|

市場調査レポート

商品コード

1693409

軍用ヘリコプター:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Military Helicopters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 軍用ヘリコプター:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 334 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

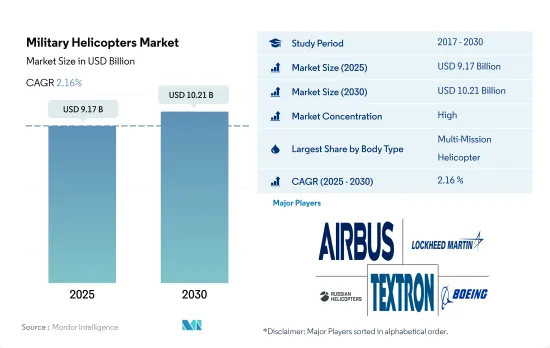

軍用ヘリコプター市場規模は2025年に91億7,000万米ドルと推定・予測され、2030年には102億1,000万米ドルに達し、予測期間(2025~2030年)のCAGRは2.16%で成長すると予測されます。

軍用ヘリコプター市場全体では、さまざまな新たな脅威に対抗するため、マルチミッションヘリコプターのセグメントが最も高い需要を生み出すと予想されます。

- 軍事紛争、テロ、国境紛争、領土侵犯、違反行為の増加により、回転翼機の使用が増加しています。また、多くの地域の軍事が、敵対勢力に対して軍事的に優位に立つために、ヘリコプターを最先端技術でアップグレードしています。マルチミッションヘリコプターは、部隊への近接航空支援や敵の装甲の破壊に加え、対戦車任務にも使用できます。

- 過去では、マルチミッションヘリコプターが最も多く調達され、軍用ヘリコプター全体の49%を占め、次いでその他の回転翼機(実用ヘリコプター、海上ヘリコプター、対潜水艦戦用ヘリコプター、訓練用ヘリコプター)、輸送ヘリコプターがそれぞれ37%、13%のシェアを占めました。同期間に最も多く調達された回転翼機はUH-60シリーズで409機、次いでAH-1Zが180機、CH-47D/Fが173機でした。

- さらに、軍用ヘリコプターの需要は、非対称的な脅威と複雑な作戦環境を特徴とする現代戦争の性質の変化によって、適応性と柔軟性の高いプラットフォームが必要とされるようになったことなど、いくつかの要因によって促進されてきました。また、従来型と非従来型のハイブリッド戦術の台頭も、先進的ISR能力を備えたヘリコプターの需要を高めています。このような要因が軍用機調達の需要を促進すると予想されます。予測期間中、世界全体で合計2,854機の回転翼航空機が納入される見込みです。

国防予算の増加に伴う地政学的脅威の高まりが市場を牽引

- 世界の軍用ヘリコプター市場は、防衛予算の増加、安全保障上の脅威の進化、ヘリコプター技術の進歩などを背景に、ここ数年で大きく成長しています。軍用ヘリコプターは、迅速な輸送、近接航空支援、戦闘能力を提供し、現代の戦争において極めて重要です。

- 2022年、ロシアとウクライナの戦争は、各国の国防予算をさらに煽り、世界的に軍事の作戦準備態勢を再評価する必要性を高めました。世界の軍事費は2022年に3.7%増加し、過去最高の2兆2,400億米ドルに達しました。ロシアのウクライナ侵攻は、2022年の支出増加の主要因でした。2022年の5大支出国は米国、中国、ロシア、インド、サウジアラビアで、これらを合わせると世界の軍事費の63%を占めます。

- 2017~2022年の軍用ヘリコプター調達では、北米が市場を独占しており、主に米国がヘリコプター全体の38%を占めています。米国は世界最大の軍用ヘリコプター保有国であり、世界シェアの32%を占めています。アジア太平洋も重要な市場であり、中国やインドなどの国々の防衛予算の増加により、25%のシェアを占めています。欧州は、ロシア、フランス、ドイツ、英国といった国々がヘリコプター近代化計画に投資しているため、20%という大幅な成長を遂げています。中東アフリカと南米も防衛力強化のために軍用ヘリコプターに投資しており、それぞれ15%と3%のシェアを占めています。このような開発により、世界の回転翼航空機市場は2023~2030年の間に2,854機のヘリコプターを調達すると予想されています。

世界の軍用ヘリコプター市場の動向

国境緊張の高まりと新型機の必要性から国防費が急増

- アジア太平洋の軍事費は総額5,690億米ドル中国とインドの国境問題などの地政学的紛争、国内安全保障上の課題、海洋モニタリング、対テロ作戦などは、この地域の国々の固定翼航空機の成長を助長する要因の一部です。中国とインドにおける軍事費の増加が2022年の増加の主因です。2022年におけるこの地域の2カ国の軍事費の合計は66%でした。過去10年間における各国の国防費の増加は、経済成長と領土紛争によってもたらされました。

- アジア太平洋には、インド、中国、日本、韓国をはじめとする主要な軍事大国が存在し、国防予算も年々増加しています。この予算には、航空優位性の向上と拡大のための大きな部分が含まれており、この地域における軍事航空の成長を牽引しています。例えば、インド政府は2023年度予算で、新型戦闘機ラファールへの決済やスホイ-30MKI、テジャス戦闘機の製造を含め、インド空軍のために前回予算より約10%増額した予算を計上しました。

- アジア太平洋における軍事費の増加は、多くの地域主権主体が存在する南シナ海の緊張や、インド・中国、インド・パキスタン間の国境紛争など、いくつかの政治的・国境的紛争において優位に立つことを目的としています。中国の主要国の国防支出は、2030年までに4,000億米ドルを超えると予想されています。

艦隊の近代化と新規調達は、アジア太平洋の軍事活動艦隊を改善すると予測されます。

- 2022年末までに、アジア太平洋の現役航空機数は1万5,543機で、そのうち固定翼機が60%を占め、残りの航空機数は回転翼機です。中国、インド、日本、韓国を合わせると、この地域の現役航空機総数の55%を占めます。

- 2020年時点で、アジア太平洋の平均航空機保有年数は9.5年であったが、2030年には10.7年になると予測されています。1960年代にさかのぼる古い航空機の一部は、インド空軍によって徐々に廃止されています。MiG 21とMiG 27は、インド空軍(IAF)を支えてきました。これらの戦闘機の平均機齢は約45年です。オーストラリアの2機の戦闘機、FA-18とF-35は、それぞれ過去16年間と8年間就役しています。

- 中国、インド、韓国などの国々は、近代戦の要求を満たすために航空機保有数を拡大しています。予測期間中も、次世代航空機の生産と取得が続く可能性があります。アジア太平洋の軍事はまた、外部の脅威に対する軍事的優位性を獲得するために、最先端技術を駆使してヘリコプターの能力を強化しています。

- アジア太平洋の現役航空機保有数は、2022年には2017年比で3%増加しました。東南アジアでは、インドネシアとタイが保有機数の63%を占めています。今後数年間、タイ、マレーシア、シンガポール、インドネシア、フィリピンなどの主要国が135機以上の航空機調達を計画しているため、航空機保有数は増加する可能性があります。同地域の活発な航空機保有数は、予測期間中に健全な速度で拡大すると予想されます。

軍用ヘリコプター産業概要

軍用ヘリコプター市場はかなり統合されており、上位5社で76.84%を占めています。この市場の主要企業は、Airbus SE、Lockheed Martin Corporation、Russian Helicopters、Textron Inc.、The Boeing Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 国内総生産

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

- アクティブフリートデータ

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

- 国防支出

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- 機体タイプ

- マルチミッションヘリコプター

- 輸送用ヘリコプター

- その他

- 地域

- アジア太平洋

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- シンガポール

- 韓国

- タイ

- その他のアジア太平洋

- 欧州

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

- 中東・アフリカ

- アルジェリア

- エジプト

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

- 北米

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 南米

- ブラジル

- チリ

- コロンビア

- その他の南米

- アジア太平洋

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Hindustan Aeronautics Limited

- Leonardo S.p.A

- Lockheed Martin Corporation

- MD Helicopters LLC.

- Russian Helicopters

- Textron Inc.

- The Boeing Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92465

The Military Helicopters Market size is estimated at 9.17 billion USD in 2025, and is expected to reach 10.21 billion USD by 2030, growing at a CAGR of 2.16% during the forecast period (2025-2030).

The multi-mission helicopter segment is expected to generate the highest demand in the overall military helicopters market to counter various emerging threats

- There is an increase in the use of rotorcraft due to increased military conflicts, terrorism, border disputes, territory invasions, and violations. A number of regional armed forces are also upgrading their helicopters with cutting-edge technologies to gain a military advantage over their adversaries. In addition to providing close air support to troops and destroying enemy armor, multi-mission helicopters can be used for anti-tank missions.

- During the historical period, the multi-mission helicopter was the most procured model, accounting for 49% of the total military helicopter fleet, followed by other rotorcrafts (utility helicopters, maritime helicopters, anti-submarine warfare helicopters, and training helicopters) and transport helicopters, which accounted for shares of 37% and 13%, respectively. During the same period, some of the most procured rotorcraft models were the UH-60 series helicopter with 409 procurements, followed by AH-1Z and CH-47D/F with 180 and 173 aircraft procurements, respectively.

- Furthermore, the demand for military helicopters has been fueled by several factors, such as the changing nature of modern warfare, characterized by asymmetric threats and complex operational environments, which has necessitated the need for highly adaptable and flexible platforms. The rise of hybrid warfare conventional and unconventional tactics has also increased the demand for helicopters with advanced ISR capabilities. Factors such as these are expected to drive the demand for military aircraft procurement. During the forecast period, a total of 2,854 rotorcraft are expected to be delivered globally.

Rising Geopolitical Threats Associated With Increasing Defense Budgets Are Driving The Market

- The global military helicopter market has grown significantly over the years, driven by increasing defense budgets, evolving security threats, and advancements in helicopter technology. Military helicopters are crucial in modern warfare, providing rapid transport, close air support, and combat capabilities.

- In 2022, the war between Russia and Ukraine further fueled the defense budgets across various countries and the need to reassess the operational readiness of the armed forces globally. The global military expenditure rose by 3.7% in 2022 to reach a record high of USD 2240 billion. Russia's invasion of Ukraine was a major driver of the growth in spending in 2022. The five biggest spenders in 2022 were the United States, China, Russia, India, and Saudi Arabia, which together accounted for 63% of world military spending

- In terms of military helicopter procurements during 2017-2022, North America dominates the market, with 38% of the total helicopter fleet, primarily driven by the United States. The United States has the largest military helicopter fleet globally, with 32% of the global share. Asia-Pacific is another significant market, with a share of 25%, due to the increasing defense budgets of countries like China and India. Europe has witnessed a substantial growth of 20%, with countries like Russia, France, Germany, and the United Kingdom investing in helicopter modernization programs. The Middle East Africa and South America are also investing in military helicopters to enhance their defense capabilities and have a share of 15% and 3% respectively. Due to such developments, the global rotorcraft aircraft market is expected to procure 2,854 helicopters between 2023 and 2030.

Global Military Helicopters Market Trends

Increased border tensions and the need for new aircraft has led to a surge in defense expenditure

- Asia-Pacific spent a total of USD 569 billion on military expenditures. Geopolitical conflicts such as border issues between China and India, internal security challenges, maritime surveillance, and counter-terrorism operations are some of the factors aiding the growth of the fixed-wing aircraft fleet of the countries in this region. The rise in military spending in China and India was the main cause of the increase in 2022. The combined military spending of the two nations in the region in 2022 was 66%. The increase in defense spending of the nations over the past ten years was driven by economic growth and territorial disputes.

- Major military powers, including India, China, Japan, and South Korea, are present in the Asia-Pacific region and are yearly growing their defense budgets. This budget includes a significant portion for the improvement and expansion of air superiority, which is driving the growth of military aviation in the region. For instance, in the budget of FY 2023, the Indian government allocated about 10% more for the Indian Air Force compared to the previous budget, including payments for the new Rafale fighters and the manufacturing of Sukhoi-30MKIs and Tejas fighters.

- The increased military spending in the Asia-Pacific region is intended to gain an advantage in several political and border conflicts, such as the tension in the South China Sea with many regional sovereign entities and border conflicts between India-China and India-Pakistan. The defense spending of major countries in China is expected to cross over USD 400 billion by 2030.

Fleet modernization and new procurements are projected to improve the APAC's military active fleet

- By the end of 2022, there were 15,543 active aircraft in the Asia-Pacific region, of which fixed-wing aircraft accounted for 60% while rotorcraft accounted for the remaining fleet. China, India, Japan, and South Korea together accounted for 55% of the total active fleet in the region.

- In 2020, the average aircraft fleet age in Asia-Pacific amounted to 9.5 years, which was projected to increase by 2030, when the average aircraft fleet age across the region was expected to be 10.7 years. The older aircraft, some of which date back to the 1960s, have been slowly phased out by the Indian Air Force. The MiG 21 and MiG 27 have been the backbone of the Indian Air Force (IAF). The average age of these aircraft is around 45 years. Australia's two fighter aircraft, FA-18 and F-35, have been in service for the last 16 years and 8 years, respectively.

- Countries such as China, India, and South Korea are expanding their aircraft fleet size to fulfill the demands of modern warfare. They may continue to produce and acquire next-generation aircraft during the forecast period. The regional armed forces are also enhancing the capabilities of helicopters with cutting-edge technology to obtain military superiority over the external threat.

- Asia Pacific's active fleet increased by 3% in 2022 compared to 2017. Indonesia and Thailand accounted for 63% of the total fleet in Southeast Asia. In the coming years, the aircraft fleet may increase as major countries like Thailand, Malaysia, Singapore, Indonesia, and the Philippines plan to procure over 135 aircraft. The active fleet of the region is expected to expand at a healthy rate during the forecast period.

Military Helicopters Industry Overview

The Military Helicopters Market is fairly consolidated, with the top five companies occupying 76.84%. The major players in this market are Airbus SE, Lockheed Martin Corporation, Russian Helicopters, Textron Inc. and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Gross Domestic Product

- 4.1.1 Asia-Pacific

- 4.1.2 Europe

- 4.1.3 Middle East and Africa

- 4.1.4 North America

- 4.1.5 South America

- 4.2 Active Fleet Data

- 4.2.1 Asia-Pacific

- 4.2.2 Europe

- 4.2.3 Middle East and Africa

- 4.2.4 North America

- 4.2.5 South America

- 4.3 Defense Spending

- 4.3.1 Asia-Pacific

- 4.3.2 Europe

- 4.3.3 Middle East and Africa

- 4.3.4 North America

- 4.3.5 South America

- 4.4 Regulatory Framework

- 4.5 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Multi-Mission Helicopter

- 5.1.2 Transport Helicopter

- 5.1.3 Others

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.1.1 Australia

- 5.2.1.2 China

- 5.2.1.3 India

- 5.2.1.4 Indonesia

- 5.2.1.5 Japan

- 5.2.1.6 Malaysia

- 5.2.1.7 Philippines

- 5.2.1.8 Singapore

- 5.2.1.9 South Korea

- 5.2.1.10 Thailand

- 5.2.1.11 Rest of Asia-Pacific

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Germany

- 5.2.2.3 Italy

- 5.2.2.4 Netherlands

- 5.2.2.5 Russia

- 5.2.2.6 Spain

- 5.2.2.7 Turkey

- 5.2.2.8 UK

- 5.2.2.9 Rest of Europe

- 5.2.3 Middle East and Africa

- 5.2.3.1 Algeria

- 5.2.3.2 Egypt

- 5.2.3.3 Qatar

- 5.2.3.4 Saudi Arabia

- 5.2.3.5 United Arab Emirates

- 5.2.3.6 Rest of Middle East and Africa

- 5.2.4 North America

- 5.2.4.1 Canada

- 5.2.4.2 Mexico

- 5.2.4.3 United States

- 5.2.4.4 Rest of North America

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Chile

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Hindustan Aeronautics Limited

- 6.4.3 Leonardo S.p.A

- 6.4.4 Lockheed Martin Corporation

- 6.4.5 MD Helicopters LLC.

- 6.4.6 Russian Helicopters

- 6.4.7 Textron Inc.

- 6.4.8 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms