|

市場調査レポート

商品コード

1693373

英国の接着剤:市場シェア分析、産業動向、統計、成長予測(2025~2030年)United Kingdom Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の接着剤:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 215 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

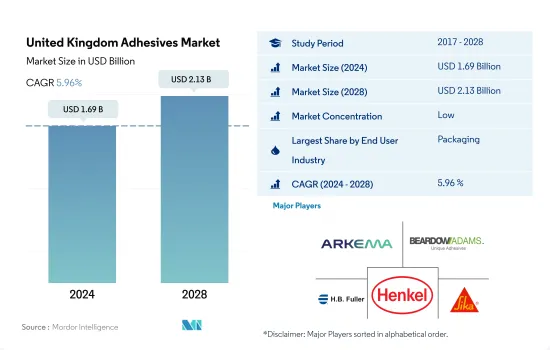

英国の接着剤市場規模は2024年に16億9,000万米ドルと推定・予測され、2028年には21億3,000万米ドルに達し、予測期間中(2024-2028年)にCAGR 5.96%で成長すると予測されています。

ヘルスケアへの投資増加で接着剤需要が拡大

- 接着剤は、様々な産業で使用される様々な基材の接着や接合において重要な役割を果たしています。これらの接着剤は、メーカーが部品や組立品を軽量化し、接合部を迅速、容易、かつ正確に形成するのに役立っています。2020年にはCOVID-19の発生が影響し、2019年と比較して消費量が10.57%減少しました。

- 包装は接着剤の最大の消費者であり、2021年には2020年より6%多い14万4,451トンの接着剤が必要となりました。英国では軟包装が大幅な成長を遂げています。英国では安価で軽量な包装が人気を集めているため、メーカーがさまざまな製品に軟包装を使用するようになっています。したがって、これらの要因が市場の成長をもたらしています。

- ヘルスケアもまた、同国で接着剤が消費される主要産業のひとつです。英国で医療製品を最も多く購入しているのは国民保健サービス(NHS)です。国民保健サービス(NHS)は、医療品とサービスに年間約250億米ドルを費やしています。NHSイングランドは人口の84%にサービスを提供しています。同国によるヘルスケアへの投資の増加は、予測期間中の接着剤需要を促進すると予測されています。

- 英国は欧州第4位の国であり、2021年のシェアは約7.8%です。アクリル系粘着剤とポリウレタン系粘着剤は、建設、自動車、ヘルスケアなど複数のエンドユーザー産業で消費される可能性のある粘着剤です。すべての樹脂系接着剤の中で、アクリル系接着剤は2021年に英国の接着剤市場全体の約29%のシェアを占め、ポリウレタンとEVAがこれに続きます。英国のエポキシ系接着剤市場は、2022~2028年にCAGR 7.08%を記録すると予測されます。

英国の接着剤市場動向

プラスチックのリサイクル性の先進パッケージングと飲食品業界の需要により、プラスチック包装が包装業界をリードする

- COVID-19のパンデミックにより、国全体のロックダウンと製造施設の一時的な操業停止により、サプライチェーンや輸出入貿易の混乱などいくつかの問題が発生しました。その結果、2020年の同国の包装生産量は前年比3%減少し、市場に大きな影響を与えました。

- しかし、パンデミックの結果、消費パターンが変化し、より多くの人々がオンラインで買い物をするようになり、包装の重要性が格段に高まりました。英国はeコマース市場が最も進んでおり、世界第4位の規模を誇っているため、パッケージ生産市場を牽引することになると思われます。インターネットショッピングに関しては、英国は欧州で最も人気のある市場です。英国のeコマース産業は2021年に1,290億英ポンドの収益を上げ、2015年に英国のeコマースが生み出した収益の3倍以上となり、2020年の1,127億英ポンドを約15%上回りました。

- 2021年に生産されたパッケージの約77%を占めています。英国では、生産されたプラスチックの約44.3%が包装用として消費されています。プラスチックのリサイクル性の向上により、プラスチック生産部門は予測期間中にCAGR約3.37%という最速の成長率を記録する可能性が高いです。

2030年までの環境に優しい輸送に加え、電気自動車登録台数の増加が自動車生産を促進する可能性が高い

- 英国の自動車産業は英国経済にとって不可欠な産業であり、その売上高は602億ユーロを超え、英国経済に119億ユーロの付加価値をもたらしています。しかし2020年、英国自動車産業がCOVID-19パンデミックへの対応やBrexitの影響に備えた態勢の立て直しなど、歴史上最大の課題に直面したため、同国の自動車生産台数は2019年同期比で29.5%減少しました。

- 2020年に29.5%減少した英国の自動車生産は、半導体不足が生産に深刻な影響を及ぼしたため、2021年にはさらに4.7%減少しました。2021年9月の新車登録台数は前年同月比で34%減少し、これは将来的に英国のシーラント市場に影響を与えることが予想されます。

- 英国は、2030年までにガソリン車とディーゼル車を段階的に廃止し、より環境に優しい交通機関への移行を促進する計画です。同国はまた、ゼロエミッション車へのアクセスを拡大し、グリーンな経済回復を支援するために、インフラと補助金に18億ポンド以上の投資を計画しており、それによって同国の電気自動車市場の需要を増加させています。

- 英国におけるBEV、PHEV、HEVの総登録台数は、2020年の28万5,199台に対し、2021年には45万2,527台となり、前年比58.7%の成長率を記録しました。2021年の総登録台数(前年比増減率)は、BEVが19万727台(76.3%)、PHEVが11万4,554台(70.6%)、HEVが14万7,246台(34.0%)でした。2021年には、BEV、PHEV、HEVが自動車登録台数の約27.5%を占める。

英国の接着剤産業の概要

英国の接着剤市場は細分化されており、上位5社で39.41%を占めています。この市場の主要企業は以下の通り。 Arkema Group, Beardow Adams, H.B. Fuller Company, Henkel AG & Co. KGaA and Sika AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- 包装

- 木工・建具

- 規制の枠組み

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- ヘルスケア

- 包装

- 木工・建具

- その他のエンドユーザー産業

- テクノロジー

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型接着剤

- 水系

- 樹脂

- アクリル系

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他の樹脂

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- Beardow Adams

- Dow

- Follmann Chemie GmbH

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Sika AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92428

The United Kingdom Adhesives Market size is estimated at 1.69 billion USD in 2024, and is expected to reach 2.13 billion USD by 2028, growing at a CAGR of 5.96% during the forecast period (2024-2028).

Increasing investments in healthcare to augment the demand for adhesives

- Adhesives play an important role in bonding and joining various substrates that are used across industries. These adhesives help manufacturers to lower the weight of their components and assemblies, to form the joints quickly, easily, and accurately. The COVID-19 outbreak impacted the country in 2020, which reduced consumption by 10.57% compared to 2019.

- Packaging is the largest consumer of adhesives, as it required 144,451 tons of adhesives in 2021, which was 6% more than in 2020. Flexible packaging has experienced substantial growth in the United Kingdom. As cheap and lightweight packaging is gaining popularity in the United Kingdom, it is encouraging manufacturers to use flexible packaging for different products. Hence, these factors are responsible for the market's growth.

- Healthcare is also one of the major industries where adhesives are consumed in the country. The largest purchaser of medical products in the United Kingdom is the National Health Service (NHS). The National Health Service (NHS) spends approximately USD 25 billion annually on medical goods and services. NHS England serves 84% of the population. The increasing investments in healthcare by the country are estimated to drive the demand for adhesives during the forecast period.

- The United Kingdom is the 4th-largest European country, holding about 7.8% of shares in 2021. Acrylic and polyurethane adhesives are the potential types of adhesives consumed across several end-user industries, including construction, automotive, and healthcare. Among all resin-based adhesives, acrylic adhesives held about 29% of the overall UK adhesives market share in 2021, followed by polyurethane and EVA. The UK epoxy adhesives market is expected to record a CAGR of 7.08% from 2022-2028.

United Kingdom Adhesives Market Trends

With the advancement in plastic recyclability and demand for food and beverage industry, plastic packaging to lead the packaging industry

- Due to the COVID-19 pandemic, the country-wide lockdowns and temporary shutdown of manufacturing facilities caused several issues, including supply chain and import and export trade disruptions. As a result, the country's packaging production declined by 3% in 2020 compared to the previous year, significantly affecting the market.

- However, as a result of the pandemic, consumption patterns have changed, more people started shopping online, and packaging has become much more significant. The United Kingdom has the most advanced e-commerce market and is the fourth largest in the world, which will drive the packaging production market. When it comes to internet shopping, the United Kingdom is the most popular market in Europe. The UK's e-commerce industry generated GBP 129 billion in revenue in 2021, more than triple the revenue generated by UK e-commerce in 2015, and it was around 15% higher than the GBP 112.7 billion in 2020.

- Packaging production is majorly driven by plastics in the country, accounting for around 77% of the packaging produced in 2021. Around 44.3% of plastics produced were consumed by packaging in the United Kingdom. With the advancement of plastic recyclability, the plastic production segment is likely to register the fastest growth rate of around 3.37% CAGR during the projected period.

In addition to eco-friendly transportation by 2030, electric vehicle registrations growth is likely to propel the automotive production

- The UK automotive industry is a vital part of the UK economy, worth more than EUR 60.2 billion in turnover and adding EUR 11.9 billion value to the UK economy. However, in 2020, the automotive vehicle production in the country reduced by 29.5% compared to the same period in 2019, as the UK automotive sector faced some of the biggest challenges in its history while responding to the COVID-19 pandemic and repositioning for Brexit implications.

- After contracting by 29.5% in 2020, British automotive vehicle production further declined by 4.7% in 2021, as the semiconductor shortage severely affected production. New car registrations decreased 34% Y-o-Y in September 2021, which is excepted to affect the UK sealants market in the future.

- The United Kingdom is planning to phase out gasoline and diesel vehicles to promote the transition to more eco-friendly transportation by 2030. The country also planned an investment of over GBP 1.8 billion in infrastructure and grants to expand access to zero-emission vehicles and support a green economic recovery, thereby increasing the demand for the electric vehicles market in the country.

- The total number of BEV, PHEV, and HEV registrations in the United Kingdom accounted for 452,527 in 2021, registering a growth rate of 58.7% Y-o-Y, compared to 285,199 registrations in 2020. Out of total registrations in 2021 (with percentage Y-o-Y change), 190,727 (76.3%) were BEVs, 114,554 (70.6%) were PHEVs, and 147,246 (34.0%) were HEVs. In 2021, BEV, PHEV, and HEV captured around 27.5% share of total car registrations in the country.

UK Adhesives Industry Overview

The United Kingdom Adhesives Market is fragmented, with the top five companies occupying 39.41%. The major players in this market are Arkema Group, Beardow Adams, H.B. Fuller Company, Henkel AG & Co. KGaA and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 United Kingdom

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Beardow Adams

- 6.4.5 Dow

- 6.4.6 Follmann Chemie GmbH

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms