|

市場調査レポート

商品コード

1940826

アジア太平洋地域の野菜種子:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Asia-Pacific Vegetable Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の野菜種子:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

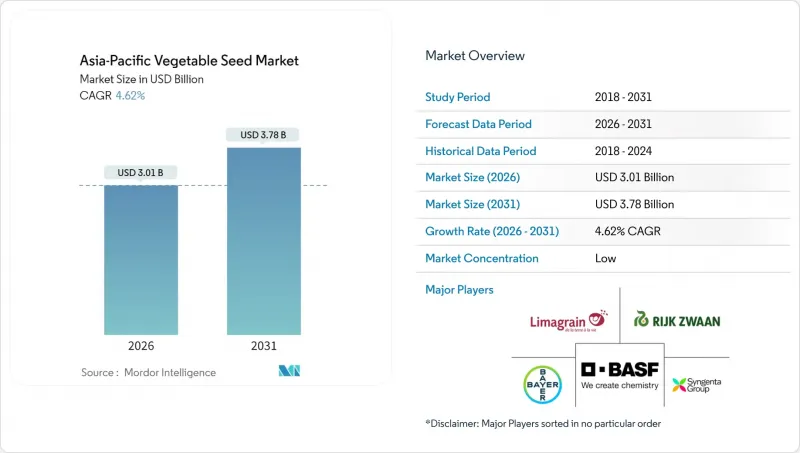

アジア太平洋地域の野菜種子市場は、2025年の28億8,000万米ドルから2026年には30億1,000万米ドルへ成長し、2026年から2031年にかけてCAGR 4.62%で推移し、2031年までに37億8,000万米ドルに達すると予測されています。

堅調な都市部需要、温室インフラの拡大、ハイブリッド技術に対する政府支援が相まって、アジア太平洋地域の野菜種子市場の着実な拡大を支えています。多国籍育種企業はマーカー支援選抜とゲノム予測に注力し新品種の投入サイクルを加速させる一方、地域企業は小規模農家へのコスト効率の高い流通を重視しています。気候変動への耐性に関する調査が研究パイプラインの中心を占めており、ASEAN域内での越境貿易調和に関する議論が、種子の流通効率化に向けた新たな機会を創出しています。こうした動向により、アジア太平洋地域の野菜種子市場は2030年までハイブリッド種子主導の持続的な変革を遂げる見込みです。

アジア太平洋地域の野菜種子市場の動向と洞察

収量・品質向上のためのハイブリッド種子採用の拡大

商業野菜畑におけるハイブリッド種の普及率は2024年に80%を超え、開放受粉系統より25~40%高い収量を実現するとともに、保存期間の延長により収穫後の損失を削減しています。インドやタイの普及機関が資金提供した実証圃場では、生産性の向上が実証され、近隣農家への普及を促進しています。精密育種により開発サイクルが5年に短縮され、抵抗性が失われる前に害虫耐性ハイブリッド種のリリースが可能となっています。種子と農業資材をセットにしたクレジットプログラムは導入障壁をさらに低減し、アジア太平洋地域の野菜種子市場を強化しています。

保護栽培・温室栽培面積の拡大

不安定なモンスーン期における収量安定化を求め、2024年には保護栽培面積が15%増加しました。フィルムコストと自動化コストの低下により、中規模農家における投資回収が改善。中国単独で400万ヘクタール以上がビニールハウスまたはガラスハウス構造で管理されています。種子会社は、植栽密度と日長管理を最適化するコンパクトで耐病性のある品種で対応しています。温室による通年生産は収益源を拡大し、アジア太平洋地域の野菜種子市場を成長させています。

分断化され厳格な種子・遺伝子組み換え規制

新規野菜品種の承認期間はタイで6ヶ月、インドでは3年と地域差が大きく、地域展開戦略を複雑化させています。商業用遺伝子組み換え野菜栽培を許可しているのはオーストラリアとフィリピンのみであり、先進的な遺伝子編集技術の収益化を制約しています。規制対応の重複により研究開発費が最大25%増加し、アジア太平洋地域の野菜種子市場の発展を阻んでいます。

セグメント分析

ハイブリッド品種は2025年時点でアジア太平洋地域の野菜種子市場規模の75.10%を占め、2031年までCAGR4.85%で首位を維持する見込みです。土地不足に直面する商業栽培者にとって、初期種子コストが自然交配品種と比べて3~5倍高いにもかかわらず、25%~40%の収量プレミアムは依然として大きな魅力です。知的財産権の執行は持続的なロイヤルティ収入の基盤となり、多国籍企業にとって農場保存が不可能な独自親系統への投資を明確に促進します。迅速なゲノム予測と二倍体技術により製品サイクルは5~6年に短縮され、企業は新興の害虫圧力に迅速に対応し、アジア太平洋地域の野菜種子市場における競争力を維持することが可能となります。

開放受粉品種は、種子の保存における自律性と低コストを重視する自給農家や有機生産者にとって、今なお有用な選択肢です。公共セクター機関は開発プログラムを通じてこれらの品種を頻繁に配布し、商業流通網が未発達な地域でも基礎的な種子アクセスを確保しています。しかしながら、コールドチェーンの拡大やスーパーマーケットの調達需要が均一性と保存期間の優位性を求める地域では、ハイブリッドの浸透が進んでいます。融資の拡大と栽培資材向け金融商品の普及に伴い、アジア太平洋地域の野菜種子産業は今後10年間で残存する開放受粉作付面積を高性能ハイブリッドへ転換する可能性が高いでしょう。

アジア太平洋地域の野菜種子市場レポートは、育種技術(ハイブリッド、開放受粉品種、ハイブリッド派生品種)、栽培形態(露地栽培、保護栽培)、作物科(ナス科、アブラナ科、ウリ科など)、国別(オーストラリア、バングラデシュ、中国、インド、インドネシア、日本など)に分類されています。市場予測は金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリーおよび主要な調査結果

第4章 主要な業界動向

- 作付面積

- 野菜

- 主流の形質

- キャベツとレタス

- トマトと唐辛子

- 育種技術

- 野菜

- 規制の枠組み

- バリューチェーン及び流通チャネル分析

- 市場促進要因

- 収量と品質向上のためのハイブリッド種子の採用増加

- 保護栽培および温室栽培面積の拡大

- 政府の園芸プログラムと種子補助金

- 栄養価の高い野菜に対する健康志向の需要

- 都市型垂直農法によるマイクロドワーフ種子需要の拡大

- ブロックチェーンを活用した種子トレーサビリティによるプレミアム価格

- 市場抑制要因

- 分断化され厳格な種子・遺伝子組み換え規制

- 偽造及び規格外種子の流通

- 気候変動による受粉媒介者の変動が種子収量に影響を与える

- 遺伝的基盤の狭さによる病害感受性コストの増加

第5章 市場規模と成長予測(金額および数量)

- 育種技術

- 交配種

- 自然交配品種および交配品種

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 作物分類

- アブラナ科

- キャベツ

- ニンジン

- カリフラワーとブロッコリー

- その他のアブラナ科野菜

- ウリ科

- キュウリとガーキン

- カボチャとウリ類

- その他のウリ科野菜

- 根菜類と球根類

- ニンニク

- タマネギ

- ジャガイモ

- その他の根菜類・球根類

- ナス科

- 唐辛子

- ナス

- トマト

- その他のナス科

- 分類されていない野菜

- アスパラガス

- レタス

- オクラ

- エンドウ豆

- ほうれん草

- その他の分類されない野菜

- アブラナ科

- 国

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- 企業概要

- 企業プロファイル

- Bayer AG

- Syngenta Group

- BASF SE

- Advanta Seeds(UPL Limited)

- East-West Seed

- Sakata Seed Corporation

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Groupe Limagrain

- Corteva Agriscience

- Enza Zaden Holding BV

- Bejo Zaden BV

- Takii and Co., Ltd.

- Namdhari Seeds Pvt. Ltd.

- Maharashtra Hybrid Seeds Company Private Limited(Mahyco Private Limited)