|

市場調査レポート

商品コード

1692129

北米の保険テレマティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Insurance Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の保険テレマティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 113 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

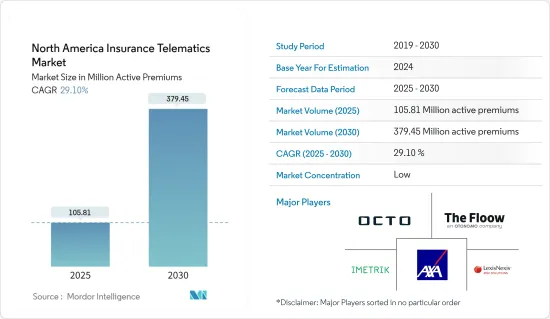

北米の保険テレマティクス市場規模は2025年に1億581万アクティブ保険料と推計され、2030年には3億7,945万アクティブ保険料に達すると予測され、予測期間(2025年~2030年)のCAGRは29.1%です。

保険業界と自動車業界におけるテレマティクス機器への需要の高まりが、市場の成長を後押ししています。多くの自動車会社は、競争力を高めるために先進的なテレマティクス・システムに投資しています。アプリケーションに特化したテレマティクスやコンピュータ画像から、車両管理者は車両の状態に関する豊富な情報にアクセスできます。

主なハイライト

- 渋滞と道路交通量の増加により、人々の安全が最優先事項となっています。先進的な車両機能の向上は、車両保険テレマティクスの需要拡大を後押しする重要な要因です。全米安全評議会によると、米国では2021年に約4万7,000人の交通事故死者が発生しました。この死者数は2022年にはわずかに減少し、約46,300人となりました。米国では自動車事故が死因となることが多いです。

- また、公式発表によると、2023年、米国で警察が報告した自動車事故は6,102,936件でした。そのうち39,508件が死亡事故でした。このような交通事故の増加は、この地域で保険テレマティクスの需要をさらに生み出す可能性があります。

- 様々な政府が事故や自動車衝突を避けるために交通安全への取り組みを行っており、それがこの地域での保険テレマティクスの需要を生み出す可能性があります。さらに、カナダの第4次交通安全国家計画である交通安全戦略(RSS)2025は、2016年初頭に運輸・道路安全担当閣僚会議によって開始されました。その目標は、設定された基準期間と複数年の平均を比較しながら、5年間を通じて死亡事故と重傷事故の減少動向を達成することに変わりはないです。

- しかし、保険テレマティクスの認知度の低さや、プライバシーやセキュリティに関する懸念が、やや市場の妨げとなっています。その一方で、自動車企業における技術革新の進展と新興経済圏における未開拓の可能性は、今後数年間に新たな機会をもたらします。

- COVID-19パンデミックは保険テレマティクス業界に好影響を与えました。これは、車両が封鎖されている間に利用が制限された場合に、保険料を安くしたいという消費者のニーズにテレマティクスが直接対応したためです。

- さらに、パンデミックは保険会社の要求を従来の保険数理モデルや保険引受モデルからPAYD(Pay as You Drive)モデルへと変化させました。さらに、保険契約の締結や保険金請求プロセスにおけるデジタルツールの利用が消費者に受け入れられ、保険会社が保険料をより正確に設計する必要性が高まったことも、市場の成長に大きく寄与しています。

北米の保険テレマティクス市場の動向

地域全体の自動車産業における技術革新の増加が成長を牽引

- 自動車業界における技術革新は保険テレマティクスの成長を牽引する重要な要因であり、保険会社がテクノロジーを活用してよりパーソナライズされたデータ主導型の保険商品を提供する機会を生み出しています。組み込み型テレマティクス・システム、車載センサー、車載通信ネットワークなど、コネクテッド・カー技術の普及により、保険会社は車両性能、ドライバーの行動、環境状況に関するリアルタイムのデータを入手できるようになりました。これらのデータストリームは、より正確な保険契約のリスク評価と価格設定モデルを可能にします。

- さらに、自律走行車や半自律走行車の技術開発は、自動車産業を再構築し、保険テレマティクスに新たな機会をもたらしています。保険会社はテレマティクス・データを活用して、ADASや自律走行機能が運転行動、安全性、リスク・エクスポージャーに与える影響を評価することができます。コネクテッドカーや自律走行車の台頭により、これらの新しいシステムは運転行動に関連するデータを効果的にモニターし、報告する必要があるため、テレマティクスの重要性はさらに高まっています。テレマティクス技術は現代の自動車にとって極めて重要な要素となっており、保険会社は単なる推測に頼るのではなく、ドライバーのリアルタイムの行動を評価することで保険料を正確に決定することができます。

- 米国は、自動車OEMの存在感が大きいこと、一般の自動車購入者の技術意識が高いこと、自動車におけるインフォテインメントとテレマティクスの選好、4G/5Gの普及、同国における電気自動車、コネクテッドカー、自律走行車の販売増加などにより、コネクテッドカーの重要な市場になると予想されます。

- 米国道路安全保険協会によると、米国の道路を走る自動運転車は2025年までに約350万台、2030年までに450万台になると予想されています。しかし、同研究所は、これらの自動車は完全な自律走行ではなく、一定の条件下で自律走行するだろうと注意を促しています。保険会社と自律走行車メーカーとの共生関係を認識し、保険会社は積極的に協力関係を結んでいます。メーカーと密接に協力することで、保険会社は自律走行車に関連する技術、安全機能、潜在的なリスクに関する知見を得ることができます。

- このような協力的なアプローチは、保険会社が自動運転車の進化する状況に沿った保険を作るのに役立っています。例えば、トヨタ・インシュアランス・マネジメント・ソリューションズUSAの関連会社であるコネクテッド・アナリティック・サービスLLC(CAS)は、北米トヨタ自動車との提携を拡大し、トヨタ車の所有者の所有体験を向上させる新商品を追加しました。CASは、トヨタの顧客が運転データを利用して保険料の節約を図りたい場合に、トヨタが独占的に提供するデータアグリゲーションサービスであり、保険会社にテレマティクスと車両データを提供します。同市場の主要企業は、コネクテッドカー需要の増加に対応するため、デジタルモビリティ分野でのプレゼンスを拡大しつつあります。

米国が主要市場シェアを占める

- 開発・技術コストの低下、消費者行動の変化、政府の厳しい規制が、米国で調査された市場の成長を後押ししています。米国では、消費者は利用ベースの保険(UBI)スナップショット・プログラムを好みます。他の地域では、自動車保険のテレマティクス保険が好まれています。

- 保険テレマティクスの導入は、保険会社と消費者にとっていくつかの利点があり、市場成長を促進すると予想されます。消費者にとっては、安全運転が促進され、その結果、事故の深刻度と頻度が軽減されます。予測期間中、保険会社の保険金請求処理費用は少なくとも半減し、市場の成長に寄与すると思われます。

- 米国のさまざまな消費者が保険会社を乗り換えているのは、運転する機会が減ったにもかかわらず保険料が上昇したためです。パンデミック(世界的大流行)時の封鎖措置により、消費者は運転する機会が減り、最終的には自動車の使用状況を分析して走行距離に応じた個別保険を提供する保険が求められるようになりました。

- ロイズ・オブ・ロンドンによると、米国の自動車保険セクターの2015年の市場規模は約2,247億米ドルに達すると予想されています。2025年には約3,585億1,000万米ドルに成長すると予測されています。

- BEAによれば、2023年5月、米国ではライトトラックを含む107万台の自動車が販売され、106万台の販売に寄与し、依然として米国の自動車市場の最も重要なセグメントでした。

- 米国は、自動車OEMの大きな存在感、一般的な自動車購入者の技術意識の高さ、自動車のインフォテインメントとテレマティクスの嗜好、4G/5Gの広範な採用、電気自動車、コネクテッドカー、自律走行車の販売増加により、同国におけるコネクテッドカーの重要な市場になると予想されます。

北米の保険テレマティクス産業の概要

北米の保険テレマティクス市場は断片化されており、Octo Telematics SpA、IMERTIK Global Inc.、AXA SA、The Floow Limited、LexisNexis Risks Solutions(RELX Group)などの主要企業が参入しています。市場参入企業は、製品ラインナップを充実させ、持続的な競争力を確保するために、パートナーシップや買収を採用しています。

- 2023年10月、OCTOテレマティクスは、自動車所有に代わるスマートな選択肢を提供するFlexcarとの提携を発表。

- 2023年10月、PowerFleet Inc.は、南アフリカを拠点とする車両管理技術会社MiX Telematics Ltd.と合併し、合計約170万人の加入者を有する単一会社を設立する予定です。買収は2024年第1四半期に完了する予定で、統合後のブランド名はPowerFleetとなります。上場はナスダック、本社はニュージャージー州ウッドクリフレイクとなります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 保険会社による利用ベース保険の採用増加

- 地域全体の自動車産業における技術革新の増加が成長を牽引

- 市場の課題

- データ品質と互換性の問題

第6章 利用ベースの保険テレマティクス-収益モデル

- PAYD

- PHYD

- How-you-driveの管理

第7章 各種テレマティクス・ハードウェアベースの保険ソリューションの比較分析

- ポータブル

- 組み込み型

- スマートフォンベース

第8章 市場セグメンテーション

- 国別

- 米国

- カナダ

第9章 競合情勢

- 企業プロファイル

- Octo Telematics SpA

- IMERTIK Global Inc.

- AXA SA

- The Floow Limited

- LexisNexis Risks Solutions(RELX Group)

- PowerFleet Inc.

- Cambridge Mobile Telematics

- State Farm Mutual Automobile Insurance Company

- GEICO(Berkshire Hathaway Inc.)

- Nationwide Mutual Insurance Company

第10章 投資分析

第11章 今後の動向

The North America Insurance Telematics Market size is estimated at 105.81 million active premiums in 2025, and is expected to reach 379.45 million active premiums by 2030, at a CAGR of 29.1% during the forecast period (2025-2030).

The growing demand for telematic devices among the insurance and automotive sectors propels the market's growth. Many automotive companies invest in advanced telematics systems to gain a competitive edge. From application-specific telematics and computer imaging, fleet managers can access a wealth of information about the condition of their vehicles.

Key Highlights

- Rising congestion and road traffic have made people's safety a top priority. Improving advanced vehicle features is a significant factor aiding the growth of the demand for vehicle insurance telematics. According to the National Safety Council, some 47,000 road traffic fatalities occurred in the United States in 2021, which was the most significant number of deaths recorded in the country since 2012. This fatality volume was slightly dipped in 2022, down to nearly 46,300. Motor vehicle crashes are a frequent cause of death in the United States.

- In addition, according to the official source, in 2023, there were 6,102,936 police-reported vehicle accidents in the United States. Of those, 39,508 were fatal. Such increases in road accidents may further create demand for insurance telematics in the region.

- Various governments are taking initiatives in road safety to avoid accidents or car crashes, which may create demand for insurance telematics in the region. Furthermore, Canada's fourth national road safety plan, the Road Safety Strategy (RSS) 2025, was launched by the Council of Ministers Responsible for Transportation and Highway Safety in early 2016. The goal remains to achieve downward trends in fatalities and severe injuries throughout a five-year duration, comparing multi-year rolling averages with the established baseline period.

- However, a lack of awareness of insurance telematics and privacy and security concerns somewhat hinder the market. On the other hand, increasing innovation in the automotive enterprise and untapped potential in emerging economies present new opportunities in the upcoming years.

- The COVID-19 pandemic had a positive impact on the insurance telematics industry. This is attributed to telematics directly addressing consumer needs to pay lower premiums when the vehicles had limited utilization during the lockdown.

- In addition, the pandemic changed insurers' demands from traditional actuarial and underwriting models to pay-as-you-drive (PAYD) models. In addition, increased acceptance of digital tools in the policy binding and claims process among consumers, combined with a need for insurers to design premium policies more precisely, are significant factors that notably contribute to the market's growth.

North America Insurance Telematics Market Trends

Increase in Innovation in the Automotive Industry Across the Region to Witness Growth

- Innovation in the automotive sector is a key driver of the growth of insurance telematics, creating opportunities for insurers to leverage technology to offer more personalized and data-driven insurance products. The proliferation of connected car technologies, including embedded telematics systems, onboard sensors, and in-vehicle communication networks, provide insurers with real-time data on vehicle performance, driver behavior, and environmental conditions. These data streams enable more accurate insurance policy risk assessments and pricing models.

- Moreover, developing autonomous and semi-autonomous vehicle technologies is reshaping the automotive industry and presenting new opportunities for insurance telematics. Insurers can leverage telematics data to assess the impact of ADAS and autonomous features on driving behavior, safety, and risk exposure. With the rise of connected and autonomous vehicles, telematics is even more important as these new systems need to monitor effectively and report data related to driving behavior. Telematics technology has become a crucial element in modern vehicles, enabling insurers to precisely determine premiums by assessing a driver's real-time behavior rather than relying on mere speculation.

- The United States is anticipated to be the significant market for connected cars due to the significant presence of automotive OEMs, higher technological awareness among the general car buyers, preference for infotainment and telematics in vehicles, widespread adoption of 4G/5G, and increasing sales of electric, connected and autonomous cars in the country.

- According to the Insurance Institute for Highway Safety, it is anticipated that there will be around 3.5 million self-driving vehicles on US roads by 2025 and 4.5 million by 2030. However, the institute cautioned that these vehicles would not be fully autonomous but would operate autonomously under certain conditions. Recognizing the symbiotic relationship between insurers and autonomous vehicle manufacturers, insurers are actively engaging in collaborations. By working closely with manufacturers, insurers gain insights into the technology, safety features, and potential risks associated with autonomous vehicles.

- This collaborative approach helps insurers craft policies that align with the evolving landscape of self-driving cars. For instance, Connected Analytic Services, LLC (CAS), an affiliate of Toyota Insurance Management Solutions USA, expanded its partnership with Toyota Motor North America to add new product offerings to enhance the ownership experience for owners of enrolled Toyota vehicles. For Toyota customers who wish to use their driving data to obtain potential insurance savings, CAS is Toyota's exclusive data aggregation service, providing telematics and vehicle build data to insurance companies. Major players in the market are expanding their presence in digital mobility to cater to the increased demand for connected cars.

United States to Hold Major Market Share

- Decreasing the cost of development and technology, altering consumer behavior, and stringent government regulations drive the growth of the market studied in the United States. In the United States, consumers prefer usage-based insurance (UBI) snapshot programs. In other regions, motor insurance telematics policies are preferred.

- Introducing insurance telematics has several advantages for insurers and consumers, which are expected to fuel market growth. For consumers, it will promote safe driving, resulting in the mitigation of accident severity and frequency. Over the forecast period, the insurers' claim-handling expenses will likely decrease by at least half, contributing to the market's growth.

- Various US consumers are switching insurers because their premiums have increased despite driving less. Measures imposed during the lockdown during the pandemic led consumers to drive less and ultimately demanded policies that analyzed auto usage to provide personalized policies based on mileage.

- According to Lloyd's of London, the value of the motor vehicle insurance sector in the United States is expected to amount to approximately USD 224.7 billion in 2015. It was projected to grow to about USD 358.51 billion by 2025.

- According to BEA, in May 2023, 1.07 million vehicles were sold in the United States, including light trucks, which remained the most significant United States auto market segment, contributing to sales of 1.06 million units.

- The United States is anticipated to be the significant market for connected cars in the country due to the substantial presence of automotive OEMs, high levels of technology awareness amongst the general car buyers, preference for infotainment and telematics in vehicles, widespread adoption of 4G/5G and increasing sales of electric, connected and autonomous cars in the country.

North America Insurance Telematics Industry Overview

The North American insurance telematics market is fragmented, with major players like Octo Telematics SpA, IMERTIK Global Inc., AXA SA, The Floow Limited, and LexisNexis Risks Solutions (RELX Group). Market participants employ partnerships and acquisitions to improve their product offerings and secure a lasting competitive edge.

- In October 2023 - OCTO Telematics announced a partnership with Flexcar, the smart alternative to car ownership, focused on adding OCTO's connected vehicle capabilities to Flexcar's fleet across the United States.

- In October 2023 - PowerFleet Inc. intends to merge with MiX Telematics Ltd, a fleet management tech firm based in South Africa, creating a single company with a combined subscriber base of some 1.7 million users. The deal is expected to close in the first quarter of 2024, and the combined business will be branded as PowerFleet. Its primary listing will be on Nasdaq, and its headquarters will be in Woodcliff Lake, New Jersey.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Usage-based Insurance by Insurance Companies

- 5.1.2 Increase in Innovation in the Automotive Industry Across the Region to Witness the Growth

- 5.2 Market Challenge

- 5.2.1 Data Quality and Compatibility Issues

6 USAGE BASED INSURANCE TELEMATICS - REVENUE MODELS

- 6.1 Pay-as-you-drive

- 6.2 Pay-how-you-drive

- 6.3 Manage-how-you-drive

7 COMPARATIVE ANALYSIS OF VARIOUS TYPES OF TELEMATICS HARDWARE-BASED INSURANCE SOLUTIONS

- 7.1 Portable

- 7.2 Embedded

- 7.3 Smartphone Based

8 MARKET SEGMENTATION

- 8.1 By Country

- 8.1.1 United States

- 8.1.2 Canada

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Octo Telematics SpA

- 9.1.2 IMERTIK Global Inc.

- 9.1.3 AXA SA

- 9.1.4 The Floow Limited

- 9.1.5 LexisNexis Risks Solutions (RELX Group)

- 9.1.6 PowerFleet Inc.

- 9.1.7 Cambridge Mobile Telematics

- 9.1.8 State Farm Mutual Automobile Insurance Company

- 9.1.9 GEICO (Berkshire Hathaway Inc.)

- 9.1.10 Nationwide Mutual Insurance Company