|

市場調査レポート

商品コード

1693383

インドネシアの接着剤:市場シェア分析、産業動向、成長予測(2025~2030年)Indonesia Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシアの接着剤:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 201 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

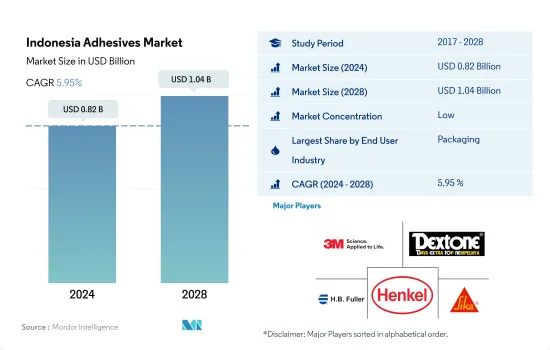

インドネシアの接着剤市場規模は2024年に8億2,000万米ドルと推定され、2028年には10億4,000万米ドルに達すると予測され、予測期間(2024~2028年)のCAGRは5.95%で成長します。

同国で進行中と計画中の多数のインフラプロジェクトが、接着剤需要の成長に重要な役割を果たします。

- インドネシアにおける接着剤の消費量は、COVID-19の影響により2020年には減少傾向を示しました。同年の消費量は2019年に比べ数量ベースで約13%減少しました。同国における封鎖が、同国における接着剤不足の主要因となっていることが大きいです。さらに、生産施設の操業停止とサプライチェーンの混乱により、これらの接着剤の需要は大きく影響を受けています。

- インドネシアの包装産業は、あらゆる産業やビジネスにおいて重要な役割を果たしています。そのため、包装産業の開発は国家産業の開発と切り離すことはできないです。実際、包装は国の工業製品の競合要因の一つとなっています。近年、包装セグメントは前年比6%~7%の成長を遂げており、2021年の実現額は104兆7,280億IDRに達します。現実には、COVID-19の流行が広がり始めても、包装事業は大きな被害を受けなかりました。包装産業は、飲食品(マミン)、医薬品、小売といった主要な支援部門の成長に連動して、年率6%~8%で増加すると予想されています。

- 他方で、産業は現在、国の成長を加速させるために大規模なインフラプロジェクトに投資しています。例えば、インドネシアはジャカルタの地下鉄網を拡大するために400億米ドル以上を投資する計画で、同国の建設産業の強化が期待されています。インドネシアはまた、25の空港や新しい発電所の建設など、今後4,000億米ドル以上の野心的な建設プロジェクトを計画しています。これらすべての変数が接着剤の需要に影響を与えています。

インドネシアの接着剤市場動向

紙と板紙の包装を促進する政府の取り組みが産業規模を拡大する

- 包装は主に、保護、封じ込め、情報、実用性、プロモーションのために使われます。そのため、包装はほとんどの産業にとって不可欠な要素となっています。成長するインドネシア市場は、包装利用を促進し、予測期間中にCAGR 4.33%を記録すると予想されます。2017年の包装利用量は、紙・板紙、プラスチックを含む1億4,346万トンを占めました。COVID-19により、2020年、市場は-5.77%のマイナス成長を記録したが、これはサプライチェーンの混乱、包装材料の不足、商品の輸出入の制限、工場の低能力操業によるものです。

- 2021年には、市場は4.28%のプラス成長を記録し、1億5,341万トンの包装材料が様々な用途に使用されます。商品の出荷には特殊な包装が必要であるため、ここ数年、包装産業に大きな追い風となっているeコマースセクタが増加しており、包装産業は今後も成長を続けると予想されます。

- インドネシアは中国に次いで海洋におけるプラスチック廃棄物の排出量が第2位であるため、インドネシア政府はプラスチック使用に対する措置を講じています。インドネシア政府が課した拡大生産者責任(EPR)規制は、生産者や小売業者に対し、リサイクル可能な材料の比率が高くなるよう製品包装を再設計することを義務付けるものです。これにより、メーカーは包装の基材として紙や板紙を使用するようになり、包装プロセスで使用される接着剤の量が増えることになります。

- 競争の激しい今日の消費財市場では、競合他社に差をつけ、市場でのブランド価値を維持するために、企業が魅力的な包装を使用することは避けられなくなっています。

自動車部品コンポーネントの輸出額の大幅な伸びが産業の成長を促進する

- インドネシアの自動車産業は、国の経済発展に大きく貢献する有望なセクタであり続けています。インドネシア共和国セクタ大臣Agus Gumiwang Kartasasmitaによると、インドネシアの自動車産業は2021年に17.82%の2桁成長率で驚異的な成長を示しました。2019年、インドネシアの自動車生産台数は約128万6,848台であったが、2020年には69万176台に激減し、COVID-19の流行により約46%減少しました。このため、2019~2021年にかけての自動車生産台数の変動は約-13%であったのに対し、2020~2021年にかけての変動は約63%でした。

- インドネシアの自動車部門の貿易は、2019~2021年まですべての年で黒字を示しました。2020年には世界のパンデミックにより輸出入ともに減少し、経済活動に制限と混乱が生じたため、世界のサプライチェーンが阻害され、総生産に打撃を与えました。しかし、2021年の堅調な生産に伴い、輸出入額ともに大幅に増加し、貿易収支は19億3,000万米ドルとなりました。2021年の商業活動のレベルは過去10年間で最高であったが、貿易収支の黒字は、それぞれ20億米ドル、19億5,000万米ドルの黒字であった2019年、2020年と比較して最低でした。

- 世界的に見ると、EVの開発はインドネシアの交通セクタの施策の根本的な転換を告げるものでした。同国のニッケル埋蔵量を考えると、インドネシアは世界のEVサプライチェーンの主要企業になるのに十分な位置にあります。この地域のEVの未来の一翼を担うためには、インドネシアは技術、人材、再生可能エネルギー、インフラに投資する必要があります。

インドネシアの接着剤産業概要

インドネシアの接着剤市場は細分化されており、上位5社で15.91%を占めています。同市場の主要企業は以下の通りです。3M、DEXTONE INDONESIA、H.B. Fuller Company、Henkel AG & Co. KGaA、Sika AGなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- フットウェア皮革

- 包装

- 木工・建具

- 規制の枠組み

- インドネシア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- フットウェアと皮革

- 医療

- 包装

- 木工・建具

- その他

- 技術

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型接着剤

- 水性

- 樹脂

- アクリル系

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- ALTECO co., ltd.

- DEXTONE INDONESIA

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI S.p.A.

- Pidilite Industries Ltd.

- PT. Pamolite Adhesive Industry

- Sika AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92438

The Indonesia Adhesives Market size is estimated at 0.82 billion USD in 2024, and is expected to reach 1.04 billion USD by 2028, growing at a CAGR of 5.95% during the forecast period (2024-2028).

The numerous ongoing and planned infrastructure projects in the country to have a key role in the growth of adhesive demand

- The consumption of adhesives in Indonesia has shown a downward trend in 2020 due to the impact of COVID-19. The consumption was reduced by about 13% in terms of volume in the same year compared to 2019. The lockdown in the country has largely become the major reason for the shortage of adhesives in the country. Moreover, due to the shutdown of production facilities and supply chain disruption, the demand for these adhesives is largely being impacted.

- The Indonesian packaging industry plays an important role in all industries and businesses. Therefore, the development of the packaging industry cannot be separated from the development of the national industry. In fact, packaging has become one of the determining factors for the competitiveness of national industrial products. In recent years, the packaging sector has grown by 6%-7% year-on-year, with a realized value of IDR 104,728 billion in 2021. In reality, as the COVID-19 epidemic began to spread, the packing business did not suffer considerably. The packaging industry is expected to increase at a 6%-8% annual rate, in conjunction with the growth of the major supporting sectors, such as food and beverage (Mamin), pharmaceutical, and retail.

- On the other side, the industry is now investing in massive infrastructure projects to accelerate the country's growth. For example, Indonesia is planning to invest over USD 40 billion to expand Jakarta's metro network, which is expected to strengthen the country's construction industry. Indonesia is also planning ambitious construction projects worth more than USD 400 billion in the future years, including the construction of 25 airports and new power plants. All of these variables influence the demand for adhesives.

Indonesia Adhesives Market Trends

The government initiatives to promote paper and paperboard packaging will escalate the industry size

- The packaging is mainly used for protection, containment, information, utility of use, and promotion. This makes packaging an integral part of most industries. The growing Indonesian market is expected to boost packaging usage and register a CAGR of 4.33% during the forecast period. In 2017, packaging usage accounted for 143.46 million tons of packaging, including paper and paperboard and plastic. Due to COVID-19, in 2020, the market registered a negative growth of -5.77%, and this was due to disruption in the supply chain, shortage of packaging material, restrictions on the import and export of goods, and factories operating at low capacity.

- In 2021, the market registered a positive growth of 4.28%, with 153.41 million tons of packaging material used for various purposes. It is expected that the packaging industry will keep growing as there has been a rise in the e-commerce sector which has given a significant boost to the packaging industry in the past few years as special packaging is required for shipping goods.

- The government of Indonesia has taken steps toward the use of plastic, as Indonesia is the second-largest contributor of plastic waste in the ocean after China. The extended producer responsibility (EPR) regulation imposed by the Indonesian government will oblige producers and retailers to redesign their product packaging to have a higher proportion of recyclable material. This will encourage manufacturers to use paper and paperboard as the base material for the packaging, which will increase the volume of adhesives used in the packaging process.

- In today's competitive market of consumer products, it has become inevitable for companies to use attractive packaging to stand out from their competitors and maintain their brand value in the market.

Considerable growth of export values for automotive parts & components will proliferate the industry growth

- The automotive industry in Indonesia remains a promising sector that contributes significantly to the country's economic progress. According to Agus Gumiwang Kartasasmita, Minister of Sector Republic of Indonesia, the automobile industry in Indonesia witnessed tremendous growth in 2021, with a double-digit growth rate of 17.82%. In 2019, the country produced about 12,86,848 units of vehicles which drastically reduced to 6,90,176 units in 2020, accounting for a decline of about 46% owing to the COVID-19 pandemic. Due to this reason, the variation in automotive production between 2019 and 2021 resulted in about -13%, whereas between 2020 and 2021, the variation was about 63%.

- The trade in the automotive sector in Indonesia showed a surplus in all years from 2019 to 2021. Both exports and imports fell in 2020 as a result of the global pandemic, which generated limitations and disruptions in economic activities, so impeding the global supply chain and hurting total production. However, in line with the robust output in 2021, both export and import values increased significantly, with a trade balance of USD 1.93 billion. Although 2021 had the highest level of commercial activity in the prior ten years, the trade balance surplus was the lowest in comparison to 2019 and 2020, which had balance values of USD 2 billion and USD 1.95 billion, respectively.

- Globally, the development of EVs signaled a fundamental shift in the Indonesian transportation sector's policies. Given the country's nickel reserves, Indonesia is well-placed to become a major player in the global EV supply chain. To be a part of the region's EV future, Indonesia needs to invest in technology, talent resources, renewable energy, and infrastructure.

Indonesia Adhesives Industry Overview

The Indonesia Adhesives Market is fragmented, with the top five companies occupying 15.91%. The major players in this market are 3M, DEXTONE INDONESIA, H.B. Fuller Company, Henkel AG & Co. KGaA and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Indonesia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 ALTECO co., ltd.

- 6.4.3 DEXTONE INDONESIA

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Huntsman International LLC

- 6.4.7 MAPEI S.p.A.

- 6.4.8 Pidilite Industries Ltd.

- 6.4.9 PT. Pamolite Adhesive Industry

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms