|

市場調査レポート

商品コード

1692575

EVA接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)EVA Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| EVA接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 323 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

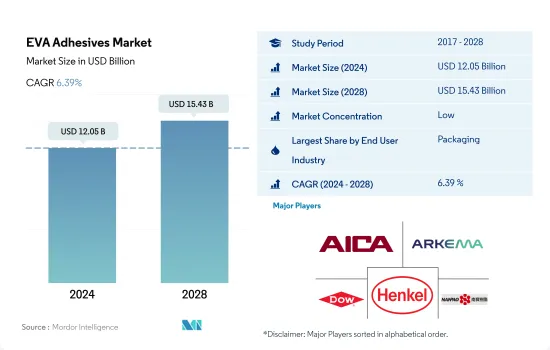

EVA接着剤市場規模は2024年に120億5,000万米ドルと推定され、2028年には154億3,000万米ドルに達すると予測され、予測期間中(2024-2028年)のCAGRは6.39%で成長する見込みです。

ヘルスケアが最も急成長するエンドユーザーである一方、包装は依然としてポールポジションにある

- EVA接着剤は世界的に、包装、自動車、木工・建具、建築・建設など、さまざまなエンドユーザー産業に応用されています。これらの接着剤は、紙、木材、プラスチック、ゴム、金属、皮革などの基材と接着することができます。これらの接着剤の主な用途としては、紙/カードストック箱、パッケージのラベリング、カートンのシール、組み立て、自動車の内装、紙の変換などがあります。

- EVA接着剤の世界需要は2017年から2019年にかけて大きく伸びた。北米地域の木工・建具産業が、全地域のエンドユーザー産業の中で最も高い需要の伸び(CAGR 9.00%)を示しました。家具製品に対する輸入関税の増加により、国内の木工産業が成長しました。

- 2020年、EVA接着剤の需要は、操業や貿易の制限、サプライチェーンの制約、労働力不足など様々な要因により、すべてのエンドユーザー産業から減少しました。自動車産業からの需要が最も苦しく、前年比14.72%減少しました。旅行活動の減少、原材料不足、その他の様々な要因がこの落ち込みを引き起こしました。規制が緩和されるにつれて、世界のEVA接着剤需要は2021年に流行前の水準まで急速に上昇しました。

- この成長動向は予測期間中も続くと予想されます。数量ベースでは、すべてのエンドユーザー産業を合わせたEVA接着剤の需要は成長し、予測期間中のCAGRは4.32%を記録すると予想されます。包装業界は、その速硬化特性からEVA接着剤を好むため、需要の最大シェアを占めています。同業界は予測期間中、最大のエンドユーザーであり続けると予想されます。

EVA接着剤の需要を押し上げる世界の建設・自動車産業の成長

- アジア太平洋地域は、多くの建設・包装活動、自動車、医療機器、航空宇宙産業の生産能力、その他の確立されたエンドユーザー産業があるため、調査期間を通じてEVA樹脂系接着剤の需要で最大のシェアを占めています。中国は、世界最大の建設および自動車市場であり、アジア太平洋地域の需要の最大58%を生み出しています。

- 2017年から2019年にかけて、欧州とアジア太平洋地域の成長鈍化により、EVA樹脂系接着剤の需要は低迷しました。主要なエンドユーザー産業である建設産業と自動車産業からの需要が世界的に減少したことにより、2018年と2019年のEVA接着剤の全体的な成長は、以前と比較して約3%(数量ベース)に制限されました。

- 2020年には、COVID-19の流行により、すべてのエンドユーザー産業からのEVA接着剤の需要が減少しました。ドイツ、ロシア、南アフリカ、ブラジルのような一部の国では、パンデミックの間、建設活動が不可欠とみなされ、操業が許可されました。このような要因が世界の影響を緩和し、2020年のEVA接着剤の減少を2019年比で約6.75%抑制した(数量ベース)。

- 2021年には、米国、オーストラリア、欧州連合(EU)諸国などの救済策や支援制度により、需要が回復し始め、この成長動向は予測期間を通じて継続すると予想されます。欧州、南米、アジア太平洋諸国で見られる投資と予算配分の増加は、この成長を促進すると予想されます。

世界のEVA接着剤市場動向

開発途上国におけるeコマース産業の急成長により、業界は拡大する

- 2020年、包装業界は複数の長期的動向が需要増を牽引する形でスタートし、経済活動がCOVID-19パンデミックによる課題に対処する方向に転換するにつれて成長が加速しました。業界の堅調な業績は、収益の増加と、飲食品やヘルスケアなどの重要な最終市場の拡大を支え、また、経済全体が不透明な時期にも業界の全般的な安定性を実証しました。

- 2020年のパンデミック(世界的大流行)でほとんどディールメーキングが停止した後、売り手と買い手が熱心に市場に戻ってきたため、2021年のパッケージングM&A活動は急増しました。パンデミックの間、パッケージング企業の好調な業績は、パッケージング業界が全般的な市場の混乱時に安定性を提供するという考えを強化しました。パンデミックはまた、eコマースの急速な拡大や、スーパーマーケットの棚で製品を差別化するためにパッケージングを採用するブランドオーナーなど、以前からあった追い風を強化し、このセクターをより強力な長期成長へと位置づけた。

- 現在のところ、溶解可能な包装、省スペース包装、スマート包装は、包装業界で出てきたいくつかのイノベーションです。食用包装の採用は、化石燃料への依存を軽減し、カーボンフットプリントを大幅に減少させる可能性を秘めた興味深く革新的な代替手段であり、その持続可能性により食品業界全体に普及しつつあります。これらの要因は、飲食品分野における包装業界の成長機会を生み出しており、予測期間中の包装業界の成長を後押しすると期待されています。

電気自動車を促進する有利な政府政策が自動車産業を促進する

- 2021年以降、世界の自動車産業は安定的に成長すると予想されているが、消費者の乗用車の個人所有に対する嗜好が低下し、移動における共有モビリティに対する嗜好が高まっているため、成長ペースは鈍化しています。世界の自動車産業の成長率は年率2%で、予測期間中の総収益の付加価値は1兆5,000億米ドルに達すると予想されます。

- 2020年には、COVID-19パンデミックの影響により、自動車販売台数は減少したが、2021年には急速に回復しました。自動車市場は通常、GDPに大きく貢献しているため、各国政府が経済支援策を講じたからです。自動車販売台数は、2019年の乗用車9,000万台から2020年には7,800万台に減少しました。

- 世界の電気自動車の導入は、その安価なエネルギーコスト、環境に優しい性質、効率的なモビリティ機能により、世界の自動車市場全体の収益に大きく貢献しています。また、さまざまな政府の政策や基準も、電気自動車の生産を増加させる原動力となっています。例えば、EUのCO2排出量基準は、2021年に電気自動車の需要を増加させました。IEAの持続可能なシナリオによれば、2030年までに2億3,000万台の電気自動車が燃焼燃料を使用する自動車に取って代わる必要があります。2021年には、最大のEVメーカーであるテスラが、電気自動車の製造台数で157%の増加を記録しました。電気自動車を好む消費者の動向は、予測期間中(2022-2028年)にさらに高まると予想されます。

EVA接着剤産業の概要

EVA接着剤市場は細分化されており、上位5社で9.33%を占めています。この市場の主要企業は以下の通りです。 Aica Kogyo, Arkema Group, Dow, Henkel AG & Co. KGaA and NANPAO RESINS CHEMICAL GROUP(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 靴・皮革

- 包装

- 木工・建具

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- 中国

- EU

- インド

- インドネシア

- 日本

- マレーシア

- メキシコ

- ロシア

- サウジアラビア

- シンガポール

- 南アフリカ

- 韓国

- タイ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- ヘルスケア

- 包装

- 木工・建具

- その他のエンドユーザー産業

- テクノロジー

- ホットメルト

- 溶剤系

- 水性

- 地域

- アジア太平洋

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- その他アジア太平洋地域

- 欧州

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他欧州

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 北米

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- アルゼンチン

- ブラジル

- その他南米

- アジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Aica Kogyo Co..Ltd.

- Arkema Group

- Beardow Adams

- CEMEDINE Co.,Ltd.

- Dow

- Follmann Chemie GmbH

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- KLEBCHEMIE M. G. Becker GmbH & Co. KG

- NANPAO RESINS CHEMICAL GROUP

- OKONG Corp.

- Paramelt B.V.

- Selic Corp Public Company Limited.

- Soudal Holding N.V.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92412

The EVA Adhesives Market size is estimated at 12.05 billion USD in 2024, and is expected to reach 15.43 billion USD by 2028, growing at a CAGR of 6.39% during the forecast period (2024-2028).

Healthcare is the fastest-growing end-user while packaging remains as pole position

- Globally, EVA adhesives find applications in a range of end-user industries, including packaging, automotive, woodworking and joinery, and building and construction. These adhesives can bond with substrates like paper, wood, plastics, rubbers, metals, and leather. Some major applications of these adhesives are paper/card stock boxes, package labeling, carton sealing, assembly, vehicle interiors, and paper conversion.

- The global demand for EVA adhesives grew significantly from 2017 to 2019. The woodworking and joinery industry in the North American region has witnessed the highest growth (CAGR of 9.00%) in demand among all end-user industries from all regions. Increased import duties on furniture products resulted in growth in the domestic woodworking industry.

- In 2020, the demand for EVA adhesives declined from all end-user industries because of various factors such as operational and trade restrictions, supply chain constraints, labor shortages, and other factors. The demand from the automotive industry suffered the most, declining by 14.72% Y-o-Y. Reduced travel activity, shortage of raw materials, and various other factors have caused this decline. As the restrictions eased, the global EVA adhesives demand quickly rose to pre-pandemic levels in 2021.

- This growth trend is expected to continue during the forecast period. In volume terms, the demand for EVA adhesives from all end-user industries combined is expected to grow, recording a CAGR of 4.32% during the forecast period. The packaging industry favors EVA adhesives because of their fast-curing properties and thus occupies the largest share of the demand. The industry is expected to remain the largest end-user during the forecast period.

Growing construction and automotive activities across the globe to boost the demand for EVA adhesives

- Asia-Pacific occupied the largest share of the demand for EVA resin-based adhesives throughout the study period because of the large number of construction and packaging activities, automotive, medical devices, and aerospace production capacities, and other well-established end-user industries in the region. China is the largest construction and automotive market globally and generates up to 58% of the demand from the Asia-Pacific region.

- During 2017-2019, the demand for EVA resin-based adhesives was sluggish due to the slow growth in the European and Asia-Pacific regions. The global decline in the demand from construction and automotive end-user industries, which are among the major end-user industries, has restricted the overall growth of EVA adhesives to around 3% (in terms of volume) in 2018 and 2019 compared to previous years.

- In 2020, the demand for EVA adhesives from all end-user industries declined because of the COVID-19 pandemic. In some countries like Germany, Russia, South Africa, and Brazil, construction activities were deemed essential and were allowed to operate during the pandemic. Factors like these have cushioned the global impact restricting the decline of EVA adhesives by around -6.75% in 2020 compared to 2019 (in terms of volume).

- In 2021, due to the relief packages and support schemes in countries like the United States, Australia, and countries in the European Union, the demand started to recover, and this growth trend is expected to continue throughout the forecast period. Increased investments and budget allotments witnessed in European, South American, and Asia-Pacific countries are expected to drive this growth.

Global EVA Adhesives Market Trends

Fast paced growth of e-commerce industry in developing nations to augment the industry

- In 2020, the packaging industry started with multiple long-term trends driving higher demand, and growth accelerated as economic activity switched to address the challenges posed by the COVID-19 pandemic. The industry's robust performance supported rising revenues and the expansion of important end markets such as food and beverage and healthcare and also demonstrated the industry's general stability during a period of overall economic uncertainty.

- Packaging M&A activities soared in 2021, as buyers and sellers enthusiastically returned to the market after deal-making almost ceased during the pandemic in 2020. During the pandemic, the strong performance of packaging companies reinforced the idea that the industry offers stability during moments of general market turbulence. The pandemic also strengthened previously existing tailwinds, including rapid e-commerce expansion and brand owners employing packaging to differentiate their products on supermarket shelves, positioning the sector for stronger long-term growth.

- As of now, dissolvable packaging, space-saving packaging, and smart packaging are a few innovations that have come up in the packaging industry. The adoption of edible packaging, an interesting and innovative alternative that alleviates the reliance on fossil fuels and has the potential to significantly decrease the carbon footprint, is now becoming popular across the food industry owing to its sustainability. These factors have created a growth opportunity for the packaging industry in the food and beverage sector, which is expected to boost the packaging industry's growth during the forecast period.

Favorable government policies to promote electric vehicles will propel automotive industry

- Since 2021, the global automotive industry has been expected to grow steadily but at a slower pace because of the decline in consumers' preferences for individual ownership of passenger vehicles and their increased preference for shared mobility in transportation. The global automotive industry is expected to experience a growth rate of 2% annually, with an expected value addition of USD 1.5 trillion in total revenue during the forecast period.

- In 2020, due to the impact of the COVID-19 pandemic, vehicle sales declined but recovered rapidly in 2021 because the governments of various countries took measures to support their economies, as automotive markets usually contribute majorly to their GDP. Vehicle sales declined from 90 million units of passenger vehicles in 2019 to 78 million units in 2020.

- The introduction of electric vehicles worldwide has contributed significantly to the overall revenue of the global automotive market because of their cheaper energy costs, environmentally benign nature, and efficient mobility features. Various government policies and standards also work as driving factors to increase EV production. For instance, the EU standards for CO2 emissions increased the demand for electric vehicles in 2021. As per the IEA's Sustainable Scenario, 230 million electric vehicles are required to replace combustion fuel-based vehicles by 2030. In 2021, Tesla, the largest EV manufacturer, recorded a rise of 157% in the number of electric vehicles manufactured. This growing trend of consumers preferring electric vehicles is expected to rise further during the forecast period (2022-2028).

EVA Adhesives Industry Overview

The EVA Adhesives Market is fragmented, with the top five companies occupying 9.33%. The major players in this market are Aica Kogyo Co..Ltd., Arkema Group, Dow, Henkel AG & Co. KGaA and NANPAO RESINS CHEMICAL GROUP (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Argentina

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 EU

- 4.2.7 India

- 4.2.8 Indonesia

- 4.2.9 Japan

- 4.2.10 Malaysia

- 4.2.11 Mexico

- 4.2.12 Russia

- 4.2.13 Saudi Arabia

- 4.2.14 Singapore

- 4.2.15 South Africa

- 4.2.16 South Korea

- 4.2.17 Thailand

- 4.2.18 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Solvent-borne

- 5.2.3 Water-borne

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 Singapore

- 5.3.1.8 South Korea

- 5.3.1.9 Thailand

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 United Kingdom

- 5.3.2.7 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Saudi Arabia

- 5.3.3.2 South Africa

- 5.3.3.3 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Aica Kogyo Co..Ltd.

- 6.4.2 Arkema Group

- 6.4.3 Beardow Adams

- 6.4.4 CEMEDINE Co.,Ltd.

- 6.4.5 Dow

- 6.4.6 Follmann Chemie GmbH

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Jowat SE

- 6.4.10 KLEBCHEMIE M. G. Becker GmbH & Co. KG

- 6.4.11 NANPAO RESINS CHEMICAL GROUP

- 6.4.12 OKONG Corp.

- 6.4.13 Paramelt B.V.

- 6.4.14 Selic Corp Public Company Limited.

- 6.4.15 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms