保険テレマティクスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Insurance Telematics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766250

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

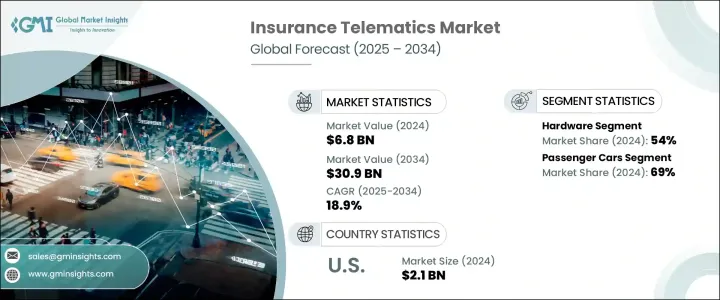

世界の保険テレマティクス市場は2024年に68億米ドルと評価され、CAGR 18.9%で成長し、2034年には309億米ドルに達すると推定されています。

この力強い勢いは、コネクテッドカーに対する需要の高まりと、データ主導型保険モデルの急速な普及によるところが大きいです。自動車とデジタル技術の統合が進むにつれ、テレマティクスは保険サービスの近代化を実現する重要な手段として浮上してきました。保険会社は、従来の画一的な引受モデルから脱却し、運転習慣、車両の使用状況、個人のリスクプロファイルを評価するためにリアルタイムデータを採用するようになっています。この変革は、運転中の契約者の実際の行動をより反映したダイナミックな価格設定モデルを提供することで、保険業界を再構築しています。

リアルタイムのテレマティクスの統合により、保険会社は、ブレーキパターン、加速度、走行距離、ルート状況など、ドライバーのパフォーマンス指標に基づいて保険料を調整することができます。このような洞察は、高度な車両センサー、GPS、加速度計、車載診断システムによって可能となり、これらすべてが連動して常にコンテキストに沿ったデータを生成します。この進化は、価格設定の精度を高めるだけでなく、クレーム処理、リスク検出、顧客維持においても重要な役割を果たしています。このエコシステムが拡大するにつれ、データは次世代保険戦略のバックボーンとなり、安全運転に報い、不正行為を減らし、保険会社と顧客の結びつきを強化する、行動ベースの保険モデルを後押しします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 68億米ドル |

| 予測金額 | 309億米ドル |

| CAGR | 18.9% |

保険会社は現在、クラウド統合とシームレスなモバイルアクセスをサポートする、拡張性のあるデータ中心のプラットフォームを優先しています。この動きは、組み込みハードウェアやスマートフォンベースのソリューションを通じてテレマティクスシステムに接続する車両が増えるにつれて不可欠となっています。これを受けて、保険会社はリアルタイムのデータ分析、パーソナライズされたレコメンデーション、柔軟な保険契約管理をサポートするテクノロジーの採用を加速させています。こうしたデジタル機能により、保険会社は業務効率を維持しながら、現代のドライバーの進化する期待に応える機動的な保険商品を発売することができます。その結果、テレマティクスはもはや単なるオプション機能ではなく、競争の激しい自動車保険業界において戦略的必須事項となりつつあります。

保険テレマティクス市場は、ハードウェア、ソフトウェア、サービスに分類されます。2024年には、ハードウェアが業界全体の約54%を占め、予測期間を通じてCAGR19%以上で拡大すると予測されています。ブラックボックス、GPSトラッカー、OBD-IIドングル、テレマティクスコントロールユニットなどのハードウェアデバイスは、車両活動に関するデータの収集と送信において重要な役割を果たします。これらのシステムは高精度と耐久性を目指して設計されており、ドライバーの行動や使用パターンに関する信頼性の高い洞察を保険会社に提供しています。こうしたシステムの採用が拡大しているのは、利用ベースや従量制の保険モデルの基盤として、リアルタイムのデータ収集に向かう業界全体の動向を反映しています。

車両タイプ別に分析すると、市場は乗用車と商用車に分けられます。2024年には、乗用車が世界売上高の約69%を占め、最大のシェアを占めており、このセグメントは2025年から2034年にかけてCAGR 20%以上で成長すると予測されています。この優位性は、個々のドライバーの間で個別化された保険への嗜好が高まっていることと、新車にテレマティクスシステムが工場で統合されつつあることが背景にあります。先進的な追跡・分析機能が乗用車に標準装備されるようになり、保険会社はこのデータを活用して、より正確な価格設定と事前のリスク管理を行うようになっています。

クラウドベースのソリューションは、その柔軟性、拡張性、大量のデータをリアルタイムで処理する能力により、市場をリードすると予測されています。これらのプラットフォームは、保険会社がストレージやコンピューティングリソースを動的に調整することを可能にし、テレマティクスの普及とデータ負荷の増大に伴って必要となります。こうしたプラットフォームの人気は、特に技術先進地域において、接続インフラへの投資が増加していることも後押ししています。

地域別では、米国が2024年の北米における保険テレマティクス市場の約81%を占め、約21億米ドルの売上を生み出しました。同国は、その広範なデジタルインフラ、高い自動車所有率、パーソナライズされた保険体験に対する需要の高まりにより、テレマティクス統合における革新の最前線にあり続けています。バリューチェーン全体の市場参入企業は、リアルタイムのドライバー監視、行動分析、自動クレーム処理をサポートする、安全でスケーラブルかつ顧客に優しいソリューションの構築に取り組んでいます。規制の枠組みがデータ主導の保険モデルをますますサポートするようになるにつれ、米国市場は世界情勢におけるリーダーシップを維持すると予想されます。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 利用度ベースの保険(UBI)の導入増加

- 車両の接続性の向上

- 運転者行動モニタリングの需要の高まり

- スマートフォンベースのテレマティクスの成長

- 業界の潜在的リスク&課題

- データのプライバシーとセキュリティに関する懸念

- 設置および保守コストが高め

- 市場機会

- EVおよび自動運転車エコシステムとの統合

- AIを活用したリスクスコアリングプラットフォームの成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- コスト内訳分析

- ソフトウェア開発およびライセンシング費用

- 導入と統合のコスト

- 保守・サポート費用

- サイバーセキュリティとコンプライアンスのコスト

- トレーニングと変更管理コスト

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

- 消費者行動と採用動向

- ユーザーエクスペリエンスとインターフェースの動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- オンボード診断(OBD)デバイス

- ブラックボックス

- スマートフォン

- OEM組み込みデバイス

- ソフトウェア

- テレマティクスデータ分析プラットフォーム

- 行動スコアリングエンジン

- モバイルテレマティクスアプリケーション

- ポリシー管理およびリスク評価ツール

- ダッシュボードと視覚化ツール

- サービス

- プロ

- 管理

第6章 市場推計・予測:車種別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 軽作業

- 中型

- ヘビーデューティー

第7章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

第8章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第9章 市場推計・予測:保険別, 2021年~2034年

- 主要動向

- 使用ベースの保険(UBI)

- 走行距離に応じた料金(PAYD)

- 運転特性に応じた料金(PHYD)

- 距離ベースの保険

- 行動ベースの保険

- オンデマンド保険

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Allstate Insurance

- AXA Group

- Cambridge Mobile Telematics

- DriveQuant

- GEICO

- Imetrik Global

- LexisNexis Risk Solutions

- Liberty Mutual Insurance

- Metromile

- Nationwide Mutual Insurance

- Octo Telematics

- Progressive Corporation

- Sierra Wireless

- State Farm

- The Floow

- TrueMotion

- UnipolTech SpA

- Verizon Connect

- Vodafone Automotive

- Zubie

目次

The Global Insurance Telematics Market was valued at USD 6.8 billion in 2024 and is estimated to grow at a CAGR of 18.9% to reach USD 30.9 billion by 2034. This strong momentum is largely attributed to the growing demand for connected vehicles and the rapid uptake of data-driven insurance models. As vehicles become more integrated with digital technologies, telematics has emerged as a key enabler in modernizing insurance offerings. Insurers are shifting away from traditional, one-size-fits-all underwriting models and embracing real-time data to evaluate driving habits, vehicle usage, and individual risk profiles. This transformation is reshaping the insurance landscape by offering dynamic pricing models that better reflect a policyholder's actual behavior behind the wheel.

The integration of real-time telematics allows insurers to tailor premiums based on a driver's performance metrics, such as braking patterns, acceleration, mileage, and route conditions. These insights are made possible by advanced vehicle sensors, GPS, accelerometers, and onboard diagnostics systems, all working together to generate a constant flow of contextual data. This evolution not only enhances pricing accuracy but also plays a critical role in claims processing, risk detection, and customer retention. As this ecosystem expands, data becomes the backbone of next-generation insurance strategies-powering behavior-based policy models that reward safe driving, reduce fraud, and strengthen the link between insurer and customer.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.8 Billion |

| Forecast Value | $30.9 Billion |

| CAGR | 18.9% |

Insurance providers are now prioritizing scalable, data-centric platforms that support cloud integration and seamless mobile access. This move is essential as more vehicles connect to telematics systems through embedded hardware or smartphone-based solutions. In response, insurers are increasingly adopting technologies that support real-time data analysis, personalized recommendations, and flexible policy management. These digital capabilities allow companies to launch agile insurance products that meet the evolving expectations of modern drivers while maintaining operational efficiency. As a result, telematics is no longer just an optional feature-it is becoming a strategic imperative in the competitive auto insurance space.

In terms of components, the insurance telematics market is categorized into hardware, software, and services. In 2024, hardware dominated the industry, accounting for approximately 54% of the total market, and is forecast to expand at a CAGR exceeding 19% throughout the forecast period. Hardware devices such as black boxes, GPS trackers, OBD-II dongles, and telematics control units play a crucial role in collecting and transmitting data about vehicle activity. These systems are engineered for high precision and durability, providing insurers with reliable insights into driver behavior and usage patterns. Their growing adoption reflects a broader industry trend toward real-time data collection as the foundation for usage-based and pay-as-you-drive insurance models.

When analyzed by vehicle type, the market is divided into passenger cars and commercial vehicles. In 2024, passenger cars held the largest share, contributing nearly 69% of the global revenue, and this segment is anticipated to grow at a CAGR of over 20% from 2025 to 2034. This dominance is driven by the growing preference for personalized insurance coverage among individual drivers and the increasing factory integration of telematics systems in new vehicles. With advanced tracking and analytics capabilities becoming standard in passenger cars, insurers are leveraging this data to offer more accurate pricing and proactive risk management.

Deployment mode is another key segment, with cloud-based solutions projected to lead the market due to their flexibility, scalability, and ability to handle large volumes of data in real time. These platforms allow insurers to adjust storage and computing resources dynamically, a necessity as telematics adoption spreads and the data load grows. Their popularity is further supported by rising investments in connected infrastructure, especially in technologically advanced regions.

Regionally, the United States accounted for around 81% of the insurance telematics market in North America in 2024, generating approximately USD 2.1 billion in revenue. The country remains at the forefront of innovation in telematics integration due to its extensive digital infrastructure, high vehicle ownership, and growing demand for personalized insurance experiences. Market participants across the value chain are working to build secure, scalable, and customer-friendly solutions that support real-time driver monitoring, behavior analysis, and automated claims handling. As regulatory frameworks increasingly support data-driven insurance models, the U.S. market is expected to maintain its leadership in the global landscape.

The overall trajectory of the insurance telematics market points to a future where connected mobility and digital insurance are deeply intertwined. As insurers continue to refine their data analytics capabilities and integrate emerging technologies like artificial intelligence and edge computing, the ability to deliver precise, real-time, and personalized insurance products will become standard practice. Telematics is not just transforming pricing models-it is redefining how insurers interact with policyholders in a connected, data-first world.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Deployment Mode

- 2.2.5 Enterprise Size

- 2.2.6 Insurance

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of Usage-Based Insurance (UBI)

- 3.2.1.2 Increased vehicle connectivity

- 3.2.1.3 Growing demand for driver behavior monitoring

- 3.2.1.4 Smartphone-based telematics growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy & security concerns

- 3.2.2.2 High installation and maintenance costs

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with EV and autonomous vehicle ecosystems

- 3.2.3.2 Growth in AI-powered risk scoring platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

- 3.13 Consumer behaviour & adoption trends

- 3.14 User experience & interface trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 On-board Diagnostic (OBD) devices

- 5.2.2 Black box

- 5.2.3 Smartphones

- 5.2.4 OEM embedded devices

- 5.3 Software

- 5.3.1 Telematics data analytics platforms

- 5.3.2 Behavior scoring engines

- 5.3.3 Mobile telematics applications

- 5.3.4 Policy management & risk assessment tools

- 5.3.5 Dashboards & visualization tools

- 5.4 Services

- 5.4.1 Professional

- 5.4.2 Managed

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Cloud-based

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Insurance, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Usage-Based Insurance (UBI)

- 9.2.1 Pay-As-You-Drive (PAYD)

- 9.2.2 Pay-How-You-Drive (PHYD)

- 9.2.3 Distance-based insurance

- 9.3 Behavior-based insurance

- 9.4 On-demand insurance

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Allstate Insurance

- 11.2 AXA Group

- 11.3 Cambridge Mobile Telematics

- 11.4 DriveQuant

- 11.5 GEICO

- 11.6 Imetrik Global

- 11.7 LexisNexis Risk Solutions

- 11.8 Liberty Mutual Insurance

- 11.9 Metromile

- 11.10 Nationwide Mutual Insurance

- 11.11 Octo Telematics

- 11.12 Progressive Corporation

- 11.13 Sierra Wireless

- 11.14 State Farm

- 11.15 The Floow

- 11.16 TrueMotion

- 11.17 UnipolTech SpA

- 11.18 Verizon Connect

- 11.19 Vodafone Automotive

- 11.20 Zubie

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日