|

市場調査レポート

商品コード

1693393

イタリアのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Italy Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イタリアのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 162 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

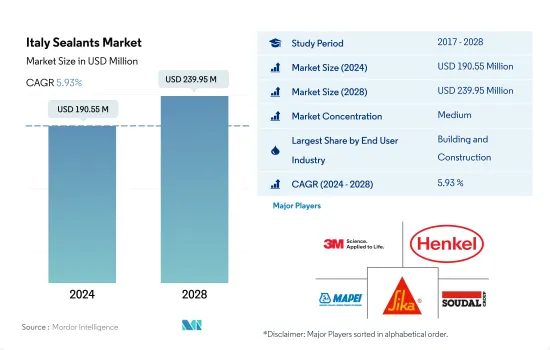

イタリアのシーラント市場規模は2024年に1億9,055万米ドルと推定され、2028年には2億3,995万米ドルに達すると予測され、予測期間(2024年~2028年)のCAGRは5.93%で成長すると予測されます。

新築と老朽化した建物の改修でシーラントの需要が高まる

- イタリアのシーラント市場は、防水、耐候性シーリング、ひび割れシーリング、目地シーリングなど、建築・建設活動におけるシーラントの用途が多岐にわたるため、主に建設業界が牽引し、その他のエンドユーザー産業セグメントがそれに続きます。イタリアの建設産業は、同国のGDPの8%近くを占めています。2018年、イタリアは建設および関連工事において49万社以上の企業を登録しました。COVID-19パンデミックの悪影響により、イタリアの建設業界の成長は2020年に10.1%減少しました。

- 様々なシーラントが、ポッティングや保護用途で電子機器や電気機器製造に広く使用されています。イタリアのエレクトロニクス市場は、大型家電、家庭用電子機器、テレフォニーの需要が高いことが主な理由で大きな成長を記録しました。これは、他のエンドユーザー産業セグメントからのシーラント需要を促進すると予想されます。機関車やDIY産業におけるシーラントの様々な用途が、2028年までにシーラントの需要を押し上げると予想されています。

- シーラントはヘルスケア産業において多様な用途があり、イタリアは数十年にわたり医療機器の製造において著しい開発を達成してきました。シーラントは、医療機器部品の組み立てやシールといったヘルスケア用途に使用されています。同国では、医療機器・技術市場に4,323社近くの企業が参入しています。イタリア政府はまた、2024年末に3,133の機器をアップグレードするために11億8,000万ユーロを投資する計画を発表しました。このような動向から、今後数年間は医療用シーラントの需要が増加することが予想されます。

イタリアのシーラント市場動向

インフラ分野への政府政策と投資の増加が建設業界を促進

- イタリアでは、公共インフラ部門への官民投資を促進するため、2017年予算法が導入されました。また、2017年から2032年の期間、同国の政府インフラ開発のために530億米ドルの予算が割り当てられました。2019年、フィレンツェ市は、より大規模な都市再開発計画の一環として、新しいスタジアムを開発するための土地も承認しました。スタジアムの収容人数は40,000人で、2023年までに完成する予定です。

- しかし、2020年には、イタリアはCOVID-19の大流行で最悪の被害を受けた国のひとつであったため、イタリアの建設市場は23%縮小しました。2021年には、イタリアの建設市場は16.59%という最高の成長率を記録しました。欧州委員会によると、イタリア政府は住宅市場を促進するためのいくつかのイニシアチブを発表しました。2021年予算法に基づき、イタリアはスーパーボーナス110%控除の期限を2022年6月30日まで延長しました。イタリア政府は、一部の都市で住宅1戸あたり最低2万米ドルを投資する建設補助金を推進し、滞在スポンサーを提供することで都市の人口を促進しています。イタリアの建設費は欧州の他の多くの地域よりもかなり安く、特に別荘の建設費は安いため、これが今後の住宅建設を後押しすると予想されます。

- イタリアの建設市場は、予測期間中(2022~2028年)にCAGR 3.2%を記録すると予想されます。政府が国全体の商業インフラやその他の土木活動の改善に注力していることから、外国直接投資や税控除に関する政府政策の変更が同国の建設業界を牽引し、ひいては市場の牽引役となることが期待されます。

電気自動車需要の高まりが自動車生産を後押しする可能性が高い

- イタリアは欧州の主要自動車メーカーのひとつです。2017年と比較して、同国の自動車生産台数は2018年に9.26%、2019年に22.2%縮小しました。2018年と2019年には、Brexitの影響、より複雑な環境規制の実施、米国と中国の緊張といった要因が、イタリアの自動車市場にマイナスの影響を与えました。

- 2020年の自動車生産台数は、2019年の同時期と比べて20%縮小しました。COVID-19の流行は自動車製造に混乱をもたらし、サプライチェーン全体に悪影響を及ぼしました。多くのサプライヤーはさらに、原材料コスト(鉄鋼、プラスチック、樹脂など)の上昇とエネルギー価格の上昇に苦しみ、同国の自動車市場に影響を与えています。

- 2020年には、電気自動車の成長がさらに加速します。2020年上半期の純EVの登録台数は、2019年比で86%増加しました。2020年には6月末までに約3万1,000台の純EVが販売されました。すべてのプラグイン車の総販売台数は5万500台に増加しました。ピュアEVの平均市場シェアも大幅に上昇し、同国の接着剤・シーリング剤市場を牽引しました。

- 同様に、2021年もイタリアのEV市場は成長を続けています。近年、電気自動車の販売台数はわずか3年で6倍に増加しました。同様に、電気自動車の市場シェアも2021年には4.6%に増加しました。そのため、同国の接着剤・シーリング剤市場の改善が期待されます。

イタリアのシーラント産業概要

イタリアのシーラント市場は適度に統合されており、上位5社で63.07%を占めています。この市場の主要企業は以下の通り。 3M, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG and Soudal Holding N.V.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- イタリア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- ヘルスケア

- その他のエンドユーザー産業

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- 3M

- Dow

- Henkel AG & Co. KGaA

- MAPEI S.p.A.

- NPT Srl

- RPM International Inc.

- Sika AG

- Soudal Holding N.V.

- Torggler S.r.l.

- Wacker Chemie AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92449

The Italy Sealants Market size is estimated at 190.55 million USD in 2024, and is expected to reach 239.95 million USD by 2028, growing at a CAGR of 5.93% during the forecast period (2024-2028).

With new construction and renovation of old buildings demand for sealants will rise

- The Italian sealants market is majorly driven by the construction industry, followed by the other end-user industries segment due to the diverse applications of sealants in building and construction activities, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. The Italian construction industry accounted for nearly 8% of the country's GDP. In 2018, Italy registered more than 490,000 companies in construction and related works. Due to the adverse impacts of the COVID-19 pandemic, the Italian construction industry's growth declined by 10.1% in 2020.

- A variety of sealants are widely used in electronics and electrical equipment manufacturing for potting and protecting applications. The Italian electronics market registered significant growth mostly due to the high demand for large household appliances, consumer electronics, and telephony. This is expected to foster the demand for sealants from the other end-user industries segment. A range of applications of sealants in the locomotive and DIY industries is expected to boost the demand for sealants by 2028.

- Sealants have diverse applications in the healthcare industry, and Italy has achieved significant development in the manufacturing of medical equipment over the decades. Sealants are used for healthcare applications such as assembling and sealing medical device parts. The country counted nearly 4,323 companies in the medical device and technology market. The Italian government also announced plans to invest EUR 1.18 billion to upgrade 3,133 devices at the end of 2024. Thus, such a trend is expected to augment the demand for medical-grade sealants over the coming years.

Italy Sealants Market Trends

Increasing government policies and investments in the infrastructure sector to propel the construction industry

- In Italy, the Budget Law 2017 was introduced to boost public and private investments in the public infrastructure sectors. A budget of USD 53 billion was also allotted for the development of government infrastructure in the country for the period 2017-2032. In 2019, the Municipality of Florence also approved land to develop a new stadium as part of the larger urban redevelopment plan. The stadium is likely to hold a capacity of 40,000 seats; it is expected to be completed by 2023.

- However, in 2020, the Italian construction market contracted by 23%, as Italy was one of the worst-hit nations during the COVID-19 pandemic. In 2021, the Italian construction market registered the highest growth rate of 16.59%. According to the European Commission, the Italian government announced several initiatives to promote the residential/housing market. Under its 2021 Budget Law, Italy extended the timeline for the super bonus, 110% deduction up to June 30, 2022. The Italian government has been promoting construction subsidies to invest a minimum of USD 20,000 per house in some cities to promote the population of the city by providing sponsorship for stay. This is expected to boost house construction in the future, as construction in Italy is significantly cheaper than in many other parts of Europe, especially for vacation homes.

- The Italian construction market is expected to register a CAGR of 3.2% during the forecast period (2022-2028). As the government focuses on improving commercial infrastructure and other civil engineering activities across the country, changes in government policies for foreign direct investments and tax deductions are expected to drive the construction industry in the country, which, in turn, is expected to drive the market.

Rising electric vehicles demand is likely to boost automotive production

- Italy is one of the major automotive manufacturers in Europe. Compared to 2017, automotive vehicle production in the country contracted by 9.26% in 2018 and 22.2% in 2019, as in 2018 and 2019, factors like the fallout from Brexit, the implementation of more complex environmental regulations, and the tensions between the United States and China negatively affected the market for automotive vehicles in Italy.

- The automotive vehicle production volume contracted by 20% in 2020 compared to the same period in 2019. The COVID-19 pandemic resulted in disruptions in car manufacturing and had a negative impact on the whole supply chain. Many suppliers additionally suffer from increased raw material costs (e.g., for steel, plastics, and resin) and higher energy prices, affecting the automotive market in the country.

- In 2020, the country's electric vehicle growth further increased. Registrations for pure EVs in the first six months of 2020 were up by 86% compared to 2019. Almost 31,000 pure EVs were sold in 2020 till the end of June. Total sales of all plug-in vehicles rose to 50,500 units. The average pure-electric market share also increased significantly, driving the market for adhesives and sealants in the country.

- Similarly, the year 2021 witnessed continued growth in the Italian EV market. In recent years, electric vehicle sales increased by six-fold in just three years. Similarly, the market share of electric vehicles increased to 4.6% in 2021. Thus, it is expected to improve the market for adhesives and sealants in the country.

Italy Sealants Industry Overview

The Italy Sealants Market is moderately consolidated, with the top five companies occupying 63.07%. The major players in this market are 3M, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Italy

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Dow

- 6.4.3 Henkel AG & Co. KGaA

- 6.4.4 MAPEI S.p.A.

- 6.4.5 NPT Srl

- 6.4.6 RPM International Inc.

- 6.4.7 Sika AG

- 6.4.8 Soudal Holding N.V.

- 6.4.9 Torggler S.r.l.

- 6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms