|

市場調査レポート

商品コード

1693405

シンガポールのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Singapore Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シンガポールのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 157 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

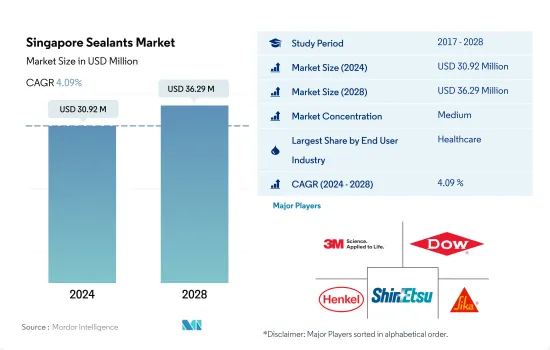

シンガポールのシーラント市場規模は2024年に3,092万米ドルと推定され、2028年には3,629万米ドルに達すると予測され、予測期間(2024-2028年)のCAGRは4.09%で成長する見込みです。

シンガポールの医療機器製造業の成長が同国のシーラント需要に大きく影響すると予測

- シンガポールのシーラント市場は、主にその他のエンドユーザー産業セグメントが支配的で、ヘルスケア産業がこれに続きます。その他のエンドユーザー産業セグメントは、エレクトロニクスと電気部品、機関車、海洋、DIYなどで構成され、そのうちエレクトロニクス産業は、多様な用途のため、主要なシェアを占めています。センサーやケーブルのシールなどに使用されます。さらに、eコマース活動の急成長と、家電セグメントの強力な市場ポジショニングが、シンガポールのシーラント市場規模を押し上げる可能性が高いです。しかし、2020年にはCOVID-19の大流行とそれに伴う規制によりエレクトロニクス産業の成長が低下し、原材料が不足しました。しかし、2021年には原材料のサプライチェーンが回復し、全国的にシーラントの需要が高まりました。

- 防水、耐候性シーリング、ひび割れシーリング、目地シーリングなどのDIY用途も最近人気を博しています。シーラントは耐用年数が長く、さまざまな基材に簡単に塗布できるように設計されています。シンガポールのDIY産業は14.31%の成長率が見込まれており、シーラント市場にとって今後数年間の余地が生まれると思われます。

- ヘルスケア産業では、主に医療機器部品の組み立てやシールにシーラントが使用されています。医療グレードのシーラントは、ガラス、金属、プラスチック、塗装面など、さまざまな基材に独自の適用性を持っており、耐候性、耐熱性、老化防止などの特徴がシーラントの需要を押し上げる可能性が高いです。シンガポールは、国内部門からの前例のない需要により、医療機器製造において大きな成長を記録すると予想されています。このような開発は、予測期間におけるシーラント需要を押し上げると予想されます。

シンガポールのシーラント市場動向

公共建築物建設への継続的かつ今後の投資がエンドユーザー産業を支える

- シンガポールの建設業界は、2022年から2028年の予測期間中に約2.6%のCAGRで推移すると予測されています。建設需要は2019年に5年ぶりの高水準に達し、推定334億SGD相当のプロジェクトが受注され、上期予測の320億SGDを上回りました。これは2018年と比較して建設需要が9.5%増加したことを表しています。しかし、2020年にはCOVID-19パンデミックの影響によりプロジェクト実施スケジュールが混乱し、建設需要の速報値は36.5%減の213億SGDとなりました。シンガポールの建設用接着剤とシーラント市場は、2022~2028年の予測期間中に数量で約2.86%、金額で約5.31%のCAGRで推移すると予測されています。

- 公共部門の建設は2019年の190億SGDから2020年には132億SGDに減少したが、これはパンデミックがリソース管理とプロジェクトスケジューリングに与える影響を検討するための時間を必要としたため、特定の大型インフラプロジェクトが延期されたためです。さらに、シンガポールの建設需要は2022年には270億~320億米ドルになると推定され、公共部門が需要全体の約60%を占めるとみられます。公共部門の建設需要は160億~190億米ドルと予想されます。

- 他方、シンガポールの住宅建設は、売れ残り建物のストックの増加により依然として低調であり、COVID-19の流行による景気後退によってさらに悪化しています。しかし、パンデミックの中、寮の人口密度を下げるため、政府は2020年末までに約6万人の出稼ぎ労働者向けに住宅を追加建設する計画を立てていました。これらの要因は、予測期間中、接着剤とシーラントの需要を抑制すると予想されます。

民間航空需要の増加が同国の航空宇宙産業を促進

- シンガポールの航空宇宙セクターはアジア太平洋市場を独占しています。シンガポールの航空宇宙セクターは過去20年間にCAGR 8.6%を記録し、2020年には年間総生産額が80億米ドルを超えます。シンガポールの重要な経済牽引役です。

- シンガポールは、予想される開発パターンを活用するため、アジア太平洋の主要な航空ハブとしてインフラの改善に努めています。チャンギ空港では、巨大なターミナル5の建設が進められています。2030年代に完成するチャンギ・ターミナル5(T5)は、世界最大級の空港ターミナルになる見込みです。初期運用段階では、T5は年間5,000万人の旅客を処理する能力を持ち、空港の年間総旅客処理能力は1億3,500万人に達します。

- チャンギ・ターミナル5の建設を急ぐとともに、シンガポールの航空業界は、パンデミックによって3万5,000人のスタッフの3分の1を失った後、2022年末までにパンデミック前の労働力の85%から90%を回復させたいと考えています。

- 民間航空はシンガポールの航空宇宙産業で最大のシェアを占めています。2020年には9機だった民間航空機が、2021年には約16機納入され、2028年には約32機の民間航空機が必要になると予測されています。さらに、企業と研究機関の間で進行中の協力関係は、シンガポールの小型衛星の能力を拡大し、革新的な宇宙サービスやアプリケーションを生み出すことを目指しています。したがって、上記のすべての要因は、調査された市場に影響を与える可能性が高いです。

シンガポールのシーラント産業概観

シンガポールのシーラント市場は適度に統合されており、上位5社で52.63%を占めています。この市場の主要企業は以下の通り。 3M, Dow, Henkel AG & Co. KGaA, Shin-Etsu Chemical and Sika AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- シンガポール

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- ヘルスケア

- その他のエンドユーザー産業

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- 3M

- ALTECO co., ltd.

- Arkema Group

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- PFE Technologies Pte Ltd

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92461

The Singapore Sealants Market size is estimated at 30.92 million USD in 2024, and is expected to reach 36.29 million USD by 2028, growing at a CAGR of 4.09% during the forecast period (2024-2028).

The forecasted growth in the medical device manufacturing of Singapore to significantly influence the sealants demand in the country

- The Singaporean sealants market is dominated mainly by the other end-user industries segment, followed by the healthcare industry. The other end-user industries segment comprises electronics and electrical components, locomotive, marine, DIY, etc., of which the electronics industry holds the major share due to the diverse applications. They are used for sealing sensors and cables, etc. Moreover, the rapid growth of e-commerce activities and the strong market positioning of the consumer electronics segment are likely to propel the size of the Singaporean sealants market. However, the electronics industry's growth declined in 2020 due to the COVID-19 pandemic and resultant restrictions, which caused a scarcity of raw materials. However, the raw materials supply chain was restored in 2021, which led to a hike in demand for sealants across the country.

- DIY applications, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing, have also recently gained popularity. Sealants are designed to provide longevity and ease of application on different substrates. The DIY industry in Singapore is expected to grow at a rate of 14.31%, which will create scope for the sealants market over the coming years.

- The healthcare industry primarily uses sealants for assembling and sealing medical device parts. Medical-grade sealants have unique applicability to various substrates such as glass, metal, plastic, painted surfaces, etc., and their features, such as weather-proofing, heat resistance, and anti-aging, are likely to boost the sealants' demand. Singapore is expected to register significant growth in medical device manufacturing due to unprecedented demand from the domestic sector. Such developments are expected to boost sealant demand over the forecast period.

Singapore Sealants Market Trends

Ongoing and upcoming investments in the construction of public buildings will support the end-user industry

- The Singaporean construction industry is projected to record a CAGR of about 2.6% during the forecast period from 2022 to 2028. The construction demand hit a five-year high in 2019, with an estimated SGD 33.4 billion worth of projects awarded, higher than its top-end projection of SGD 32 billion. This represented a 9.5% increase in construction demand compared to 2018. However, in 2020, due to the impact of the COVID-19 pandemic, which disrupted project implementation schedules, the preliminary figure for construction demand witnessed a decline of 36.5% to SGD 21.3 billion. The Singaporean construction adhesives and sealants market is projected to record a CAGR of about 2.86% in volume and 5.31% in value during the forecast period 2022-2028.

- Public sector construction declined from SGD 19 billion in 2019 to SGD 13.2 billion in 2020, as certain large infrastructure projects were postponed due to the need for more time to examine the pandemic's impact on resource management and project scheduling. Moreover, construction demand in Singapore is estimated to be between USD 27 billion and USD 32 billion in 2022, and the public sector is likely to provide roughly 60% of the overall demand. The public sector's construction demand is expected to range between USD 16 billion and USD 19 billion.

- On the other hand, residential construction in Singapore remains weak due to the growing stock of unsold buildings, further aggravated by the economic downturn due to the COVID-19 pandemic. However, to reduce the population density in dormitories amid the pandemic, the government had planned to construct additional housing for around 60,000 migrant workers by the end of 2020. These factors are expected to restrain the demand for adhesives and sealants over the forecast period.

Increasing demand from civil aviation will propel the aerospace industry in the country

- The aerospace sector in Singapore dominates the Asia-Pacific market. The Singaporean aerospace sector registered a CAGR of 8.6% during the last two decades, with a total yearly output of more than USD 8 billion in 2020. It is a significant economic driver for Singapore.

- Singapore strives to improve its infrastructure as the principal aviation hub in Asia-Pacific to capitalize on anticipated development patterns. The Changi Airport is witnessing the construction of the massive Terminal 5. When it is finished in the 2030s, Changi Terminal 5 (T5) is expected to be one of the largest airport terminals in the world. In its initial operation phase, T5 will have the capacity to handle up to 50 million passengers annually, bringing the airport's total annual passenger handling capacity to 135 million.

- Along with pressing forward with the construction of Changi Terminal 5, Singapore's aviation industry hopes to have restored 85% to 90% of its pre-COVID-19 pandemic workforce by the end of 2022 after losing a third of its 35,000 staff to the pandemic.

- Civil aviation holds the largest share of Singapore's aerospace industry. Around 16 civil aircraft were delivered to the country in 2021, compared to 9 units in 2020, and it is forecasted that around 32 civil aircraft will be needed in 2028. In addition, ongoing collaborations between businesses and research institutions aim to expand Singapore's small satellite capacity and produce innovative space services and applications. Therefore, all the abovementioned factors are likely to impact the market studied.

Singapore Sealants Industry Overview

The Singapore Sealants Market is moderately consolidated, with the top five companies occupying 52.63%. The major players in this market are 3M, Dow, Henkel AG & Co. KGaA, Shin-Etsu Chemical Co., Ltd. and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Singapore

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 ALTECO co., ltd.

- 6.4.3 Arkema Group

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 PFE Technologies Pte Ltd

- 6.4.8 Shin-Etsu Chemical Co., Ltd.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms