欧州の保険テレマティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Insurance Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644560

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

欧州の保険テレマティクス市場規模は2025年に9億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは23.34%で、2030年には27億8,000万米ドルに達すると予測されます。

同市場では、プラグ・アンド・プレイ装置や車載インテリジェント・モニタリングシステムを通じて新しい手法が積極的に採用され、車両保険の購入に革命が起こると予想されます。欧州各国の政府規制も、保険テレマティクスのプロセスを義務化することで保険テレマティクスのアイデアを後押しし、市場成長を後押しするとみられます。

主要ハイライト

- テレマティクスとは、通信と情報学を組み合わせた用語です。テレマティクスは自動車保険において、運転関連データの追跡、保存、送信に使用されます。この情報は運転習慣を判断し、適切な車両保険料を決定するのに役立ちます。本レポートでは、「Pay-as-you-drive」、「Pay-how-you-drive」、「Manage-how-you-drive」の3つの利用ベースの保険ベースのテレマティクス収入モデルを取り上げています。

- 自動車保険市場における最新のイノベーションは、テレマティクス技術の統合です。テレマティクスの組み合わせは、ドライバーにより安全な運転スタイルを促し、同時に保険料の節約にも役立っています。テレマティクスの進歩により、最近では常時モニタリング装置が利用できるようになったため、ドライバーを正確に分析し、車両の安全確保を進めるのに役立っています。

- 利用ベースの保険(UBI)またはテレマティクスは、自動車保険の文脈でテレマティクス技術を使用するための用語です。自動車保険会社はこれらのソリューションを利用することで、運転データによる価格設定プロセスの改善、クレーム管理の向上、現在と将来の契約者との商品の差別化を図ることができます。行動ベースのプライシング方式は、調査対象地域のほとんどの保険会社で採用されており、さまざまなデータモニタリング技術を活用しています。

- 運輸省によると、2022年に英国で報告された交通事故による死亡者数は推定1,760人でした。さらに、同年に報告された死者・重傷者数は推定29,804人でした。このような交通事故死者数の増加が、調査対象市場のニーズを後押ししています。

- COVID-19の世界的大流行を受け、レンタル会社のような資産を多用する事業が混乱に陥っているため、車両管理ベンダーは顧客向けに新たな使用事例を開発し、物流や医療輸送の需要増に対応した車両シフトを支援することで、市場の成長を促進しています。

欧州の保険テレマティクス市場動向

保険会社による利用ベースの保険の採用が市場を牽引

- 利用ベースの保険(またはUBI)は、独自の追跡装置(通常は顧客の車内に設置)を使って運転行動を追跡します。ドライバーがどのようにアクセルを踏み、ブレーキを踏み、コーナーを曲がるかを調べることで、保険会社はその顧客により適切な保険料を決定できるというものです。このようなプログラムを採用している保険会社は、顧客がいつ運転し、どれくらいの時間ハンドルを握っているかも調べています。

- 今後数年間は、自動車産業の拡大が利用ベース保険市場を前進させると考えられます。自動車産業は、自動車の設計、生産、マーケティング、販売に関わる多くの企業や組織で構成されています。テレマティクス主導の利用ベース保険は、リスクの低い運転には低い保険料を、リスクの高い運転には高い保険料を提供するため、自動車所有者に魅力的です。その結果、個人は運転行動を変えることで保険料を大幅に引き下げることができます。

- 小型車(LDV)と大型車(HDV)は、使用ベース保険(UBI)の最も一般的な2つの車両クラスです。最大車両総重量が8500ポンド以下の乗用車は小型車に分類され、一方、大型車は車両総重量が大きいです。OBD-IIベースのUBIプログラム、スマートフォン・ベースのUBIプログラム、ハイブリッドベースのUBIプログラム、ブラックボックス・ベースのUBIプログラムは、PAYD(Pay-As-You-Drive)、PHYD(Pay-How-You-Drive)、MWYD(Manage-How-You-Drive)のような様々な種類の包装で利用されているいくつかの技術の一つです。

- 論点のひとつはプライバシーです。個人が利用ベースの保険を選択するのはひとつのことだが、ビジネスフリートがドライバーを定期的にモニタリングすることを要求するのはまったくによることです。しかし、テレマティクスでは、測定可能な利点が最終的にプライバシーの懸念を上回るというのが通常の規範であり、主にデータの収集と処理を匿名化することによって処理されます。現実には、運転行動の追跡と報告は、ドライバーにとってポジティブな経験となり、様々なベンチマークに照らしてパフォーマンスを向上させることができ、それによって安全運転の実践がゲーム化される可能性があります。

- 欧州自動車工業会(ACEA)によると、EUにおける2022年3月の乗用車登録台数は~20.5%減の84万4,187台でした。自動車生産は、ロシアのウクライナ侵攻によって悪化したサプライチェーンの持続的混乱によって打撃を受けています。その結果、スペイン(-30.2%)、イタリア(-29.7%)、フランス(-19.5%)、ドイツ(-17.5%)など、この地域のほとんどの国で販売台数が2桁減少しました。これはテレマティクス保険部門に打撃を与える可能性があります。

イタリアが最も急成長

- イタリアのテレマティクス保険市場は、テレマティクスをベースとした保険契約の採用が増加し、ドライバーに安全運転の習慣を示すことで保険料を節約する機会を提供することによって牽引されています。

- イタリア政府は、2022年以降すべての新車にテレマティクス機器を搭載することを義務付ける法律を制定し、テレマティクス市場の開拓を常に支援しています。この法律は、調査された市場の成長をさらに促進すると予想されます。

- イタリアのインシュアテック企業は、イタリアの顧客に新しいオプションや保険スキームを提供するために協力しています。これにより、従来の車両保険購入方法から詳細なテレマティクスの選択肢への顧客のスムーズな移行が促されると考えられます。

- Istatによると、当初の推定によると、2022年1月から6月までに死傷者を出した交通事故件数は2021年同期比で24.7%増加、負傷者数は25.7%増加、30日以内の死傷者数は15.3%増加しました。こうした交通事故死者数の増加は、保険テレマティクス市場の需要をさらに押し上げると予想されます。

欧州の保険テレマティクス産業概要

保険テレマティクス事業には複数の有力な参入企業があります。現在、市場シェアでかなりの地位を占めている参入企業は皆無に近いです。主要な競合企業は、産業のトップを維持するために、国境を越えて消費者基盤を拡大することに集中しています。これらの企業は、戦略的提携イニシアティブを利用して市場シェアと利益を拡大しています。産業参入企業はまた、保険テレマティクス市場技術に取り組む新興企業を買収し、製品力を強化しています。

- 2024年1月-OCTOは交通安全に革命を起こします。OCTOソリューションはユーザー体験を大きく変容させ、ドライバーが必要とする時に積極的にサポートします。OCTOソリューションは、ユーザー体験を大きく変革し、いざというときにドライバーを積極的にサポートします。スマートフォンをアクティブセンサに変えることで、深刻な衝突を検知し、人命への影響を軽減するために自動的に支援を要請します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析(OEM、保険会社、ネットワークプロバイダー、テレマティックプロバイダー)

- 欧州の自動車市場

- COVID-19が産業に与える影響

第5章 市場力学

- 市場促進要因

- 保険会社による利用ベース保険の採用拡大

- 市場課題

- データ品質と互換性の問題

第6章 市場セグメンテーション

- タイプ別

- PAYD(Pay-As-You-Drive)

- PHYD(Pay-How-You-Drive)

- MWYD(Manage-How-You-Drive)

- 国別

- イタリア

- 英国

- ドイツ

- その他の欧州

第7章 競合情勢

- 企業プロファイル

- Towergate Insurance

- Unipolsai Assicurazioni SpA

- Octo Telematics SpA

- Drive Quant

- IMERTIK Global Inc.

- AXA S.A.

- The Floow Limited

- LexisNexis Risks Solutions

- Vodafone Automotive SpA

- Viasat Group

- *List Not Exhaustive

第8章 投資分析

第9章 市場機会と今後の動向

目次

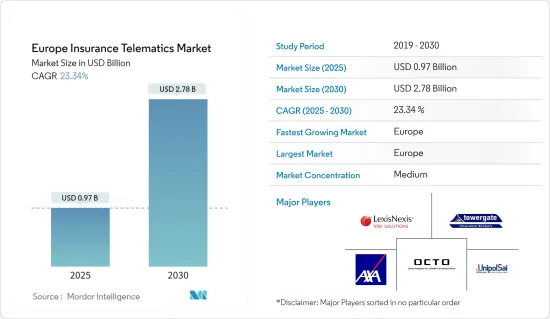

The Europe Insurance Telematics Market size is estimated at USD 0.97 billion in 2025, and is expected to reach USD 2.78 billion by 2030, at a CAGR of 23.34% during the forecast period (2025-2030).

The market is expected to witness the active adoption of new methods through plug-and-play apparatus and in-vehicle intelligent monitoring systems, revolutionizing buying vehicle insurance. Government regulations in different European countries are also likely to back the idea of insurance telematics by making the process mandatory and boosting market growth.

Key Highlights

- Telematics is a term that combines the terms telecommunication and informatics. Telematics is used in vehicle insurance to track, store, and send driving-related data. This information helps determine driving habits and determine appropriate vehicle insurance premiums. Pay-as-you-drive, Pay-how-you-drive, and Manage-how-you-drive are three usage-based insurance-based telematics income models discussed in the report.

- The latest innovation in the vehicle insurance market is the integration of telematics technology. The combination of telematics has helped encourage safer driving styles among drivers, helping them save on insurance premiums simultaneously. The constant monitoring device available these days due to advancements in telematics helps analyze the drivers accurately and proceed with ensuring their vehicles.

- Usage-based insurance (UBI) or telematics is the term for using telematics technology in the context of automobile insurance. Automotive insurers can use these solutions to improve pricing processes based on driving data, improve claim control, and distinguish their products from current and future policyholders. Behavior-based pricing schemes are adopted by most of the insurers in the regions studied, leveraging different data monitoring techniques.

- According to the Department of Transport, there were an estimated 1,760 fatalities in reported road accidents in Great Britain in 2022. Moreover, there were an estimated 29,804 reported killed or seriously injured in the same year. Such rising numbers of road fatalities are driving the need for the studied market.

- In the wake of the global COVID-19 pandemic, which has thrown asset-heavy businesses like rental companies into disarray, fleet management vendors are developing new use cases for their customers to help them shift fleets to meet the growing demand for logistic and medical transportation, thereby fostering the market growth.

Europe Insurance Telematics Market Trends

Adoption of Usage-based Insurance by Insurance Companies will Drive The Market

- Usage-based insurance (or UBI) uses a unique tracking device (usually placed within a client's vehicle) to track driving behavior. By examining how a driver accelerates, brakes, and corners, the idea is that an insurance company can determine a more appropriate premium for that client. Insurance companies who have adopted these programs also examine when clients drive and how much time they spend behind the wheel.

- In the coming years, the expansion of the vehicle industry is likely to move the usage-based insurance market forward. The automotive industry comprises many firms and organizations involved in automobile design, production, marketing, and sale. Telematics-driven usage-based insurance appeals to car owners since it offers low premiums for low-risk driving and high premiums for high-risk driving. As a result, individuals can significantly reduce their insurance prices by changing their driving behaviors.

- Light-duty vehicles (LDV) and heavy-duty vehicles (HDV) are the two most common vehicle classes for usage-based insurance (UBI). Passenger automobiles with a maximum gross vehicle weight of fewer than 8500 lbs are classified as light-duty vehicles, whereas heavy-duty vehicles have a higher gross vehicle weight. OBD-II-based UBI programs, smartphone-based UBI programs, hybrid-based UBI programs, and black-box-based UBI programs are among the several technologies that are utilized in various sorts of packages such as pay-as-you-drive (PAYD), pay-how-you-drive (PHYD), and manage-how-you-drive (MWYD).

- One point of contention is privacy. It's one thing for private individuals to choose usage-based insurance, but it's quite another for business fleets to demand that their drivers be regularly watched. However, with telematics, the usual norm is that measurable benefits eventually surpass privacy concerns, primarily handled by anonymizing data collection and processing. In reality, tracking and reporting on driving behavior might be a positive experience for drivers, allowing them to improve their performance against various benchmarks, thereby gamifying the practice of safe driving.

- According to the European Automobile Manufacturers Association (ACEA), the count of passenger car registrations in the European Union reduced by -20.5% in March 2022, with 844,187 units sold. Car production has been harmed by persistent supply chain disruptions, worsened by Russia's invasion of Ukraine. As a result, most nations in the region saw double-digit sales declines, including Spain (-30.2%), Italy (-29.7%), France (-19.5 %), and Germany (-17.5%). This could harm the telematics insurance sector.

Italy to Account for the Fastest Growth

- The insurance telematics market in Italy is driven by the rising adoption of telematics-based insurance policies, which offer drivers the opportunity to save money on their premiums by demonstrating safe driving habits.

- The Italian government is constantly supporting the developments of the telematics market with legislation requiring all new cars to be equipped with telematics devices from 2022. This legislation is further expected to drive the growth of the studied market.

- Italian insurtech companies collaborate to bring new options and insurance schemes to Italian customers. This would encourage a smoother transition of the clients from traditional methods of buying vehicle insurance to detailed telematics alternatives.

- According to Istat, as per the initial estimates, the number of road accidents resulting in death or injury has increased by 24.7%, the number of injured by 25.7%, and the number of casualties within 30 days by 15.3% increased from January to June 2022 compared to the same period in 2021. Such increased number of road fatalities is further expected to boost the demand for insurance telematics market.

Europe Insurance Telematics Industry Overview

There are several prominent participants in the insurance telematics business. Nearly none of the market players now hold a considerable position in terms of market share. The major competitors concentrate on growing their consumer base beyond international borders to stay on top of the industry. These businesses use strategic collaboration initiatives to expand their market share and profits. Industry players also purchase start-ups working on insurance telematics market technology to strengthen their product capabilities.

- January 2024 - OCTO is revolutionizing road safety; the OCTO solution is profoundly transformative in the user experience, proactively supporting drivers in their time of need. It does this by turning the smartphone into an active sensor for detecting severe crashes and automatically requesting assistance to reduce the impact on human life.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Porters Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis (OEMs, Insurance Companies, Network Providers, and Telematic Providers)

- 4.4 Automotive Market in Europe

- 4.5 Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Usage-based Insurance by Insurance Companies

- 5.2 Market Challenge

- 5.2.1 Data Quality and Compatibility Issues

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Pay-As-You-Drive

- 6.1.2 Pay-How-You-Drive

- 6.1.3 Manage-How-You-Drive

- 6.2 BY COUNTRY

- 6.2.1 Italy

- 6.2.2 United Kingdom

- 6.2.3 Germany

- 6.2.4 Rest of the Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Towergate Insurance

- 7.1.2 Unipolsai Assicurazioni SpA

- 7.1.3 Octo Telematics SpA

- 7.1.4 Drive Quant

- 7.1.5 IMERTIK Global Inc.

- 7.1.6 AXA S.A.

- 7.1.7 The Floow Limited

- 7.1.8 LexisNexis Risks Solutions

- 7.1.9 Vodafone Automotive SpA

- 7.1.10 Viasat Group

- 7.1.11 *List Not Exhaustive

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日