジプトのような主要国が約100機の航空機調達を計画しているため、今後数年間で保有機数は増加する可能性があります。中東・アフリカのアクティブ・フリートは、2017年と比較して8%増加しました。中東では、サウジアラビア、アラブ首長国連邦、カタール、トルコが総フリートの59%を占めています。予測期間中、アラブ首長国連邦、カタール、トルコのような国々が約400機の航空機調達を計画しているため、この地域の現役航空機保有数は増加する可能性があります。

中東・アフリカ軍用ヘリコプター産業の概観

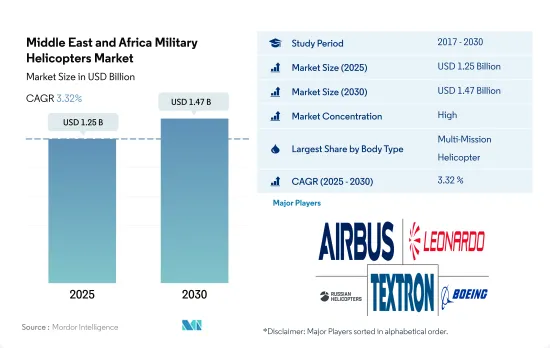

中東・アフリカの軍用ヘリコプター市場はかなり統合されており、上位5社が100%を占めています。この市場の主要企業は以下の通り。 Airbus SE, Leonardo S.p.A, Russian Helicopters, Textron Inc. and The Boeing Company(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 国内総生産

- アクティブフリートデータ

- 国防支出

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- 機体タイプ

- マルチミッションヘリコプター

- 輸送用ヘリコプター

- その他

- 国名

- アルジェリア

- エジプト

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他中東とアフリカ

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Leonardo S.p.A

- Lockheed Martin Corporation

- Robinson Helicopter Company Inc.

- Russian Helicopters

- Textron Inc.

- The Boeing Company

- Turkish Aerospace Industries

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Middle East and Africa Military Helicopters Market size is estimated at 1.25 billion USD in 2025, and is expected to reach 1.47 billion USD by 2030, growing at a CAGR of 3.32% during the forecast period (2025-2030).

Geopolitical challenges and rising defense budgets are the driving factors of military rotorcraft in the region

- The regional armed forces are modernizing the capabilities of helicopters with cutting-edge technologies to gain a military edge. During the forecast period, multi-mission helicopters are expected to hold the major share of the market. Multi-mission helicopters can provide close air support to ground troops and conduct anti-tank operations to destroy enemy armor. The armed forces in the region require these capabilities, aiding the procurement of multi-mission helicopters.

- There are currently 3,118 combat helicopters in operation in the Middle East & Africa. With a 474-helicopter operational force, Turkey possesses the most combat helicopters in the region. Egypt and Algeria have active fleets of 313 and 276 combat helicopters, respectively, after Turkey.

- Turkey, Algeria, and Egypt are anticipated to purchase most of the helicopters throughout the forecast period. Egypt plans to buy 24 EW-149 multi-mission helicopters by 2024. By 2024, Algeria plans to purchase 42 Mi-28 attack helicopters. Around 160 helicopters will likely be purchased by Turkey, including 109 S-70 utility helicopters. By 2026, all the helicopters are expected to be delivered.

- Earlier in 2018, the United Arab Emirates signed a USD 242 million contract with The Boeing Company for the procurement of 17 Apache AH-64E attack helicopters, which are expected to be delivered by 2023. Turkey is currently developing a new T629 attack helicopter, with a total displacement of six tons, lighter than its T129 ATAK predecessor. By the second half of 2020, Turkish Aerospace Industries started delivering ATAK FAZ 2 helicopters.

The demand for fleet upgradation and fleet replacement programs for the growing aging fleet is expected to aid the market growth

- The defense expenditure in the Middle East was around USD 184 billion in 2022, with a decline of over 3.2% compared to 2022. It was around USD 39.4 billion in Africa in 2022, with a decline of over 5% from 2021.

- The Gulf region continues to be fragmented due to geographic tensions between the countries in the region. Saudi Arabia, Egypt, Qatar, the UAE, and Algeria are the major arms importers globally. They also have active programs for procuring combat and utility helicopters in the rotorcraft segment. These countries are expected to procure newer rotorcraft for fleet upgradation during the forecast period.

- In 2022, the rotorcraft accounted for 41% of the overall aircraft deliveries in the region. Some major procurements during 2017-2021 were Boeing's AH-64E combat helicopters by the UAE and the procurement of 48 CH-47F Chinook heavy-lift helicopters by Saudi Arabia.

- During 2017-2021, the active rotorcraft fleet grew by around 4% in the Middle East and 6% in Africa. This growth was driven by the overt intervention of regional powers and ongoing conflicts between Iran, Saudi Arabia, and the UAE. The US, France, and Russia are the major supplier nations of rotorcraft in this region. Apart from the major countries, small countries such as Morocco and Nigeria are also increasing their defense budgets due to the ongoing tensions with Algeria. All such factors are expected to drive the spending on various types of military rotorcraft in the region during the forecast period. During 2023-209, around 514 rotorcraft are expected to be delivered in the region.

Middle East and Africa Military Helicopters Market Trends

Major military powers in the region have surged their defense expenditure

- Defense expenditures in the Middle Eastern region were around USD 184 billion in 2022, a decline of over 3.2% compared to 2021. In contrast, it was around USD 39.4 billion in Africa in 2022, with a decline of over 5% from 2021. Countries such as Saudi Arabia, Egypt, Qatar, United Arab Emirates, and Algeria were the major countries in the region with a high defense expenditure during 2017-22. They have active procurement programs for multi-role and utility aircraft in fixed-wing segments.

- Sub-Saharan Africa's combined military expenditure stood at USD 20.3 billion in 2022, down by 7.3% compared to 2021 and 18% compared to 2013. Nigeria and South Africa, the sub-regions two largest spenders, led the decline in military spending in 2022. In 2022, Israel's military spending fell for the first time since 2009. Its total of USD 23.4 billion was 4.2% lower than in 2021.

- The year-on-year (Y-o-Y) growth in Saudi Arabia's military spending was 16% in 2022 compared to 2021, the first Y-o-Y increase since 2018. Saudi Arabia's military expenditure was estimated at USD 75.0 billion last year. The reduction coincided with accusations that Saudi Arabia had started to remove its military personnel from Yemen. However, the Saudi government denied the allegations and insisted that the personnel were just being redeployed. Since 2015, Saudi Arabia has been leading a coalition in a military campaign against the war-torn nation of Yemen, and the fighting continued into 2022. Saudi Arabia had the second-largest military budget in the world, at 7.4% of GDP, after Ukraine in 2022.

Fleet replacement programs for older aircraft are projected to be the main driver for Middle Eastern military aviation

- As of 2022, the Middle East & Africa had an active fleet of 9,460 aircraft. The total active aircraft fleet increased by 1% in the region compared to 2017. South Africa, Algeria, the United Arab Emirates, Saudi Arabia, Turkey, Egypt, and Qatar accounted for 58% of the total active fleet in the region.

- In the Middle East, defense spending in 2022 totaled USD 157 billion, an increase of 8.6% from 2020 and 5.6% from 2012, respectively. While North Africa accounted for 49%, Sub-Saharan Africa accounted for 51% of the total spending.

- Countries such as Saudi Arabia, Qatar, and the United Arab Emirates are expanding their aircraft fleet size to fulfill the demands of modern warfare. They may continue to produce and acquire next-generation aircraft during the forecast period. The regional armed forces are also enhancing the capabilities of helicopters with cutting-edge technology to obtain military superiority over the external threat.

- Africa's active fleet size decreased by 1% in 2022 compared to 2017. South Africa, Algeria, and Egypt accounted for 45% of the total fleet in Africa. The fleet may increase in the coming years as major countries like Algeria and Egypt plan to procure around 100 aircraft. The Middle East & Africa's active fleet increased by 8% compared to 2017. Saudi Arabia, the United Arab Emirates, Qatar, and Turkey accounted for 59% of the total fleet in the Middle East. During the forecast period, the active aircraft fleet may increase in the region as countries like the United Arab Emirates, Qatar, and Turkey plan to procure around 400 aircraft.

Middle East and Africa Military Helicopters Industry Overview

The Middle East and Africa Military Helicopters Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are Airbus SE, Leonardo S.p.A, Russian Helicopters, Textron Inc. and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Gross Domestic Product

- 4.2 Active Fleet Data

- 4.3 Defense Spending

- 4.4 Regulatory Framework

- 4.5 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Multi-Mission Helicopter

- 5.1.2 Transport Helicopter

- 5.1.3 Others

- 5.2 Country

- 5.2.1 Algeria

- 5.2.2 Egypt

- 5.2.3 Qatar

- 5.2.4 Saudi Arabia

- 5.2.5 United Arab Emirates

- 5.2.6 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Leonardo S.p.A

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 Robinson Helicopter Company Inc.

- 6.4.5 Russian Helicopters

- 6.4.6 Textron Inc.

- 6.4.7 The Boeing Company

- 6.4.8 Turkish Aerospace Industries

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日