|

市場調査レポート

商品コード

1693398

インドのシーラント:市場シェア分析、産業動向と統計、成長予測(2025~2030年)India Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのシーラント:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

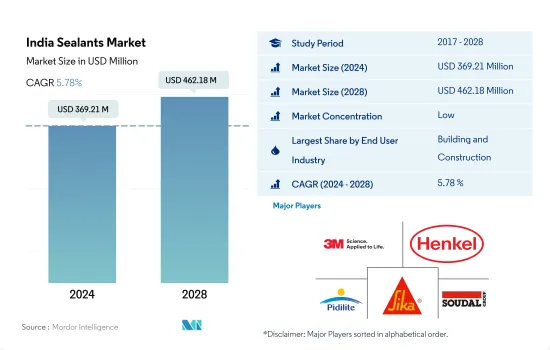

インドのシーラント市場規模は2024年に3億6,921万米ドルと推定され、2028年には4億6,218万米ドルに達すると予測され、予測期間(2024~2028年)のCAGRは5.78%で成長すると予測されます。

自動車市場と建設産業の台頭がインドのシーラント消費を押し上げる見込み

- 建設産業はインドのシーラント市場を独占しており、防水、耐候性シーリング、ひび割れシーリング、目地シーリングなど、建築・建設活動におけるシーラントの多様な用途により、その他のエンドユーザー産業がそれに続いています。建築用シーラントは、耐用年数が長く、さまざまな基材に簡単に塗布できるように設計されています。インドの建設部門は、COVID-19パンデミックの悪影響を相殺することにより、2021年には国のGDPの約9%を占めています。インド政府は低エネルギー建物とサステイナブル開発を継続的に推進しており、予測期間中にシーラントの需要が徐々に増加すると予想されます。

- 様々なシーラントは、電気機器製造においてポッティングや保護用途に使用されています。これらはセンサやケーブルなどの密封に使用されます。インドのエレクトロニクス市場は、2021年には同国のGDPの2.5%近くを占め、通信や民生用電子機器市場の需要拡大により、今後数年間は有望な成長を記録する可能性が高いです。これは、他のエンドユーザー産業セグメントにおけるシーラント需要を促進すると考えられます。インドは、機関車、海洋、DIY産業でかなりの成長を示しており、2028年までに必要なシーラントの需要を押し上げると予想されています。

- シーラントは自動車産業において多様な用途があり、主にエンジンや自動車のガスケットに使用され、様々な基材に広範囲に接着します。インドでは、パーソナルモビリティへの消費者動向の変化により、自動車生産がまともな成長を遂げており、この傾向は今後も続くとみられます。したがって、このような傾向は、予測期間2022~2028年にかけてシーラントの需要を増大させると予想されます。

インドのシーラント市場動向

Housing for All(万人のための住宅)やPradhan Mantri Awas Yojana(PMAY)といった住宅セグメントへの政府投資やイニシアチブが建設産業を牽引

- 建設産業はインド第2位の産業であり、GDP貢献度は約9%で、2019年も有望な成長を示しました。しかし、COVID-19の発生により、政府による短期間の封鎖により、建設セクタは大幅な落ち込みを見せた。建設業はインドで第2位の産業であり、GDPへの貢献度は約9%です。インドは2025年までに世界第3位の建設市場になると予想されています。さらに、建設産業は予測期間中(2022~2028年)に約3.79%のCAGRで推移すると予想されています。

- 住宅セグメントでは、政府が今後数年間で巨大プロジェクトを推進しています。政府の「万人のための住宅」構想は、2022年までに都市部の貧困層向けに2,000万戸以上の手頃な住宅を建設することを目指しています。これは住宅建設(市場最大のカテゴリー)に大きな追い風となり、2023年までに産業総額の3分の1以上を占めることになります。さらに、プラダン・マントリ・アワス・ヨジャナ(PMAY)のようなイニシアチブは、2022年までに多くの人々に手頃な価格の住宅を提供することを意図しています。また、政府は、国民が初めて家を建てたり購入したりする場合、住宅ローンの利子を一部補助することにも力を入れています。

- インドはまた、建設セグメントにおける海外投資家の大きな関心を目の当たりにしています。建設開発セクタ(タウンシップ、住宅、建設インフラ、建設開発プロジェクト)への外国直接投資(FDI)は、2,000年4月から2020年3月までに256億6,000万米ドルとなっています。全国的なインフラと建設開発の増加は、接着剤とシーラントの需要の増加につながります。

e-AMRITや自動車ローン金利の2~3%低下といった政府のイニシアティブの高まりが自動車製造を牽引

- インドの自動車産業は、2020年にはアジア太平洋で第4位の規模になります。2021年に4兆3,200億インドルピーの資金を割り当てて道路を拡大するなどの政府の取り組みにより、道路を走る自動車の数も増加しています。この成長動向は2028年まで持続すると予想されます。

- COVID-19の流行により、全国的な封鎖、サプライチェーンの混乱、全体的な景気減速のため、乗用車の販売台数は2019年の338万台から2021年には239万台へと落ち込みました。しかし、自動車ローンの金利を2~3%引き下げるなど、自動車製造部門を支援する政府の取り組みにより、2022年3月には272万台まで増加しました。乗用車部門ではマルチ・スズキが最大で、2021年の市場シェアは52%です。この成長動向は予測期間(2022~2028年)においても持続すると予想されます。

- 商用車の場合、タタ・モーターズが台数ベースで最大で、2022年3月の市場シェアは43%近くに達しています。商用車販売台数は、2020年のCOVID-19の影響による赤字経済の回復により、2021年の56万8,560台から2022年3月には71万6,570台に増加しました。2020年のCOVID-19の影響による赤字経済の回復により、2021年の56万8,560台から2022年3月には71万6,570台まで増加しました。

- e-AMRITのようなイニシアチブを持つインド政府による電気自動車製造の推進は、2028年までの数年間における電気自動車の生産増加につながります。インドで販売される電気自動車の数は、2020年と比較して2021年には108%増加します。

インドのシーラント産業概要

インドのシーラント市場は細分化されており、上位5社で21.68%を占めています。同市場の主要企業は以下の通りです。3M、Henkel AG & Co. KGaA、Pidilite Industries Ltd.、Sika AG、Soudal Holding N.V.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 医療

- その他

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- ASTRAL ADHESIVES

- Dow

- Henkel AG & Co. KGaA

- Jubilant Industries Ltd.

- Pidilite Industries Ltd.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92454

The India Sealants Market size is estimated at 369.21 million USD in 2024, and is expected to reach 462.18 million USD by 2028, growing at a CAGR of 5.78% during the forecast period (2024-2028).

Emerging automotive market and construction industry are expected to boost the consumption of sealants in India

- The construction industry dominates the Indian sealants market, followed by other end-user industries due to the diverse applications of sealants in building and construction activities, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. Construction sealants are designed for longevity and ease of application on different substrates. The Indian construction sector accounted for about 9% of the nation's GDP in 2021 by offsetting the adverse impacts of the COVID-19 pandemic. The Indian government continuously promotes low-energy buildings and sustainable development, which is expected to increase the demand for sealants over the forecast period gradually.

- Various sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Indian electronics market accounted for nearly 2.5% of the country's GDP in 2021 and is likely to record promising growth over the coming years due to the growing demand from the telecommunication and domestic appliances market. This, in turn, will foster the demand for sealants in the other end-user industry segment. India has showcased considerable growth in the locomotive, marine, and DIY industries, which is expected to boost the demand for the required sealants by 2028.

- Sealants have diverse applications in the automotive industry and exhibit extensive bonding to various substrates, mainly used for engines and car gaskets. India has achieved decent growth in automotive production due to the shifting consumer trend toward personal mobility, which is likely to continue over the coming years. Thus, such a trend is expected to augment the demand for sealants over the forecast period 2022-2028.

India Sealants Market Trends

Government investments and initiatives such as Housing for All and Pradhan Mantri Awas Yojana (PMAY) for the housing sector to lead the construction industry

- The construction industry is the second-largest industry in India, with a GDP contribution of about 9%, and it showed promising growth in 2019. However, due to the outbreak of COVID-19, the construction sector witnessed a significant decline, owing to the lockdown by the government for a brief period. The construction industry is the second-largest industry in India, with a GDP contribution of about 9%. India is expected to become the third-largest construction market in the world by 2025. Moreover, the construction industry is expected to register a CAGR of about 3.79% during the forecast period (2022 - 2028).

- In the residential segment, the government is pushing huge projects in the next few years. The government's 'Housing for All initiative aims to build more than 20 million affordable homes for the urban poor by 2022. This will provide a significant boost to residential construction (the market's largest category) and accounts for more than a third of the industry's total value by 2023. Furthermore, initiatives such as Pradhan Mantri Awas Yojana (PMAY) are intended to provide affordable homes to many people by 2022. The government is also into providing some subsidiary on interest on housing loans if a citizen builds/buys their first house.

- India is also witnessing significant interest from international investors in the construction space. Foreign Direct Investment (FDI) in the construction development sector (townships, housing, built-up infrastructure, and construction development projects) stood at USD 25.66 billion from April 2000 to March 2020. The increasing infrastructure and construction development across the nation leads to an increase in the demand for adhesives and sealants.

Rising government initiatives such as e-AMRIT and auto loan interest rates decrease by 2-3% to lead the automotive manufacturing

- The Indian automotive industry was the fourth largest in the Asia-Pacific by volume in 2020. With the government initiatives such as the expansion of roads in 2021 by allocation of funds of INR 4.32 trillion, the number of vehicles has also increased on roads. This trend of growth is expected to sustain in the coming years up to 2028.

- Due to the COVID-19 pandemic, there was a dip in sales of passenger vehicles from 3.38 million in 2019 to 2.39 million in 2021 because of nationwide lockdown, supply chain disruptions, and overall economic slowdown. But, with the government initiatives to support the automobile manufacturing sector, such as decreasing interest rates for auto loans by 2-3%, it moved up to 2.72 million vehicles by March 2022. Maruti Suzuki is the largest in the passenger vehicles segment, with a market share of 52% in 2021. This growth trend is expected to sustain in the forecast period, which is 2022-2028.

- In the case of commercial vehicles, Tata Motors is the largest vehicle producer by number, with a market share of nearly 43% in March 2022. The commercial vehicle sales increased from 568,560 in 2021 to 716570 by March 2022 because of recovering loss-ridden economy due to the impact of COVID-19 in 2020. With this growing post-pandemic economy, it is expected to increase in the mentioned period.

- The electric vehicle manufacturing push by the Indian government with initiatives such as e-AMRIT will lead increase in the production of electric vehicles in years up to 2028. The increase in the number of electric vehicles being sold in India increased by 108% in 2021 compared to 2020.

India Sealants Industry Overview

The India Sealants Market is fragmented, with the top five companies occupying 21.68%. The major players in this market are 3M, Henkel AG & Co. KGaA, Pidilite Industries Ltd., Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 India

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 ASTRAL ADHESIVES

- 6.4.4 Dow

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Jubilant Industries Ltd.

- 6.4.7 Pidilite Industries Ltd.

- 6.4.8 Sika AG

- 6.4.9 Soudal Holding N.V.

- 6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms