|

市場調査レポート

商品コード

1693477

アフリカの野菜種子:市場シェア分析、産業動向、成長予測(2025~2030年)Africa Vegetable Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの野菜種子:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 331 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

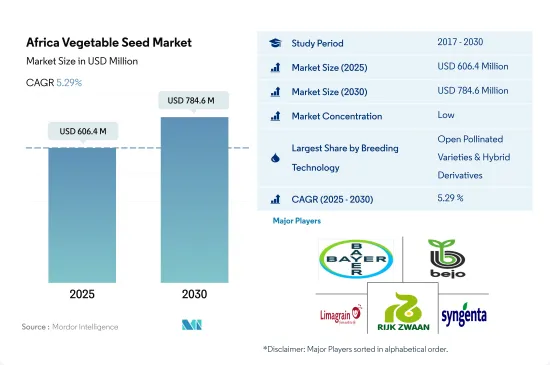

アフリカの野菜種子市場規模は、2025年に6億640万米ドルと推定され、2030年には7億8,460万米ドルに達し、予測期間中(2025~2030年)のCAGRは5.29%で成長すると予測されます。

開放受粉品種が市場を独占し、高収量と耐病性によりハイブリッド種子の利用が増加

- アフリカでは、2022年には開放受粉品種が野菜種子市場全体の55.1%を占め市場を独占し、ハイブリッド野菜種子は44.9%のシェアを占めました。これは主に野菜生産需要の増加によるものです。ハイブリッド種子の高い収量がアフリカの野菜種子市場を牽引しています。

- 2022年には、ハイブリッド種子市場の下で、ナス科のセグメントは54.3%で、地域の野菜種子市場の金額ベースで最も高いシェアを占めました。作物レベルでは、トマトとタマネギが金額ベースで主要な野菜作物であり、2022年のハイブリッド野菜種子市場でそれぞれ約47.8%と5.5%のシェアを占めます。ハイブリッド種子市場は、主に農業の近代化と新製品の開発によって牽引されています。アフリカにおける野菜の有機栽培面積の拡大が、非トランスジェニックハイブリッドの成長に寄与しています。

- アフリカの野菜生産における開放受粉品種とハイブリッド派生品種の総栽培面積は、2017~2022年の間に2%以上増加しました。この増加は主に、農村部や半都市部におけるマイナーな野菜作物でのOPVの使用の増加によるものです。

- 2022年には、分類されていない野菜がこの地域の開放受粉品種とハイブリッド派生野菜種子市場の約30.9%を占めます。この作物には、在来種のアスパラガス、アーティチョーク、その他の野菜が含まれます。

- 栽培面積の増加と野菜需要の増加が、CAGR 5.7%で予測期間中のハイブリッド種子市場を牽引すると予測されます。

ナイジェリアは耕作面積と市販種子の使用量が多く、アフリカの野菜種子市場を独占

- 2022年、アフリカの種子市場における野菜のシェアは低く、金額ベースで20.8%を占めました。アフリカにおける野菜生産の栽培面積は、野菜需要の増加、高い投資収益率、新技術により、2017年の4,100万haから2022年には4,800万haに増加しました。

- ナイジェリアはこの地域の主要な野菜種子市場です。2022年にはアフリカの野菜種子市場の60.4%のシェアを占めています。この大きなシェアは主に、同国における野菜栽培の高い普及率、消費需要の増加、栽培面積の拡大によるものです。例えば、同国の野菜栽培面積は2017年の1,810万ヘクタールから2022年には2,190万ヘクタールに増加しています。

- エジプトはこの地域で2番目の主要市場であり、2022年のシェアは12.3%です。エジプトにおける野菜の栽培面積は、2017年の90万ヘクタールから2022年には100万ヘクタールに増加しました。この増加は主に、市場における高収量品種の入手可能性が高まったことによるものです。野菜種子の販売は予測期間中に増加すると予想されます。

- 南アフリカはこの地域の主要な野菜生産国のひとつです。同国では、オランダや中国など他国からの野菜需要が高いため、野菜の栽培が盛んです。2022年に同国で栽培された主要野菜作物は、チリ(15.7%)、レタス(13.7%)、カボチャとカボチャ(13.6%)でした。その他の主要国は、タンザニア、エチオピア、ガーナです。

- したがって、野菜耕作面積の増加による野菜需要の増加に伴い、野菜種子市場は予測期間中に5.7%のCAGRで推移すると予想されます。

アフリカの野菜種子市場動向

根菜類と球根類が野菜栽培面積の主要セグメントであり、主にタマネギとジャガイモの大規模栽培に牽引される

- 2022年、アフリカの野菜栽培面積は、アフリカの総栽培面積の18.6%を占めました。これは、野菜は連作作物よりも栽培に多くの水を必要とするため、この地域の農業従事者が連作作物の栽培を好むためです。さらに、アフリカでは頻繁に干ばつが発生するため、野菜の栽培も制限されています。

- 2022年のアフリカの野菜作付面積の84.9%は根菜類と球根類でした。これは、この地域の多様な農業気候帯が、特にジャガイモ、サツマイモ、キャッサバ、ヤムイモ、タロイモなどの作物にとって、根菜・球根栽培に好条件を提供しているためです。さらに、根菜・球根市場の安定性とその安定した需要は、多くのアフリカ農業従事者にとって魅力的な選択肢となっています。その結果、このセグメントの作付面積は2030年には4,650万haに達すると推定されます。分類されていない野菜はアフリカで2番目に大きな栽培面積を占め、2022年には地域全体の栽培面積の7.5%を占めます。これは、この地域でオクラとエンドウ豆の消費が多いためです。さらに、オクラとエンドウ豆はアフリカの気候に適しており、栽培も比較的容易です。

- 2022年には、ナイジェリアが42.7%(2,190万ha)のシェアを占め、アフリカにおける野菜栽培の主要な土地となりました。これは、同国がアフリカ最大の地理的面積を有し、野菜栽培に非常に適した肥沃な土壌を有しているためです。

- したがって、多様な農業気候帯、野菜栽培に適した条件、安定した野菜需要が、予測期間中にアフリカでの栽培面積を拡大すると推定されます。

耐病性は、キャベツやエンドウの栽培において非常に好まれる形質です。なぜなら、耐病性は、キャベツの黒腐病やエンドウの花畑病などの流行病害と闘うことができるからです。

- キャベツはアフリカで最も広く栽培されている外来葉野菜のひとつです。新鮮サラダ、スープ、ソテー、典型的な夏野菜に対するレストランからの需要が、キャベツの需要を牽引しています。農業従事者は、高品質の食品に対する需要の高まりから、複数の望ましい形質を持つ高品質の種子を用いてキャベツを栽培しています。

- 頭の大きさ、葉の色の均一性、様々な栽培条件への適応性、早熟性、耐病性などの特徴を持つ種子品種は、この地域の生産者による嗜好性が高いため、市場の成長を後押ししています。キャベツでは、Xanthomonas campestris PV.カンペストリス(XCC)は10~50%の収量損失をもたらします。BayerAG、BASF SE、サカタのタネ、シンジェンタ・グループといった市場の主要企業は、黒腐病、べと病、その他の葉の病害を含む病害に抵抗性があり、生産性が高い品種を提供しています。これらの種子品種は、作物の損失を防ぐために高い需要があります。

- エンドウ豆はアフリカ地域の多くの地域で重要な作物です。農業従事者は、真菌、ウイルス、線虫の感染に抵抗するエンドウ豆の種子を栽培しています。これらの種子は、さまざまな栽培条件、特にストレスの多い条件への適応性が高いことでも知られています。サヤ1粒あたりの豆の量が多く、サヤの形や大きさも好ましいです。

- したがって、高収量とともに、耐病性、幅広い適応性などの形質を持つ新しい種子品種の導入が、予測期間中の種子市場の成長を後押しすると予測されます。

アフリカの野菜種子産業概要

アフリカの野菜種子市場はセグメント化されており、上位5社で26.38%を占めています。この市場の主要企業は、Bayer AG、Bejo Zaden BV、Groupe Limagrain、Rijk Zwaan Zaadteelt en Zaadhandel B.V.、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 野菜

- 最も人気のある品種

- キャベツとエンドウ豆

- トマトと唐辛子

- 育種技術

- 野菜

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- 雑種

- 開放受粉品種とハイブリッド派生品種

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 作物ファミリー

- アブラナ科

- キャベツ

- ニンジン

- カリフラワー&ブロッコリー

- その他のアブラナ

- ウリ科

- キュウリ・ガーキン

- かぼちゃ・カボチャ

- その他ウリ科

- 根菜・球根

- ニンニク

- タマネギ

- ジャガイモ

- その他の根菜類

- ナス科

- 唐辛子

- ナス科

- トマト

- その他ナス科

- 分類されていない野菜

- アスパラガス

- レタス

- オクラ

- エンドウ豆

- ほうれん草

- その他分類されていない野菜

- アブラナ科

- 生産国

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BASF SE

- Bayer AG

- Bejo Zaden BV

- Enza Zaden

- Groupe Limagrain

- Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- Sakata Seeds Corporation

- Syngenta Group

- Takii and Co.,Ltd.

- Zambia Seed Company Limited(Zamseed)

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92540

The Africa Vegetable Seed Market size is estimated at 606.4 million USD in 2025, and is expected to reach 784.6 million USD by 2030, growing at a CAGR of 5.29% during the forecast period (2025-2030).

Open-pollinated varieties dominate the market, and hybrid seed usage is increasing due to high yield and disease-resistant characteristics

- In Africa, open-pollinated varieties dominated the market in 2022, with a share of 55.1% of the total vegetable seed market, and hybrid vegetable seeds occupied a share of 44.9%. This is mainly due to an increase in the demand for vegetable production. The higher yield of hybrid seeds is driving the African vegetable seed market.

- In 2022, under the hybrid seeds market, the Solanaceae segment accounted for the highest share in terms of value, with 54.3%, of the regional vegetable seed market. At the crop level, tomatoes and onions are the major vegetable crops in terms of value, accounting for shares of around 47.8% and 5.5%, respectively, of the hybrid vegetable seed market in 2022. The market for hybrid seeds is primarily driven by the modernization of agriculture and the development of new products. The expansion of the organic farming area for vegetables in Africa is contributing to the growth of non-transgenic hybrids.

- The total area under open-pollinated varieties and hybrid derivatives in African vegetable production increased between 2017 and 2022 by more than 2%. The increase was mainly because of the rise in the usage of OPVs in minor vegetable crops in rural and semi-urban areas.

- In 2022, unclassified vegetables accounted for about 30.9% of the region's open-pollinated varieties and hybrid derivatives vegetable seed market. The crops included native types of asparagus, artichokes, and other vegetables.

- The increase in area under cultivation and an increase in the demand for vegetables are estimated to drive the hybrid seed market during the forecast period with a CAGR of 5.7%.

Nigeria dominates the African vegetable seed market with higher area under cultivation and usage of commercial seeds

- In 2022, vegetables held a lower share of the African seed market, accounting for 20.8% in terms of value. The cultivation area under vegetable production in Africa increased from 41 million ha in 2017 to 48 million ha in 2022, owing to the increase in the demand for vegetables, high return on investment, and new technologies.

- Nigeria is the major vegetable seed market in the region. In 2022, it accounted for a 60.4% share of the African vegetable seed market. This large share is mainly due to the high adoption of vegetable cultivation in the country, the increasing consumption demand, and the growing area under cultivation. For instance, the vegetable cultivation area in the country increased from 18.1 million hectares in 2017 to 21.9 million hectares in 2022.

- Egypt is the second major market in the region, with a share of 12.3% in 2022. The cultivation area of vegetables in Egypt increased from 0.9 million hectares in 2017 to 1.0 million hectares in 2022. The increase was mainly due to the increased availability of high-yielding cultivars in the market. The sales of vegetable seeds are expected to increase during the forecast period.

- South Africa is one of the major vegetable-producing countries in the region. The country grows vegetables to a large extent due to the high demand for vegetables from other countries, such as the Netherlands and China. In 2022, the major vegetable crops grown in the country were chili (15.7%), lettuce (13.7%), and pumpkin and squash (13.6%). The other major countries in the region are Tanzania, Ethiopia, and Ghana.

- Therefore, with the increase in demand for vegetables due to the increasing area under vegetable farming, the vegetable seed market is anticipated to record a CAGR of 5.7% during the forecast period.

Africa Vegetable Seed Market Trends

Roots and bulbs are the leading segment in the vegetable cultivation area, primarily driven by the extensive cultivation of onion and potatoes

- In 2022, the area cultivated for vegetables in Africa accounted for 18.6% of the total area under cultivation in Africa. This is because farmers in the region prefer to cultivate row crops as the vegetables require more water for cultivation than for row crops. Additionally, frequent drought conditions in Africa also restrain vegetable cultivation.

- Roots & bulbs accounted for 84.9% of the African vegetable acreage in 2022. This was because the region's diverse agro-climatic zones provide favorable conditions for root & bulb cultivation, particularly for crops such as potatoes, sweet potatoes, cassava, yam, and taro. Additionally, the stability of the roots & bulbs market, combined with its consistent demand, makes it an attractive option for many African farmers. As a result, the acreage for this segment is estimated to reach 46.5 million ha in 2030. Unclassified vegetables accounted for the second largest acreage in Africa, with a share of 7.5% of the overall region's cultivation area in 2022. This is because of the region's high consumption of okra and peas. Additionally, okra and peas are well-suited to African climates and are relatively easy to grow.

- In 2022, Nigeria accounted for the major land for vegetable cultivation in Africa, with a share of 42.7% (21.9 million ha). This is because the country has the largest geographical area in Africa and has fertile soils, which are highly suitable for vegetable cultivation.

- Therefore, the diverse agro-climatic zones, favorable conditions for vegetable cultivation, and consistent demand for vegetables are estimated to expand the cultivation area in Africa during the forecast period.

Disease resistance is a highly preferred trait in cabbage and peas cultivation because it can combat prevalent diseases such as black rot in cabbages and floral diseases in peas

- Cabbage is one of Africa's most widely cultivated exotic leafy vegetables. The demand from restaurants for fresh salads, soups, sautees, and typical summer vegetables drives the demand for cabbage. Farmers cultivate cabbage using high-quality seeds with multiple desirable traits due to the growing demand for high-quality foods.

- Seed varieties with traits such as uniformity in head size, foliage color, adaptability to different growing conditions, early maturity, and disease tolerance are boosting the market's growth due to higher preference by the growers in the region. In cabbage, black rot is the major disease in the region caused by Xanthomonas campestris PV. Campestris (XCC) results in 10-50% yield losses. Major players in the market, such as Bayer AG, BASF SE, Sakata Seeds Corporation, and Syngenta Group, offer cultivars that resist diseases, including black rot, mildews, and other leaf diseases, along with higher productivity. These seed varieties are witnessing high demand to prevent crop losses.

- Peas are an important crop in many parts of the African region. Farmers cultivate pea seeds that resist fungal, viral, and nematode infections. These seeds are also known for their wider adaptability to different growing conditions, especially stressful conditions. They possess high peas per pod and desirable pod shape and size.

- Therefore, introducing new seed varieties with traits such as disease resistance, wider adaptability, etc., along with high yield, is projected to boost the growth of the seed market during the forecast period.

Africa Vegetable Seed Industry Overview

The Africa Vegetable Seed Market is fragmented, with the top five companies occupying 26.38%. The major players in this market are Bayer AG, Bejo Zaden BV, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel B.V. and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Cabbage & Peas

- 4.2.2 Tomato & Chilli

- 4.3 Breeding Techniques

- 4.3.1 Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Family

- 5.3.1 Brassicas

- 5.3.1.1 Cabbage

- 5.3.1.2 Carrot

- 5.3.1.3 Cauliflower & Broccoli

- 5.3.1.4 Other Brassicas

- 5.3.2 Cucurbits

- 5.3.2.1 Cucumber & Gherkin

- 5.3.2.2 Pumpkin & Squash

- 5.3.2.3 Other Cucurbits

- 5.3.3 Roots & Bulbs

- 5.3.3.1 Garlic

- 5.3.3.2 Onion

- 5.3.3.3 Potato

- 5.3.3.4 Other Roots & Bulbs

- 5.3.4 Solanaceae

- 5.3.4.1 Chilli

- 5.3.4.2 Eggplant

- 5.3.4.3 Tomato

- 5.3.4.4 Other Solanaceae

- 5.3.5 Unclassified Vegetables

- 5.3.5.1 Asparagus

- 5.3.5.2 Lettuce

- 5.3.5.3 Okra

- 5.3.5.4 Peas

- 5.3.5.5 Spinach

- 5.3.5.6 Other Unclassified Vegetables

- 5.3.1 Brassicas

- 5.4 Country

- 5.4.1 Egypt

- 5.4.2 Ethiopia

- 5.4.3 Ghana

- 5.4.4 Kenya

- 5.4.5 Nigeria

- 5.4.6 South Africa

- 5.4.7 Tanzania

- 5.4.8 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Bejo Zaden BV

- 6.4.4 Enza Zaden

- 6.4.5 Groupe Limagrain

- 6.4.6 Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- 6.4.7 Sakata Seeds Corporation

- 6.4.8 Syngenta Group

- 6.4.9 Takii and Co.,Ltd.

- 6.4.10 Zambia Seed Company Limited (Zamseed)

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms