南米の野菜種子:市場シェア分析、産業動向、成長予測(2025~2030年)

South America Vegetable Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 301 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693546

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

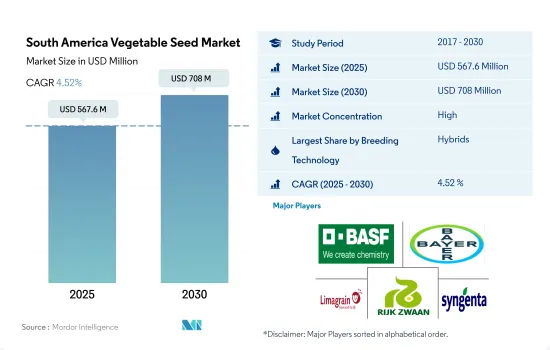

南米の野菜種子市場規模は2025年に5億6,760万米ドルと推定・予測され、2030年には7億800万米ドルに達し、予測期間(2025~2030年)のCAGRは4.52%で成長すると予測されています。

ハイブリッド種子は、保護栽培での使用率が高く、高い収量を安定して生産できることから、南米の種子市場を独占しています。

- 2022年の南米の野菜種子市場では、ハイブリッド種子が開放受粉品種と比較して主要シェアを占め、その金額は3億6,140万米ドルでした。これは、ハイブリッド種子の需要が、干ばつ耐性、土壌への適応性、開放受粉種子品種よりも高い収量などの利点により高いためです。

- ハイブリッド種子のセグメントは、農業従事者による使用量の増加、ハイブリッド種子の新品種を提供する企業、病気や天候、害虫に対する耐性などの利点から、予測期間中にCAGR 9.1%を記録すると予測されます。

- ハイブリッド種子を使用する野菜の栽培面積は、トマト、ニンニク、レタスなどの作物でハイブリッド種子の使用率が高いため、2017年の62万7,300haから2022年には69万5,400haに増加しています。

- 保護栽培では、自然受粉に必要な昆虫や害虫などの制限により、OPVは保護栽培では使用できないため、ハイブリッド種子のシェアは100%となっています。

- シンジェンタ、Rijk Zwaan Zaadteelt en Zaadhandel BV、Enza Zadenなどの大手企業も、ウイルス性病害に耐性があり、ボルト病やベト病に強い改良型ハイブリッド種子品種の提供に力を入れています。

- 開放受粉種子品種は、種子の価格が安いため小規模農業従事者に利用されており、投入コストの節約に役立っているが、害虫が作物を襲うことがあるため作物被害が大きいです。これは予測期間中、開放受粉種子品種の成長を抑制する要因になると予想されます。

- そのため、収穫量の増加や高品質な野菜の生産といった利点から、予測期間中はハイブリッド種子の販売が増加すると予測されます。

栽培面積の多いブラジルが市場を独占

- 2022年、世界の野菜種子市場における南米のシェアは約6.9%であったが、これはチリが種子の主要輸出国であり、天候に恵まれ、国内と世界の野菜の需要が高いためです。

- 野菜の栽培面積が2018年の520万haから2022年には530万haに増加するのは、野菜需要の増加と価格の高騰が高収益につながっているからです。そのため、予測期間中はより多くの種子が栽培に必要になると予想されます。

- ブラジルはこの地域の主要国で、2022年の市場シェアの35.5%を占めています。ブラジルの野菜の栽培面積は2019~2022年にかけて1.2%増加したが、これはさまざまな種類のサラダ、高価値作物、高い投資収益率に向けた野菜の需要があるためです。したがって、同国における野菜種子の販売は予測期間中に増加すると予測されます。

- アルゼンチンは、この地域の第2の主要国です。アルゼンチンにおける野菜の栽培面積は、2017年の19万haから2022年には20万haに増加しました。栽培面積の増加は、政府によるさまざまな取り組みと高価値作物によるものです。したがって、野菜種子の販売は予測期間中に増加すると予測されます。

- その他の南米は、様々な野菜作物、特にトマト、タマネギ、ジャガイモにとって良好な気象条件のため、2023~2030年にかけてCAGR 4.07%を記録すると予測されています。

- したがって、栽培面積の増加、新技術の進歩、野菜に対する高い需要などの要因が、予測期間中に南米の野菜種子市場の成長を促進すると予想されます。

南米の野菜種子市場の動向

唐辛子の価格上昇と消費が牽引し、同地域の野菜の中では唐辛子の栽培面積が最も急速に伸びています。

- 南米は世界有数の野菜生産国です。野菜の栽培面積は2022年に530万ヘクタールに達し、2017~2022年の間に1.7%減少しました。これは、より小さな面積でより高い収量を提供する保護栽培の採用が進んだためです。このため、野菜に必要な地域全体の栽培面積は減少しました。南米では、ブラジルが主要な野菜生産国です。南米の野菜栽培面積の25.3%を占め、2022年には240万ヘクタールとなります。同国の野菜栽培可能地は、保護栽培へのシフトにより、2017~2022年の間に3.1%減少しました。

- 栽培面積では、根菜類と球根類が南米最大のセグメントです。同地域ではジャガイモなどの根菜類が主食であるため、2022年には同地域の野菜総栽培面積の32.4%を占めます。しかし、根菜類と球根類の総栽培面積は、綿花や大豆など他の収益性の高い作物へのシフトにより、2017年の316万haから2022年には311万haに減少しました。ジャガイモは南米で栽培されている主要野菜のひとつです。南米におけるジャガイモの総栽培面積は、2022年には約93万7,100haとなり、ペルーの伝統的栽培地域における気温の上昇と害虫の発生により、2017年から1.8%減少しました。さらに、同国で栽培されている他の主要野菜作物は、タマネギ、キャベツ、エンドウ豆、チリです。2017~2022年の間に、この地域の唐辛子栽培面積は、価格上昇と唐辛子消費により14.6%増加しました。

- そのため、精密農業技術の採用と保護栽培の拡大が、南米の野菜栽培面積の拡大を制限すると推定されます。

耐病性は、タマネギとレタスの栽培で好まれる主要な形質であり、ピンクルート、薹立ちなどの病害と闘う。

- レタスは、この地域で広く消費されている高価値の外来野菜です。高品質な食品、特に輸出向けの需要が高まる中、農業従事者は複数の望ましい形質を持つ高品質の種子を用いてレタスを栽培してきました。病害抵抗性は、チップバーン、ピシウム病、ボルト病に対する抵抗性を含め、この地域で最も好まれている形質です。

- Limagrain、Rijk Zwaan、Enza Zadenのような大手企業は、これらの複数の形質を持つ品種を提供しています。その他の重要な形質には、幅広い適応性、葉数が多い、葉が柔らかい、色づきが良い、貯蔵期間が長い、均一な頭部を生産する、早熟品種などの品質特性があります。農業従事者は、市場の需要を満たし、利益を最大化するため、こうした品種の栽培に関心を寄せています。

- 同様に、タマネギは消費者が調味料や様々な料理に使用する主要な根菜・球根野菜です。この地域の農業従事者は、高収量、ピンクルートやフィトフトラなどの病害に対する抵抗性、長期貯蔵能力、均一な球根の大きさ、球根の色や大きさといった望ましい特性を備えたタマネギの種子を栽培しています。市場の需要を満たし、利益を増やすために、Bayer、Basf、Enza Zaden、Sakata、Rijk Zwaanなどの企業は、生産者が高い収益を達成するのに役立つ種子形質を提供しています。BASF(Nunhems)、Bayer(Seminis)、Limagrain(Vilmorin)などの人気ブランドは、この地域で商業的に販売されているタマネギの種子の幅広いカタログを持っています。

- したがって、耐病性形質、品質特性、貯蔵期間の延長を備えた高品質の野菜に対する需要が、予測期間中の市場を牽引すると予想されます。

南米の野菜種子産業概要

南米の野菜種子市場はかなり統合されており、上位5社で87.27%を占めています。この市場の主要企業は、BASF SE、Bayer AG、Groupe Limagrain、Rijk Zwaan Zaadteelt en Zaadhandel BV、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 野菜

- 最も人気のある品種

- タマネギ、レタス

- トマト、カボチャ、カボチャ

- 育種技術

- 野菜

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- 雑種

- 開放受粉品種とハイブリッド派生品種

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 作物

- アブラナ科

- キャベツ

- ニンジン

- カリフラワー&ブロッコリー

- その他のアブラナ

- ウリ科

- キュウリ・ガーキン

- かぼちゃ・カボチャ

- その他ウリ科

- 根菜・球根

- ニンニク

- タマネギ

- ジャガイモ

- その他の根菜類

- ナス科

- 唐辛子

- ナス科

- トマト

- その他ナス科

- 分類されていない野菜

- アスパラガス

- レタス

- オクラ

- エンドウ豆

- ほうれん草

- その他分類されていない野菜

- アブラナ科

- 生産国

- アルゼンチン

- ブラジル

- その他の南米

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BASF SE

- Bayer AG

- Bejo Zaden BV

- Enza Zaden

- Groupe Limagrain

- KWS SAAT SE & Co. KGaA

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Sakata Seeds Corporation

- Syngenta Group

- Takii and Co.,Ltd.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92613

The South America Vegetable Seed Market size is estimated at 567.6 million USD in 2025, and is expected to reach 708 million USD by 2030, growing at a CAGR of 4.52% during the forecast period (2025-2030).

Hybrids dominate the South American seed market due to their high usage in protected cultivation and their ability to produce high yields consistently

- In 2022, hybrids accounted for the major share compared to open-pollinated varieties, with a value of USD 361.4 million in 2022 in the South American vegetable seed market because the demand for hybrid seeds is high due to benefits such as drought tolerance, adaptability to the soil, and higher yield than open-pollinated seed varieties.

- The hybrids segment is estimated to register a CAGR of 9.1% during the forecast period because of the increase in the usage by farmers, companies providing new hybrid seed varieties, and benefits such as resistance to diseases, weather conditions, and pest attacks.

- The cultivation area of vegetables using hybrid seeds has increased from 627.3 thousand ha in 2017 to 695.4 thousand ha in 2022 because of the high usage of hybrids in crops such as tomatoes, garlic, and lettuce.

- In protected cultivation, the share of hybrid seeds was 100% because OPVs cannot be used in protected cultivation due to limitations such as the required insects or pests to be pollinated naturally; in protected cultivation, there is no natural pollination.

- Major companies, such as Syngenta, Rijk Zwaan Zaadteelt en Zaadhandel BV, and Enza Zaden, are also focused on providing improved hybrid seed varieties that are tolerant to viral diseases and are resistant to boltings and mildews.

- Open-pollinated seed varieties are used by small-scale farmers because of the low prices of seed, helping save input costs, but the crop damage is high as pests can attack the crop. This is expected to be a restraint in the growth of open-pollinated seed varieties during the forecast period.

- Therefore, the sales of hybrid seeds are estimated to increase during the forecast period due to benefits such as higher yield and the production of high-quality vegetables.

Brazil dominated the market with a higher area under cultivation

- In 2022, South America's share in the global vegetable seed market was about 6.9% because Chile is a leading exporter of seeds, has favorable weather conditions, and has a high demand for domestic and global vegetables.

- The cultivation area for vegetables increased from 5.2 million ha in 2018 to 5.3 million ha in 2022 because of the increase in the demand for vegetables and high prices, leading to high profits. Therefore, more seeds are expected to be required for cultivation during the forecast period.

- Brazil is the major country in the region, which accounted for 35.5% of the market share in 2022. The cultivation area of vegetables in Brazil increased by 1.2% from 2019 to 2022 because of the demand for vegetables for different types of salads, high-value crops, and high return on investment. Therefore, sales of vegetable seeds in the country are projected to increase during the forecast period.

- Argentina is the second major country in the region. The cultivation area of vegetables in Argentina increased from 0.19 million ha in 2017 to 0.2 million ha in 2022. The increase in cultivation area was due to different initiatives by the government and high-value crops. Therefore, sales of vegetable seeds are estimated to increase during the forecast period.

- The Rest of South America is expected to register a CAGR of 4.07% from 2023 to 2030 because of favorable weather conditions for different vegetable crops, especially tomatoes, onions, and potatoes.

- Therefore, factors such as an increase in the cultivation area, new technological advancements, and high demand for vegetables are expected to fuel the growth of the South American vegetable seed market during the forecast period.

South America Vegetable Seed Market Trends

Chili is experiencing the fastest growth in cultivation area among vegetables in the region, driven by rising prices and consumption of chili

- South America is one of the largest producers of vegetables in the world. The area cultivated under vegetables reached 5.3 million hectares in 2022, which decreased by 1.7% between 2017 and 2022. This was due to the growing adoption of protected cultivation that offered higher yields in smaller areas. This led to a reduction in the region's overall cultivation area needed for vegetables. In South America, Brazil is the major vegetable producer. It accounted for 25.3% of the South American vegetable cultivated area, with 2.4 million hectares in 2022. The vegetable-cultivable land in the country decreased by 3.1% between 2017 and 2022 due to a shift toward protected cultivation.

- By cultivation area, roots and bulbs were the largest segments in South America. They accounted for 32.4% of the region's total vegetable area in 2022, as potatoes and other roots and bulbs are the staple food in the region. However, the total area under roots and bulbs decreased from 3.16 million ha in 2017 to 3.11 million ha in 2022 due to a shift toward other profitable crops such as cotton and soybean. Potato is one of the major vegetables cultivated in South America. The total area under potato production in South America was around 937.1 thousand ha in 2022, which decreased by 1.8% since 2017 due to increased temperatures and pest incidences in the traditional growing areas in Peru. Furthermore, other major vegetable crops cultivated in the country are onion, cabbage, peas, and chili. Between 2017 and 2022, the region's chili cultivation area increased by 14.6% due to rising prices and chili consumption.

- Therefore, the growing adoption of precision farming techniques and protected cultivation is estimated to limit South America's expansion of vegetable cultivation areas.

Disease resistant is the primary trait preferred in onion and lettuce cultivation to combat diseases such as pink root, bolting, and others.

- Lettuce is a high-value exotic vegetable that is widely consumed across the region. With the growing demand for high-quality foods, especially for exports, farmers have been cultivating lettuce using high-quality seeds that possess multiple desirable traits. Disease resistance is the most popular trait preferred in the region, including resistance to tip burn, pythium, and bolting diseases.

- Major companies like Limagrain, Rijk Zwaan, and Enza Zaden offer cultivars with these multiple traits. Other significant traits include wider adaptability, quality attributes such as a high number of leaves, soft leaves, good coloration, extended shelf life, uniformity in producing consistent heads, and early maturation varieties. Farmers are interested in cultivating such varieties to meet market demands and maximize profits.

- Similarly, onions are the leading root and bulb vegetables consumers use for seasoning and in various cuisines. Farmers in the region are cultivating onion seeds with traits that offer high yields, resistance to diseases like pink root and phytophthora, extended storage capacity, uniform bulb size, and desirable attributes such as bulb color and size. To meet market demand and increase profits, companies such as Bayer, Basf, Enza Zaden, Sakata, and Rijk Zwaan offer seed traits that help growers achieve high returns. Popular brands like BASF (Nunhems), Bayer (Seminis), and Limagrain (Vilmorin) have extensive catalogs of onion seeds that are commercially sold in the region.

- Therefore, the demand for high-quality vegetables with disease-resistant traits, quality attributes, and extended shelf life is anticipated to drive the market during the forecast period.

South America Vegetable Seed Industry Overview

The South America Vegetable Seed Market is fairly consolidated, with the top five companies occupying 87.27%. The major players in this market are BASF SE, Bayer AG, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel BV and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Onion & Lettuce

- 4.2.2 Tomato, Pumpkin & Squash

- 4.3 Breeding Techniques

- 4.3.1 Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Family

- 5.3.1 Brassicas

- 5.3.1.1 Cabbage

- 5.3.1.2 Carrot

- 5.3.1.3 Cauliflower & Broccoli

- 5.3.1.4 Other Brassicas

- 5.3.2 Cucurbits

- 5.3.2.1 Cucumber & Gherkin

- 5.3.2.2 Pumpkin & Squash

- 5.3.2.3 Other Cucurbits

- 5.3.3 Roots & Bulbs

- 5.3.3.1 Garlic

- 5.3.3.2 Onion

- 5.3.3.3 Potato

- 5.3.3.4 Other Roots & Bulbs

- 5.3.4 Solanaceae

- 5.3.4.1 Chilli

- 5.3.4.2 Eggplant

- 5.3.4.3 Tomato

- 5.3.4.4 Other Solanaceae

- 5.3.5 Unclassified Vegetables

- 5.3.5.1 Asparagus

- 5.3.5.2 Lettuce

- 5.3.5.3 Okra

- 5.3.5.4 Peas

- 5.3.5.5 Spinach

- 5.3.5.6 Other Unclassified Vegetables

- 5.3.1 Brassicas

- 5.4 Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Bejo Zaden BV

- 6.4.4 Enza Zaden

- 6.4.5 Groupe Limagrain

- 6.4.6 KWS SAAT SE & Co. KGaA

- 6.4.7 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.8 Sakata Seeds Corporation

- 6.4.9 Syngenta Group

- 6.4.10 Takii and Co.,Ltd.

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

南米の野菜種子:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 301 Pages

- 納期

- 2~3営業日