|

市場調査レポート

商品コード

1692087

イタリアの接着剤:市場シェア分析、産業動向、成長予測(2025年~2030年)Italy Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イタリアの接着剤:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 211 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

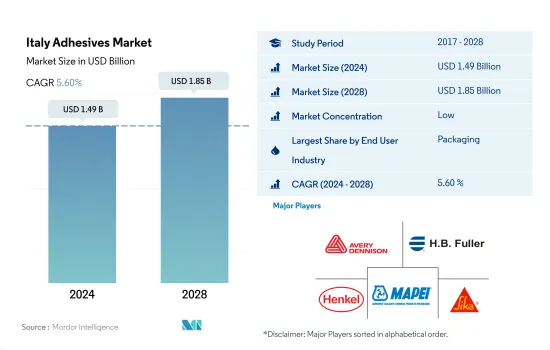

イタリアの接着剤市場規模は2024年に14億9,000万米ドルと推定・予測され、2028年には18億5,000万米ドルに達し、予測期間中(2024年~2028年)にCAGR 5.60%で成長すると予測されています。

家具市場の台頭と軟包装の動向の進展がイタリアの接着剤消費を押し上げる見通し

- 接着剤は、あらゆる産業で使用される様々な基材を接着・接合する上で重要な役割を果たしています。これらの接着剤は、メーカーがコンポーネントやアセンブリの重量を低減し、迅速、簡単かつ正確に接合部を形成するのに役立ちます。2020年にはCOVID-19の大流行の影響を受け、2019年と比較して消費量が10.38%減少しました。

- 同国では包装セクターが著しい成長を遂げています。包装産業は、電子機器、消費財、医療、食品産業向けのコールドチェーン・ソリューションや輸送用包装など、特定の用途を持っています。イタリアの包装産業は、欧州で最大の産業のひとつです。国内には7,000社近くの大手および中小の包装会社が存在します。スーパーマーケット小売の重要性が増し、消費者の購買習慣が変化していることから、同国では包装用途の接着剤需要が増加しています。

- イタリアは、世界中で人気のあるイタリア家具で知られています。そのため、接着剤はイタリアの木工産業で多く消費されています。2021年には、約6万3,030トンの接着剤がこの産業で消費され、その年の接着剤の国内第2位のエンドユーザーでした。水性接着剤は環境に優しく、他のタイプの接着剤に比べて安価に入手できるため、この産業で多く消費されています。これらの接着剤のコストは、他の接着剤に比べてほぼ半分です。

- 同国におけるフレキシブル包装や住宅リフォームの動向の高まりは、今後数年間、イタリアにおける接着剤需要を牽引すると予想されます。

イタリアの接着剤市場動向

イタリアにおける安価で軽量な包装の傾向の高まりが、軟質および硬質プラスチック包装の需要を牽引

- イタリアの一人当たりGDPは3万4,780米ドルで、2022年の成長率は前年比2.3%です。包装産業部門は同国のGDPの約0.36%に寄与しています。イタリアはドイツに次いで欧州で2番目に大きな包装産業です。イタリアの包装産業に影響を与えている要因は、貿易交流、雇用、ワイン生産、政府の政策支援などです。

- イタリアはCOVID-19パンデミックの影響により経済減速を目の当たりにしました。同年の生産量は2019年比で3.75%減少しました。これは、サプライチェーンの混乱、労働力不足、3カ月近くにわたる国内封鎖のために起こりました。2021年には景気回復のため国際国境が開放され、その結果、生産用の原材料が定期的に供給されるようになり、同年に3,500トン増加しました。

- 欧州連合(EU)では、包装の生産額は年間4,000億米ドルに達し、そのうち15%がイタリアで生産されています。同国の包装産業は紙・板紙包装分野が中心で、これは欧州第2位です。包装の主な用途は、飲食品(29%)とヘルスケア・美容製品包装(26%)です。

- 段ボール箱包装ではイタリアが欧州第2位です。フランスでは、安価で軽量な包装の動向が高まっており、今後数年間は軟包装と硬質プラスチック包装の需要を牽引すると予想されます。したがって、同国の包装業界の成長につながると期待されています。イタリアは世界最大のワイン生産国です。しかし、同国におけるワイン生産量の減少は、将来的に包装製品に支障をきたす可能性があります。2021年のワイン生産量は前年比9%減少しました。

電気自動車需要の増加が自動車生産を押し上げる可能性が高い

- イタリアは欧州の主要自動車メーカーのひとつです。2017年と比較して、同国の自動車生産台数は2018年に9.26%、2019年に22.2%縮小しました。2018年と2019年には、Brexitの影響、より複雑な環境規制の実施、米国と中国の緊張といった要因が、イタリアの自動車市場に悪影響を及ぼしたためです。

- 2020年の自動車生産台数は、2019年の同時期と比べて20%縮小しました。COVID-19の流行は自動車製造に混乱をもたらし、サプライチェーン全体に悪影響を及ぼしました。多くのサプライヤーはさらに、原材料コスト(鉄鋼、プラスチック、樹脂など)の上昇とエネルギー価格の上昇に苦しみ、同国の自動車市場に影響を与えています。

- 2020年には、電気自動車の成長がさらに加速します。2020年上半期の純EVの登録台数は、2019年比で86%増加しました。2020年には6月末までに約3万1,000台の純EVが販売されました。すべてのプラグイン車の総販売台数は5万500台に増加しました。ピュアEVの平均市場シェアも大幅に上昇し、同国の接着剤・シーリング剤市場を牽引しました。

- 同様に、2021年もイタリアのEV市場は成長を続けています。近年、電気自動車の販売台数はわずか3年で6倍に増加しました。同様に、電気自動車の市場シェアも2021年には4.6%に増加しました。そのため、同国の接着剤・シーリング剤市場の改善が期待されています。

イタリアの接着剤産業の概要

イタリアの接着剤市場は細分化されており、上位5社で34.73%を占めています。この市場の主要企業は以下の通り。 AVERY DENNISON CORPORATION, H.B. Fuller Company, Henkel AG & Co. KGaA, MAPEI S.p.A. and Sika AG(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- 包装

- 木工・建具

- 規制の枠組み

- イタリア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 履物および皮革

- ヘルスケア

- 包装

- 木工・建具

- その他のエンドユーザー産業

- 技術

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型接着剤

- 水系

- 樹脂

- アクリル系

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他の樹脂

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- DURANTE ADESIVI S.p.A.

- FRATELLI ZUCCHINI S.p.A.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI S.p.A.

- Sika AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤・シーリング剤産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 90429

The Italy Adhesives Market size is estimated at 1.49 billion USD in 2024, and is expected to reach 1.85 billion USD by 2028, growing at a CAGR of 5.60% during the forecast period (2024-2028).

Emerging furniture market and evolving trend of flexible packaging expected to boost the consumption of adhesives in Italy

- Adhesives play an important role in bonding and joining various substrates that are used across industries. These adhesives help manufacturers lower the weight of their components and assemblies and form joints quickly, easily, and accurately. The COVID-19 pandemic impacted the country in 2020, which reduced consumption by 10.38% compared to 2019.

- The packaging sector has been experiencing significant growth in the country. The packaging industry has specific applications, such as cold chain solutions and transport packaging for electronics, consumer goods, medical, and food industries. The Italian packaging industry is one of the largest industries in Europe. There are nearly 7,000 active major and minor packaging companies in the country. The increasing importance of supermarket retailing and the changing consumer buying habits are increasing the demand for adhesives in packaging applications in the country.

- Italy is known for its Italian furniture, which is popular around the world. Therefore, adhesives are largely consumed in the woodworking industry in Italy. In 2021, around 63,030 tons of adhesives were consumed by this industry, which is the second-largest end user of adhesives in the country during that year. Water-borne adhesives are largely consumed in this industry, as they are eco-friendly and cheaply available compared to other types of adhesives. The cost of these adhesives is nearly half compared to other adhesives.

- The rising trend of flexible packaging and home renovation in the country is expected to drive the demand for adhesives in the coming years in Italy.

Italy Adhesives Market Trends

Rising trend of cheap and lightweight packaging in Italy drives the demand for flexible and rigid plastic packaging

- Italy has a GDP of USD 34,780 per capita with a growth rate of 2.3% Y-o-Y in 2022. The packaging industry sector contributes to around 0.36% of the country's GDP. Italy is the second-largest packaging industry in Europe after Germany. Factors that are affecting the Italian packaging industry are trade exchange, employment, wine production, government policy support, etc.

- The country witnessed an economic slowdown because of the impact of the COVID-19 pandemic. The production volume was reduced by 3.75% in the same year compared to 2019. This happened due to a supply chain disruption, labor shortages, and a lockdown in the country for nearly three months. International borders were opened in 2021 because of the economic recovery, which resulted in a regular supply of raw materials for production that increased by 3500 tons in 2021.

- In the European Union, packaging production reaches USD 400 billion annually, out of which 15% of the share is produced in Italy. The packaging industry in the country is dominated by the paper and paperboard packaging segment, which is the second largest in Europe. Packaging is majorly used in food and beverages (29%) and healthcare and beauty products packaging (26%).

- Italy is the second largest in corrugated box packaging in Europe. The rising trend of cheap and lightweight packaging in France is expected to drive the demand for flexible packaging and rigid plastic packaging in the coming years. Hence, it is expected to lead to the growth of the packaging industry in the country. Italy is the world's largest producer of wine. However, declining wine production in the country may hinder packaging products in the future. Wine production was reduced by 9% Y-o-Y in 2021.

Rising electric vehicles demand is likely to boost automotive production

- Italy is one of the major automotive manufacturers in Europe. Compared to 2017, automotive vehicle production in the country contracted by 9.26% in 2018 and 22.2% in 2019, as in 2018 and 2019, factors like the fallout from Brexit, the implementation of more complex environmental regulations, and the tensions between the United States and China negatively affected the market for automotive vehicles in Italy.

- The automotive vehicle production volume contracted by 20% in 2020 compared to the same period in 2019. The COVID-19 pandemic resulted in disruptions in car manufacturing and had a negative impact on the whole supply chain. Many suppliers additionally suffer from increased raw material costs (e.g., for steel, plastics, and resin) and higher energy prices, affecting the automotive market in the country.

- In 2020, the country's electric vehicle growth further increased. Registrations for pure EVs in the first six months of 2020 were up by 86% compared to 2019. Almost 31,000 pure EVs were sold in 2020 till the end of June. Total sales of all plug-in vehicles rose to 50,500 units. The average pure-electric market share also increased significantly, driving the market for adhesives and sealants in the country.

- Similarly, the year 2021 witnessed continued growth in the Italian EV market. In recent years, electric vehicle sales increased by six-fold in just three years. Similarly, the market share of electric vehicles increased to 4.6% in 2021. Thus, it is expected to improve the market for adhesives and sealants in the country.

Italy Adhesive Industry Overview

The Italy Adhesives Market is fragmented, with the top five companies occupying 34.73%. The major players in this market are AVERY DENNISON CORPORATION, H.B. Fuller Company, Henkel AG & Co. KGaA, MAPEI S.p.A. and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Italy

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 DURANTE ADESIVI S.p.A.

- 6.4.5 FRATELLI ZUCCHINI S.p.A.

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms