|

市場調査レポート

商品コード

1693380

ドイツの接着剤:市場シェア分析、産業動向、統計、成長予測(2025~2030年)Germany Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツの接着剤:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 211 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

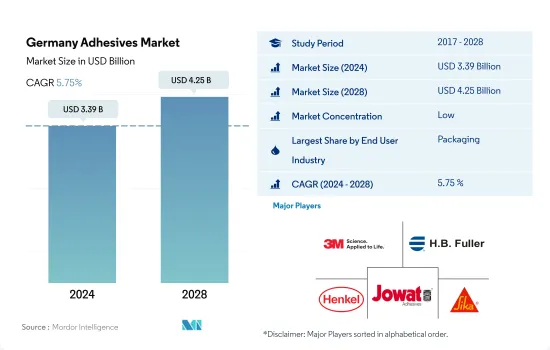

ドイツの接着剤市場規模は2024年に33億9,000万米ドルと推定・予測され、2028年には42億5,000万米ドルに達し、予測期間中(2024~2028年)にCAGR 5.75%で成長すると予測されています。

建設・リフォーム活動の拡大が接着剤需要を押し上げる

- 接着剤は、プラスチック、金属、紙・段ボール包装用途の接着に重要であるため、国内では包装産業で主に消費されています。水性接着剤は、その安価なコストと、これらのアプリケーションで必要とされる高い接着強度のため、産業で高度に消費されています。2021年には、16万1,000トン近くの水性接着剤が同国の包装産業で消費されると見られています。

- ドイツの接着剤市場は、屋根材、配管、床材など多様な用途があるため、建設産業によって大きく牽引されています。ドイツの建設産業は同国のGDPの5.9%近くを占めており、これが今後数年間の接着剤需要を促進すると考えられます。住宅施設の不足と進行中の改修工事による住宅建設プロジェクトの増加は、予測期間中にドイツの接着剤需要を増大させると考えられます。

- ドイツは数十年にわたり、医療と自動車産業で著しい開発を達成してきました。接着剤は、医療機器部品の組み立てやシールなど、医療セグメントの用途に使用されています。自動車産業では、ガラス、金属、プラスチック、塗装面など、さまざまな基材に接着剤が使用されています。ドイツは、2021年のプレミアムカーの生産台数で市場シェアの約23%を占めています。ドイツの自動車とOEMは、二酸化炭素排出量を削減するために電気自動車の製造に注力し、産業標準を満たすために車両重量を維持しています。これらの要因は、近い将来、自動車とOEMの生産を増強し、自動車用接着剤の需要に徐々に影響を与えます。

ドイツの接着剤市場動向

プラスチックのリサイクル性と飲食品産業の需要の先進包装により、プラスチック包装が包装産業をリードする

- COVID-19パンデミックにより、国全体の製造施設の閉鎖や一時的な操業停止により、サプライチェーンの混乱や輸出入取引など、いくつかの問題が発生しました。その結果、同国の包装生産量は2020年に前年比5%減少し、市場に大きな影響を与えました。

- ドイツは欧州最大のeコマース市場の1つであり、欧州で2番目に人口が多いため、包装生産市場を牽引すると考えられます。欧州の平均と比較して、ドイツはオンラインショッピング利用者数、インターネット利用者の割合、年間平均消費額が高いです。オンラインで販売される商品の総売上高は、2021年には約991億ユーロに達し、2020年の833億ユーロに比べて増加します。

- 2021年に生産される包装の約79%を占めます。プラスチック包装産業は、国内の飲食品産業の急成長によって大きく牽引されています。加えて、プラスチックのリサイクル性の向上により、プラスチック生産部門は予測期間中にCAGR約3.32%という最も速い成長率を記録する可能性が高いです。したがって、上記のすべての要因は、国内の今後数年間の包装需要をさらに繁栄させると考えられます。

自動車メーカーに対する政府の規制にもかかわらず、電気自動車の需要は自動車産業を推進すると考えられます。

- 自動車製造業はドイツで最も重要な産業であり、国内産業収益の24%はこの産業から生み出されています。ドイツの自動車生産台数は2018年第3四半期に9.4%減少したが、これは同国が2018年後半に景気減速に見舞われたことに加え、新しい世界調和小型車検査方法(WLTP)の実施における問題が重なったためです。

- ドイツで生産される自動車ユニットの75%以上は国際市場向けであり、主に米国、中国、その他のEU諸国です。米国と中国の貿易摩擦は2019年の世界需要を減退させました。これに加え、新たに販売される自動車の平均CO2排出量を1キロメートル当たり95グラムにすることを自動車メーカーに義務付けるEU-28のCO2排出量の新基準が加わり、国内での自動車生産は一時的に制限されました。

- 2020年、COVID-19の大流行は、すでに減少していた自動車生産に大きな打撃を与えました。2020年の自動車生産台数は前年比24.5%減少し、その直後に発生したサプライチェーンの制約と2021年の半導体チップ不足が相まって、自動車生産台数は2020年の水準に比べてさらに10.8%減少しました。チップ不足とサプライチェーン制約の長期的な影響により、予測期間中のドイツの自動車生産は制限されると予想されます。ドイツ政府のe-モビリティ計画では、2030年までに1,500万台のEVの普及を目指しています。これにより、同国の自動車生産は増加すると予想されます。これらすべての要因により、ドイツの自動車生産は予測期間中に増加すると予想されます。

ドイツの接着剤産業概要

ドイツの接着剤市場は細分化されており、上位5社で37.88%を占めています。この市場の主要企業は、3M、H.B. Fuller Company、Henkel AG & Co. KGaA、Jowat SE、Sika AGなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 靴と皮革

- 包装

- 木工・建具

- 規制の枠組み

- ドイツ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- フットウェアと皮革

- 医療

- 包装

- 木工・建具

- その他

- 技術

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型接着剤

- 水性

- 樹脂

- アクリル系

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- KLEBCHEMIE M. G. Becker GmbH & Co. KG

- Sika AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92435

The Germany Adhesives Market size is estimated at 3.39 billion USD in 2024, and is expected to reach 4.25 billion USD by 2028, growing at a CAGR of 5.75% during the forecast period (2024-2028).

Growing construction and renovation activities to boost the demand for adhesives

- Adhesives are majorly consumed in the packaging industry in the country owing to their importance in bonding plastics, metals, and paper & cardboard packaging applications. Waterborne adhesives are highly consumed in the industry because of their cheaper cost and high bonding strength which is required in these applications. It is seen that nearly 161 thousand tons of water-borne adhesives are consumed in the packaging industry of the country during 2021.

- The German adhesives market is majorly driven by the construction industry due to diverse applications, such as roofing, plumbing, and flooring. The construction industry of Germany obtained nearly 5.9% of the country's GDP, which will propel the adhesives demand in the coming years. The increasing growth of residential construction projects due to the shortage in housing facilities and ongoing renovating works will augment the adhesives demand in Germany during the forecast period.

- Germany has achieved significant development in the healthcare and automotive industries over the decades. Adhesives are used in applications in healthcare, such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of adhesives to various substrates, such as glass, metal, plastic, and painted surfaces. Germany has registered about 23% of the market share in terms of the production of premium cars in 2021. German automotive and OEMs focus on manufacturing electric vehicles to reduce carbon emissions and maintain vehicle weight to meet the industry standard. These factors will augment automotive and OEM production in the near future, which gradually influences the demand for automotive adhesives.

Germany Adhesives Market Trends

With the advancement in plastic recyclability and demand for food and beverage industry, plastic packaging to lead the packaging industry

- With the rise in busier lifestyles, greater spending power, and related factors in the country, the demand for quick and on-the-go packaged products is increasing.Due to the COVID-19 pandemic, the country-wide lockdowns and temporary shutdown of manufacturing facilities caused several issues, including supply chain disruptions and imports and exports trade. As a result, the country's packaging production declined by 5% in 2020 compared to the previous year, significantly affecting the market.

- Germany is one of the biggest e-commerce markets in Europe and has the second largest population in Europe, which will drive the packaging production market. Compared to Europe's average, Germany has a high number of online shoppers, the percentage of people using the internet, and the average annual spending. Total sales of goods sold online reached around EUR 99.1 billion in 2021, an increase compared to EUR 83.3 billion in 2020.

- Packaging production is majorly driven by plastics in the country, which nearly accounts for around 79% of the packaging produced in 2021. The plastic packaging industry is majorly driven by the rapid growth of the food and beverages industry in the country. In addition, with the advancement of plastic recyclability, the plastic production segment is likely to register the fastest growth rate of around 3.32% CAGR during the projected period. Therefore, all the above-mentioned factors will further thrive the packaging demand in the coming years in the country.

Despite the government regulations on carmakers, electrical vehicles demand is likely to propel the automotive industry

- The automotive manufacturing industry is the most important industry in Germany, and 24% of the domestic industry revenue is generated from this industry. Automotive production in Germany declined by 9.4% in the third quarter of 2018, as the country experienced an economic slowdown in the second half of 2018, coupled with the problems in the implementation of the new Worldwide Harmonized Light-Duty Vehicles Test Procedure (WLTP).

- Over 75% of the automotive units manufactured in Germany are destined for international markets, which are mainly the United States, China, and other EU countries. The trade conflicts between the United States and China sapped away the global demand in 2019. This, coupled with the new EU-28 standard of CO2 emissions, which mandates carmakers to achieve average CO2 emissions of 95 grams per kilometer across newly-sold vehicles, has briefly restricted automotive production in the country.

- In 2020, the COVID-19 pandemic hit hard on the already declining automotive production. In 2020, automotive production fell by 24.5% Y-o-Y, and the supply chain constraints that quickly followed, coupled with the semiconductor chip shortage in 2021, have further declined automotive production by 10.8% compared to 2020 levels. The long-lasting effects of chip shortages and supply chain restrictions are expected to restrict automotive production in Germany in the forecast period. The German government's e-mobility plan aims to achieve 15 million EVs on the road by 2030. This is expected to drive up automotive production in the country. Due to all these factors, Germany's automotive production is expected to increase during the forecast period.

Germany Adhesives Industry Overview

The Germany Adhesives Market is fragmented, with the top five companies occupying 37.88%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Jowat SE and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Germany

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Jowat SE

- 6.4.9 KLEBCHEMIE M. G. Becker GmbH & Co. KG

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms