|

市場調査レポート

商品コード

1693463

欧州の野菜種子:市場シェア分析、産業動向、成長予測(2025~2030年)Europe Vegetable Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の野菜種子:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 369 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

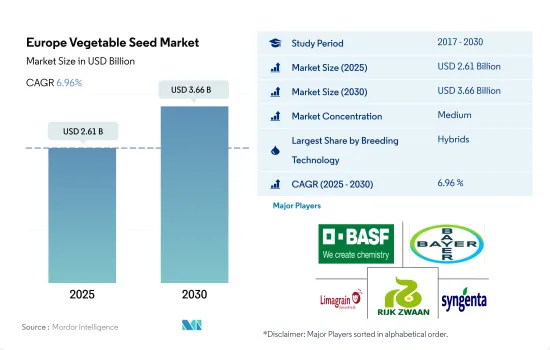

欧州の野菜種子市場規模は2025年に26億1,000万米ドルと推定・予測され、2030年には36億6,000万米ドルに達し、予測期間(2025~2030年)のCAGRは6.96%で成長すると予測されています。

ハイブリッド種子がこの地域の野菜種子市場を独占、保護栽培や有機栽培の需要が増加

- ハイブリッド種子セグメントが欧州の野菜種子市場を独占しています。ハイブリッド種子はエンドウ、トマト、タマネギ、ニンジンで主に開発されており、2022年の欧州ハイブリッド野菜種子市場の37.2%、7.6%、6.9%、6.8%をそれぞれ占めました。これらはこの地域で最も取引され消費されている野菜です。

- 2022年には、この地域のハイブリッド野菜種子市場において、分類されていない野菜と根菜・球根のセグメントがそれぞれ55%と13.1%の主要シェアを占めています。ハイブリッド野菜種子は保存性が向上し、収量が多いため、野菜生産者の間で好まれています。

- 開放受粉品種はエンドウ、カボチャとカボチャ、レタスで主に開発されており、2022年のOPV野菜種子市場の45.9%を占めています。ロシア、イタリア、ドイツは、開放受粉品種(OPV)を使用する主要野菜生産国で、2022年の欧州OPV野菜種子市場の37.5%を占めました。

- 欧州の有機栽培面積は2016~2021年の間に26%増加しました。2021年の有機栽培面積は1,709万haです。したがって、非トランスジェニックハイブリッド種子とOPVは、予測期間中に莫大な需要が発生すると予測されます。

- Bayerは、新セグメントの野菜種子の提供を拡大し、有機生産種子を含めることを意図しています。この発売は、温室とガラス温室市場向けの3つの主要作物、すなわちトマト、ピーマン、キュウリの有機認証生産に集中します。

- したがって、生鮮食品市場からの野菜需要の増加と市販品種の高収量が、同地域におけるハイブリッド種子の普及を加速させ、予測期間中のCAGRは7%になると予測されます。

ロシアは栽培面積が多く、市販種子の使用率が高いため、同地域の野菜種子市場を独占しています。

- 欧州では野菜の需要が急速に伸びています。2022年には金額ベースで世界の野菜種子市場の19.3%に寄与しました。この地域はアブラナ科植物の重要な生産地であり、2022年の世界のアブラナ科植物種子市場で26.4%のシェアを占めています。

- ロシアは欧州の主要市場です。2022年、ロシアでは野菜種子セグメントが種子市場の28.2%を占めます。同国で栽培されている主要野菜はナス科の野菜です。トマトはロシア市場の主要野菜で、2022年には3,220万米ドルを占めます。トルコ産トマトの輸入が禁止されたことで、ロシアではトマトの栽培が増え、トマトの自給自足が可能になりました。

- スペインは2022年に12.3%のシェアを占め、同地域で第2位となりました。野菜部門はスペイン経済において重要な役割を担っており、国内市場だけでなくその他の欧州諸国からの野菜需要も満たしています。同国の野菜栽培面積は、2022年には総栽培面積の約5.0%を占めます。

- 2022年には、フランスはこの地域の野菜種子市場の9.0%を占めます。分類されていない野菜はフランスの主要作物セグメントであり、2022年にはフランスの野菜種子市場の60.8%を占めます。これは同国で葉物野菜の需要が伸びているためです。この地域の他の主要国には、ウクライナ、ドイツ、イタリアなどがあります。

- 欧州では、野菜の栽培面積は2017~2022年の間に870万haから830万haに減少しました。しかし、消費用野菜の需要は増加しており、品種改良による生産性の向上で対応できます。したがって、予測期間中、この地域では改良種子の需要が増加すると予想されます。

欧州の野菜種子市場動向

高収入が期待でき、国内需要が旺盛なため、欧州では根菜類と球根類が野菜栽培の大半を占める

- 欧州では2022年に900万ヘクタール近くの土地が野菜栽培に充てられ、同地域の総栽培面積の5.4%を占めました。欧州で最大の野菜栽培地域はフランス、ロシア、ウクライナ、トルコにあり、これらを合計すると2022年の同地域の野菜栽培面積の60.5%を占めます。

- 根菜類と球根のセグメントは、欧州における栽培面積で最大のセグメントであり、2022年の野菜作物栽培面積全体の46%を占めています。根菜・球根作物のうち、タマネギの栽培面積が増加したのは、フランス、ベルギー、ドイツ、オランダでの需要が高かったためです。タマネギの栽培面積が年々拡大しているのは、タマネギの価格が高止まりしていると推定されるため、複数の生産者がタマネギの栽培開始を選択したためです。この動向がタマネギ種子市場を牽引すると推定されます。タマネギの栽培面積は、2020年の42万haから2022年には43万3,100haに増加します。ジャガイモはこの地域の主要作物であり、2022年には野菜栽培面積の39.8%を占めます。欧州におけるジャガイモの栽培面積は減少しています。例えば2022年には、ポーランドやルーマニアといった主要生産国からの急激な減少により、面積は2017年の490万haから9%減少します。

- 欧州のトマト栽培面積は、生鮮農産物の価格上昇と消費拡大と加工産業からの需要により、2021年の58万5,200haから2022年には59万2,400haに増加しました。例えば、欧州におけるトマトの消費量は2017年の6,500トンから2022年には7,159トンに増加し、加工用トマトは2022年に1万1,000トンを占め、前年比7%増加しました。したがって、これらの要因が種子市場の成長を促進すると推定されます。

病気に強く、均一性の高いニンジンとカリフラワーの形質を持つハイブリッドの使用が増加しています。

- ニンジンやカリフラワー・ブロッコリーの生産は、気候変動、病気、害虫の攻撃によりますます困難になっています。そのため、耐病性、耐アビオティックストレス性、均一性、高収量性などの形質を持つ種子の需要が市場の成長を促進しています。

- ニンジンとカリフラワーの生育は、低窒素含量、暑さ、洪水、干ばつ、塩分などの生物学的ストレスに大きく影響されます。これらの悪環境は、これらの作物の収量を著しく低下させています。そのため、この地域では生物的ストレスに対する耐性を持つ種子品種に対する需要が高まっている

- 近年では、うどんこ病、アルテルナリア斑点病、ボルト病に対する耐病性形質を持つハイブリッド種子の採用により、収量が大幅に増加しています。例えば、カリフラワーとブロッコリーの収量は、2019年の16万7,168 hg/haから2021年には16万7,803 hg/haに急増しました。同様に、ニンジンの収量は同期間に36万7,359 hg/haから386,331 hg/haに上昇しました。

- 望ましい内外色、長いニンジンの根、カリフラワーのクラウンとカードにおける高い均一性といった品質形質は、消費者への美的アピールのために広く評価されています。こうした要因から、この地域の主要企業は、各国の特定の気候条件に適した多様なポートフォリオを開発してきました。例えば英国では、Rijk ZwaanがDexter RZ F1、Lavender RZ F1、Stabilis RZ F1といったカリフラワー品種を提供しており、いずれも高い均一性を示しています。

- さらに、この地域の農業従事者は、貯蔵期間の延長、長期保存能力、ひび割れ耐性、早生~中生品種、高乾物量などの付加的な形質を持つ作物を栽培しています。

欧州の野菜種子産業概要

欧州の野菜種子市場は適度に統合されており、上位5社で40.80%を占めています。この市場の主要企業は、BASF SE、Bayer AG、Groupe Limagrain、Rijk Zwaan Zaadteelt en Zaadhandel BV、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 野菜

- 最も人気のある形質

- ニンジン、カリフラワー、ブロッコリー

- トマト、キャベツ

- 育種技術

- 野菜

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- 雑種

- 開放受粉品種とハイブリッド派生品種

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 作物ファミリー

- アブラナ科

- キャベツ

- ニンジン

- カリフラワー&ブロッコリー

- その他のアブラナ

- ウリ科

- キュウリ・ガーキン

- かぼちゃ・カボチャ

- その他ウリ科

- 根菜・球根

- ニンニク

- タマネギ

- ジャガイモ

- その他の根菜類

- ナス科

- 唐辛子

- ナス科

- トマト

- その他ナス科

- 分類されていない野菜

- アスパラガス

- レタス

- オクラ

- エンドウ豆

- ほうれん草

- その他分類されていない野菜

- アブラナ科

- 生産国

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BASF SE

- Bayer AG

- Bejo Zaden BV

- Enza Zaden

- Groupe Limagrain

- KWS SAAT SE & Co. KGaA

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Sakata Seeds Corporation

- Syngenta Group

- Takii and Co. Ltd

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92526

The Europe Vegetable Seed Market size is estimated at 2.61 billion USD in 2025, and is expected to reach 3.66 billion USD by 2030, growing at a CAGR of 6.96% during the forecast period (2025-2030).

Hybrids dominate the vegetable seed market in the region with increasing demand for protected and organic cultivation methods

- The hybrid seed segment dominated the European vegetable seed market. Hybrids are largely developed in peas, tomatoes, onions, and carrots, which occupied 37.2%, 7.6%, 6.9%, and 6.8% of the European hybrid vegetable seed market, respectively, in 2022. These are the most traded and consumed vegetables in the region.

- In 2022, unclassified vegetables and roots & bulbs segments held a major share of 55% and 13.1%, respectively, in the region's hybrid vegetable seed market. Hybrid vegetable seeds have improved shelf-life traits and higher yields, boosting their preference among vegetable growers.

- The open-pollinated varieties are largely developed in peas, pumpkin & squash, and lettuce, which together accounted for 45.9% of the OPV vegetable seed market in 2022. Russia, Italy, and Germany were the major vegetable-producing countries using open-pollinated varieties (OPVs), which accounted for 37.5% of the European OPV vegetable seed market in 2022.

- The organic farming area in Europe increased by 26% between 2016 and 2021. The organic area under farming was 17.09 million ha in 2021. Therefore, non-transgenic hybrid seeds and OPVs are estimated to experience huge demand during the forecast period.

- Bayer intended to expand its vegetable seed offerings under the new segment to include organically produced seeds. The launch will concentrate on certified organic production of three major crops for the greenhouse and glasshouse market, namely, tomato, sweet pepper, and cucumber.

- Therefore, the increase in demand for vegetables from the fresh food market and higher yield with commercial varieties are estimated to drive the hybrids faster in the region, with a CAGR of 7% during the forecast period.

Russia dominated the region's vegetable seed market due to higher area under cultivation and higher usage of commercial seeds

- In Europe, the demand for vegetables is growing rapidly. It contributed 19.3% to the global vegetable seed market in terms of value in 2022. The region is a significant producer of brassicas, holding a share of 26.4% in the global brassicas seed market in 2022.

- Russia is the major market in the Europen region. In 2022, the vegetable seed segment accounted for 28.2% of the seed market in Russia. The major vegetables grown in the country are Solanaceae vegetables. Tomato is a major vegetable in the Russian market, accounting for USD 32.2 million in 2022. The ban on Turkish tomato imports made Russia self-sufficient in tomato production by cultivating more tomatoes in the country.

- Spain held second in the region by accounting for a 12.3% share in 2022. The vegetable sector plays a crucial role in Spain's economy, and it fulfills vegetable demand not only from the domestic market but also from the rest of Europe. The vegetable cultivation area in the country accounted for about 5.0% of the total acreage in 2022.

- In 2022, France accounted for 9.0% of the region's vegetable seed market. Unclassified vegetables are France's major crop segment, accounting for 60.8% of the French vegetable seed market in 2022. This is because the demand for leafy vegetables is growing in the country. Other major countries in the region include Ukraine, Germany, and Italy.

- In Europe, the area under cultivation for vegetables decreased from 8.7 million ha to 8.3 million ha between 2017 and 2022. However, there is an increasing demand for vegetables for consumption, which can be catered to by increased productivity through improved varieties. Therefore, the demand for improved seeds is anticipated to increase in the region during the forecast period.

Europe Vegetable Seed Market Trends

Roots and bulbs dominate the vegetable cultivation in Europe due to their high-income potential and strong domestic demand

- Europe had nearly 9 million hectares of land dedicated to vegetable cultivation in 2022, accounting for 5.4% of the region's total cultivation area. The largest vegetable-growing areas in Europe are located in France, Russia, Ukraine, and Turkey, which collectively accounted for 60.5% of the region's vegetable area cultivated in 2022.

- The roots and bulbs segment was the largest segment in terms of acreage in Europe, accounting for 46% of the total area under vegetable crops in 2022. Among roots and bulb crops, the area under onion increased because of high demand in France, Belgium, Germany, and the Netherlands. The acreage of onions is expanding yearly due to several producers choosing to start growing onions because onion prices are estimated to remain high. This trend is estimated to drive the onion seed market. The area under cultivation of onion increased from 420 thousand ha in 2020 to 433.1 thousand ha in 2022. Potato is a major crop in the region, accounting for 39.8% of the vegetable area in 2022. The acreage of potatoes in Europe has been declining. For instance, in 2022, the area decreased by 9% from 4.9 million ha in 2017 due to a sharp decline from the major producing countries such as Poland and Romania.

- The area under tomato cultivation in Europe increased from 585.2 thousand ha in 2021 to 592.4 thousand ha in 2022 due to the increase in the price of fresh produce coupled with growing consumption and demand from the processing industry. For instance, the consumption of tomatoes in Europe increased from 6,500 metric tons in 2017 to 7,159 metric tons in 2022, and tomatoes for processing accounted for 11,000 metric tons in 2022, which increased by 7% from the previous year. Therefore, these factors are estimated to drive the growth of the seed market.

There has been an increase in the use of hybrids with disease-resistant and high uniformity carrot and cauliflower traits

- The production of carrots and cauliflower & broccoli is becoming increasingly challenging due to climate change, diseases, and pest attacks. Therefore, the demand for seeds with traits such as disease resistance, abiotic stress tolerance, uniformity, and higher yield potential is driving the growth of the market.

- The growth of carrot and cauliflower plants is greatly influenced by abiotic stresses such as low nitrogen content, heat, flooding, drought, and salinity. These adverse conditions significantly decrease the yield of these crops. Consequently, there is a higher demand for seed varieties that possess tolerance to abiotic stresses in the region.

- In recent years, the adoption of hybrid seeds containing disease-resistant traits against powdery mildew, Alternaria spots, and bolting has significantly boosted yield. For instance, the yield of cauliflower and broccoli surged to 167,803 hg/ha in 2021 from 167,168 hg/ha in 2019. Similarly, carrot yield rose to 386,331 hg/ha from 367,359 during the same period.

- Quality traits such as desirable internal and external colors, long carrot roots, and high uniformity in cauliflower crowns and curds are widely valued for their aesthetic appeal to consumers. Because of these factors, key players in the region have developed a diverse portfolio suitable for specific climatic conditions of the countries. For instance, in the United Kingdom, Rijk Zwaan offers cauliflower varieties like Dexter RZ F1, Lavender RZ F1, and Stabilis RZ F1, all of which exhibit high uniformity characteristics.

- Furthermore, farmers are cultivating crops with additional traits such as extended shelf life, prolonged storage capabilities, tolerance to cracking, early to medium maturing varieties, and high dry matter content in the region.

Europe Vegetable Seed Industry Overview

The Europe Vegetable Seed Market is moderately consolidated, with the top five companies occupying 40.80%. The major players in this market are BASF SE, Bayer AG, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel BV and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Carrot, Cauliflower and Broccoli

- 4.2.2 Tomato & Cabbage

- 4.3 Breeding Techniques

- 4.3.1 Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Family

- 5.3.1 Brassicas

- 5.3.1.1 Cabbage

- 5.3.1.2 Carrot

- 5.3.1.3 Cauliflower & Broccoli

- 5.3.1.4 Other Brassicas

- 5.3.2 Cucurbits

- 5.3.2.1 Cucumber & Gherkin

- 5.3.2.2 Pumpkin & Squash

- 5.3.2.3 Other Cucurbits

- 5.3.3 Roots & Bulbs

- 5.3.3.1 Garlic

- 5.3.3.2 Onion

- 5.3.3.3 Potato

- 5.3.3.4 Other Roots & Bulbs

- 5.3.4 Solanaceae

- 5.3.4.1 Chilli

- 5.3.4.2 Eggplant

- 5.3.4.3 Tomato

- 5.3.4.4 Other Solanaceae

- 5.3.5 Unclassified Vegetables

- 5.3.5.1 Asparagus

- 5.3.5.2 Lettuce

- 5.3.5.3 Okra

- 5.3.5.4 Peas

- 5.3.5.5 Spinach

- 5.3.5.6 Other Unclassified Vegetables

- 5.3.1 Brassicas

- 5.4 Country

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Netherlands

- 5.4.5 Poland

- 5.4.6 Romania

- 5.4.7 Russia

- 5.4.8 Spain

- 5.4.9 Turkey

- 5.4.10 Ukraine

- 5.4.11 United Kingdom

- 5.4.12 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Bejo Zaden BV

- 6.4.4 Enza Zaden

- 6.4.5 Groupe Limagrain

- 6.4.6 KWS SAAT SE & Co. KGaA

- 6.4.7 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.8 Sakata Seeds Corporation

- 6.4.9 Syngenta Group

- 6.4.10 Takii and Co. Ltd

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms