|

市場調査レポート

商品コード

1693399

日本のシーラント:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Japan Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のシーラント:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 156 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

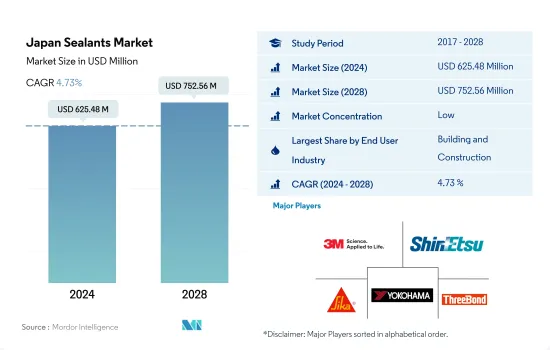

日本のシーラント市場規模は、2024年に6億2,548万米ドルと推定・予測され、2028年には7億5,256万米ドルに達し、予測期間(2024~2028年)のCAGRは4.73%で成長すると予測されます。

自動車市場と建築・建設産業の台頭が日本のシーラント消費を押し上げる見込み

- 日本のシーラント市場では、防水、耐候性シーリング、ひび割れシーリング、目地シーリングなど、建築・建設活動におけるシーラントの多様な用途により、建設産業が主要シェアを占め、その他のエンドユーザー産業がそれに続きます。さらに、建築用シーラントは、耐用年数が長く、さまざまな基材に簡単に塗布できるように設計されています。日本の建設部門は2019年に国内総生産(GDP)の約5.3%を達成し、今後数年間でかなりの成長を記録する可能性が高いです。日本政府は建築物の品質を重視し、サステイナブル開発を推進しているため、予測期間中にシーラント需要が急増する可能性が高いです。

- 様々なシーラントが電気機器製造においてポッティングや保護用途に使用されています。これらはセンサやケーブルのシールに使用されます。日本のエレクトロニクス市場は、2021年に6%近い売上シェアを記録し、高所得層と中間所得層における民生用電子機器製品の急速な普及により、今後数年間は有望な成長を遂げる可能性が高いです。このことは、他のエンドユーザーセグメントにおけるシーラント需要を促進します。さらに、日本は世界中で機関車エンジンを生産するための確立された設備を持っており、2028年までに必要なシーラントの需要を促進すると考えられます。

- シーラントは自動車産業の多様な用途に使用され、主にエンジンや自動車のガスケットに使用され、様々な基材に広範囲に接着します。日本は、広範な生産設備と大手自動車メーカーの強い存在感により、長年にわたり自動車産業における主要生産国の1つとしてマークされており、これが今後数年間のシーラント需要を生み出す可能性が高いです。

日本のシーラント市場動向

商業とインフラプロジェクトの増加が建設産業を牽引

- 日本の建設セクタは、公共・民間インフラや商業プロジェクトへの投資の増加により、今後5年間は緩やかな成長を記録すると予想されます。日本の建設用接着剤・シーラント市場は、予測期間2022~2028年にかけて、数量で約2.89%、金額で約5.35%のCAGRで推移すると予測されます。

- 日本は超高層ビルや高層建築物のセグメントで主要な地域であり、重要な消費市場となっています。日本にはさまざまな高層ビル(290棟近く)があり、東京はそうしたビルの主要拠点となっています。このようなビルの計画と建設は、短期的には日本でまともな成長を目の当たりにしています。いくつかの建設プロジェクトには、東京駅のための2つの高層タワー、37階建て高さ230mのオフィスタワー、2027年完成予定の61階建て高さ390mのオフィスタワーなどがあります。最も重要な再開発プロジェクトとしては、2023年完成予定の、古いビルを新しいオフィス、ホテル、住宅、小売、教育施設に建て替える八重洲再開発プロジェクトがあります。

- 日本では、清水建設、鹿島建設、大林組、大成建設、大和ハウスなどの大手建設会社が工事を中断しました。政府はCOVID-19のパンデミック対策を緩和し始めたが、どの程度まで仕事が正常に戻るか予測するのは難しいです。近年、COVID-19パンデミック以前は、日本の建設インフラプロジェクトの数と量は増加していました。日本がパンデミックから回復するにつれて、建設インフラプロジェクトも再開されるはずです。こうした要因により、接着剤とシーラントの需要が増加すると予想されます。

トヨタ、ホンダ、日産を含む有名自動車メーカーの本拠地であることに加え、EVの需要が自動車産業を押し上げています。

- 日本にはトヨタ、ホンダ、日産といった世界最大の自動車メーカーがあり、中でもトヨタは時価総額世界第2位の企業です。トヨタの2022年3月期の売上高は前年同期比15%増を示し、日本における自動車市場の成長動向の高まりを示唆しています。日本の乗用車販売台数は2027年までに395万1,710台に達すると予想されます。

- COVID-19パンデミックの影響により、全国的な封鎖、全体的な景気減速、輸出の減少、サプライチェーンの混乱等により、自動車の販売は大幅に減少しました。これらの要因により、乗用車販売台数は2019年の399万7,000台から2020年には384万1,000台に減少し、2020年の自動車販売台数は減少しました。

- 日本では、環境問題に対する意識の高まりと、日本の都市部における公共輸送の利用増加により、2021年の自動車市場の売上高は2020年に比べて減少しました。政府も公共輸送を以前より効率的にすることでこの原因を支援しています。日本の公共輸送の72%近くを鉄道が占めています。

- 日本では2017年に電気自動車の販売台数がピークに達したが、これは消費者にアピールした新しいプラグインハイブリッド車の発売によるものです。自動車産業の電気自動車セグメントは、2022~2027年に24.39%のCAGRで推移すると予想されます。日本で販売される電気自動車の台数は、2027年までに16万5,500台になると予想されます。これは、日本の自動車産業全体の収益の増加につながります。

日本のシーラント産業概要

日本のシーラント市場はセグメント化されており、上位5社で26.31%を占めています。この市場の主要企業は、3M、Shin-Etsu Chemical、Sika AG、THE YOKOHAMA RUBBER、ThreeBond Holdingsなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- 日本

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 医療

- その他

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- CEMEDINE Co.,Ltd.

- Henkel AG & Co. KGaA

- SEKISUI FULLER

- SHARP CHEMICAL IND. CO.,LTD.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- THE YOKOHAMA RUBBER CO., LTD.

- ThreeBond Holdings Co., Ltd.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92455

The Japan Sealants Market size is estimated at 625.48 million USD in 2024, and is expected to reach 752.56 million USD by 2028, growing at a CAGR of 4.73% during the forecast period (2024-2028).

Emerging automotive market and building & construction industry are expected to boost the consumption of sealants in Japan

- The construction industry holds the major share in the Japanese sealants market, followed by other end-user industries due to diverse applications of sealants in building and construction activities such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. Moreover, construction sealants are designed for longevity and ease of application on different substrates. The Japanese construction sector achieved about 5.3% of the nation's GDP in 2019 and is likely to register considerable growth in the upcoming years. The Japanese government focuses on the quality of buildings and promotes sustainable development, which will likely proliferate sealants demand over the forecast period.

- A variety of sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables. The Japanese electronics market registered nearly 6% of revenue share in 2021 and is likely to have promising growth in the upcoming years owing to the rapid adoption of consumer electronics among the high and middle-income groups. This, in terms, will foster the demand for sealants in the other end-user segment. Moreover, Japan has well-established facilities to produce locomotive engines around the world will drive the demand for required sealants by 2028.

- Sealants are used in diverse applications in the automotive industry, mostly used for engines and car gaskets, and exhibit extensive bonding to various substrates. Japan has been marked as one of the leading producers in the automotive industry over the years due to extensive production facilities and the strong presence of major carmakers, which is likely to create demand for sealants in the coming years.

Japan Sealants Market Trends

Rising commercial and infrastructure projects to lead the construction industry

- The construction sector in the country is expected to record moderate growth over the next five years, owing to the increasing investments in public and private infrastructure and commercial projects. The Japanese construction adhesives and sealants market is projected to record a CAGR of about 2.89% in volume and 5.35% in value during the forecast period 2022 to 2028.

- Japan is a major area in the field of skyscrapers and high-rise buildings, making it a significant market for consumption. The country hosts various high-rise buildings (nearly 290), with Tokyo being a major hub for such buildings. The planning and construction of such buildings are witnessing decent growth in Japan in the short term. Some construction projects include two high-rise towers for Tokyo Stations, a 37-story and 230 m tall office tower, and a 61-story and 390 m tall office tower, due for completion in 2027. One of the most significant redevelopment projects includes the Yaesu redevelopments project for old buildings to new offices, hotels, residential, retail, and educational facilities, which are due to be completed by 2023.

- In Japan, major construction companies, such as Shimizu, Kajima, Obayashi, Taisei, and Daiwa House, suspended construction work. Although the government has begun to ease its measures to combat the COVID-19 pandemic, it is difficult to predict to what extent work will return to normal. In recent years, before the COVID-19 pandemic, the number and volume of construction and infrastructure projects in Japan had been increasing. As Japan recovers from the pandemic, construction and infrastructure projects should also re-commence. These factors are expected to lead to an increase in the demand for adhesives and sealants.

In addition to being home to renowned automotive manufacturers including Toyota, Honda, and Nissan, the demand for EVs is rising the automotive industry

- Japan is home to the world's largest automotive companies, such as Toyota, Honda, and Nissan, of which Toyota is the world's second-largest company in terms of market capitalization. Toyota's sales revenue showed a 15% Y-o-Y growth in the fiscal year ending March 2022, suggesting an increasing trend of automotive market growth in Japan. Passenger vehicle sales in Japan are expected to reach 3951.71 thousand units by 2027.

- Due to the impact of the COVID-19 pandemic, the sales of automobiles reduced drastically because of nationwide lockdowns, overall economic slowdown, decreased exports, supply chain disruptions, etc. These factors led to a decrease in the sales volume of automobiles in 2020 as passenger car sales fell from 3997 thousand in 2019 to 3841 thousand in 2020.

- Japan witnessed a decrease in automotive market revenue in 2021 compared to 2020 because of the increasing awareness of environmental concerns and increased use of public transport in the cities of Japan. The government is also supporting the cause by making public transport more efficient than before. The railways cover nearly 72% of the public transportation system in Japan.

- Japan witnessed peak sales of electric vehicles in 2017 because of the launch of new plug-in hybrid vehicles, which appealed to consumers. The electric vehicles segment of the automotive industry is expected to record a CAGR of 24.39% in 2022-2027. The number of electric vehicles sold in Japan is expected to be 165.5 thousand by 2027. This will lead to an increase in the overall revenue of the automotive industry in Japan.

Japan Sealants Industry Overview

The Japan Sealants Market is fragmented, with the top five companies occupying 26.31%. The major players in this market are 3M, Shin-Etsu Chemical Co., Ltd., Sika AG, THE YOKOHAMA RUBBER CO., LTD. and ThreeBond Holdings Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Japan

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 CEMEDINE Co.,Ltd.

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 SEKISUI FULLER

- 6.4.6 SHARP CHEMICAL IND. CO.,LTD.

- 6.4.7 Shin-Etsu Chemical Co., Ltd.

- 6.4.8 Sika AG

- 6.4.9 THE YOKOHAMA RUBBER CO., LTD.

- 6.4.10 ThreeBond Holdings Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms