|

市場調査レポート

商品コード

1690988

英国のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)United Kingdom Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 281 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

英国のたんぱく質の市場規模は2025年に6億2,200万米ドルと推定され、2030年には8億770万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは5.36%で成長する見込みです。

健康志向の製品への嗜好の高まりとたんぱく質に対する社会の意識が成長に影響

- 用途別では、2022年、この地域ではF&B産業がたんぱく質の主要用途分野であり、次いで動物飼料分野でした。F&B分野では、肉・肉代替品分野が32.40%の数量シェアを占め、次いで乳製品・乳製品代替品分野が2022年に27.9%の数量シェアを占める。英国は肉・乳製品代替製品の主要市場です。同市場は、植物、海藻、非動物細胞培養、発酵、培養肉に由来する健康的なタンパク源を継続的に発表しており、これらはより伝統的なタンパク源に代わるものを提供しています。

- 動物飼料部門は、2020年には数量ベースで35.5%と、市場で2番目に大きなシェアを占めており、予測期間中、公称CAGR値2.65%で市場を牽引すると予測されています。市場拡大を後押しする主な要因の1つは、動物飼料における藻類ベースのたんぱく質成分の健康上の利点に対する社会的認知の高まりです。ウシの開発初期段階において、微細藻類は動物飼料に栄養素を添加するために極めて重要です。また、身体の成長を促進し、高品質の卵、牛乳、肉の生産を保証します。

- 金額ベースでは、すべてのエンドユーザーセグメントの中で、サプリメントセグメントは、予測期間中に6.47%の最速の成長率を記録すると予想されています。健康志向の製品への嗜好の高まりと成分リストへの関心の高まりが、市場の成長を大きく後押ししています。サプリメントのカテゴリーでは、スポーツ栄養とパフォーマンス栄養が市場で突出したシェアを占めています。これは主に、日々の栄養摂取に関する意識の高まりによるもので、スポーツ栄養製品は消化や消費中に失われる栄養素を補うのに役立ちます。

英国のたんぱく質市場動向

動物性たんぱく質の消費拡大が原料部門の主要企業にチャンスを与える

- 英国の消費者は、都市化の進展、高齢者人口の増加、ライフスタイルの変化、登録労働者における女性の増加により、より健康的な食品の選択肢を求めています。たんぱく質強化食品に対する需要も、同国の消費者の間で日々の食事要件を満たすために高まっています。動物性たんぱく質は、知名度の低い商品から価値を高める成分へと変貌を遂げています。動物性たんぱく質全体の1人当たり消費量は、2018年の60.4gから2022年には65.2gに増加しました。

- 高度に成熟した飲食品業界では、健康志向の人々から高品質のたんぱく質原料に対する需要が高まっています。また、英国ではパーソナルケアやスポーツ栄養製品の人気も高まっています。これらの産業が動物性たんぱく質市場を後押ししています。動物性たんぱく質は、体重管理を促進し、免疫力を高める製品の主要成分のひとつです。2022年7月現在、英国の消費者の約40%が、運動スケジュールのために飲食品を選ぶ際にたんぱく質を探しています。18~29歳では需要が50%近く増加しました。

- 総合的な健康とクリーンラベル製品に大きな注目が集まる中、スポーツ栄養セグメントからの天然成分への需要が伸びています。ホエイたんぱく質市場は、健康的なライフスタイルを送るという意向の高まりが主な要因となっています。ヘルス&フィットネスクラブの数は、この動向によって大きく増加し、市場成長の可能性を大きく高めています。英国のホエイたんぱく質市場もまた、高品質なたんぱく質原料に対する消費者の需要における業界の経験によって牽引されました。英国のジムとフィットネスセンターの数は、2017年の2,642から2021年には3,060に増加しました。

乳製品加工産業の急速な開発が生乳生産を促進する

- 動物性たんぱく質市場には、牛、鶏、豚の骨付き肉、牛の生乳、牛の脱脂乳、乾燥ホエイパウダーのような明確な原材料の生産が含まれます。消費者は、牛肉/仔牛肉や豚肉を含む自家と畜肉の消費に傾いています。2020年には、牛肉・子牛肉と豚肉の需要はそれぞれ1.92%と2.81%増加し、93万2,100トンと98万4,300トンに達します。食肉生産量の絶え間ない増加は、同国の動物性たんぱく質部門に貢献しています。

- 英国では、乳牛の頭数が減少し続けているにもかかわらず、牛乳生産量は絶えず増加しています。2016年から2019年の間、19歳から64歳の個人の1日平均たんぱく質摂取量は1人当たり76gで、成人の1日平均必要摂取量の64g/日を上回っていました。この数値は、1日当たり体重0.83g/kgの摂取基準値を用いて算出されました。1人当たりの1日平均動物性たんぱく質消費量は39.6gと予測され、25.9gが肉および肉製品から、9.9gが牛乳および牛乳製品から摂取されています。それに伴い、国内の牛乳生産量は増加しています。国内生産量の7%未満が輸出されており、メーカーにとっては入手しやすいです。

- 予測年である2023年は、英国の養豚業界にとって課題でした。2022年に繁殖豚群が縮小したため、2023年には仕上豚数が大幅に減少しました。この結果、清浄豚のと畜頭数が過去10年間で最低の数に減少したため、生産量は前年比で減少すると予想されました。豚の生産コストは2023年に低下し、純マージンは2年以上ぶりにプラスに転じた。

英国のたんぱく質産業の概要

英国のたんぱく質市場は細分化されており、上位5社で27.23%を占めています。この市場の主要企業は以下の通りです。Archer Daniels Midland Company, Arla Foods AmbA, Darling Ingredients Inc., International Flavors & Fragrances Inc. and Kerry Group PLC(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物性

- 植物性

- 生産動向

- 動物

- 植物

- 規制の枠組み

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 原料

- 動物

- たんぱく質タイプ別

- カゼインとカゼイネート

- コラーゲン

- 卵たんぱく質

- ゼラチン

- 昆虫たんぱく質

- ミルクたんぱく質

- ホエイたんぱく質

- その他の動物性たんぱく質

- 微生物

- たんぱく質タイプ別

- 藻類たんぱく質

- マイコたんぱく質

- 植物

- たんぱく質タイプ別

- ヘンプ・たんぱく質

- エンドウ豆たんぱく質

- ジャガイモ・たんぱく質

- 米たんぱく質

- 大豆たんぱく質

- 小麦たんぱく質

- その他の植物性たんぱく質

- 動物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- A. Costantino & C. SpA

- Agrial Enterprise

- Archer Daniels Midland Company

- Arla Foods AmbA

- Darling Ingredients Inc.

- Glanbia PLC

- International Flavors & Fragrances Inc.

- Kernel Mycofood

- Kerry Group PLC

- Roquette Freres

- Volac International Limited

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

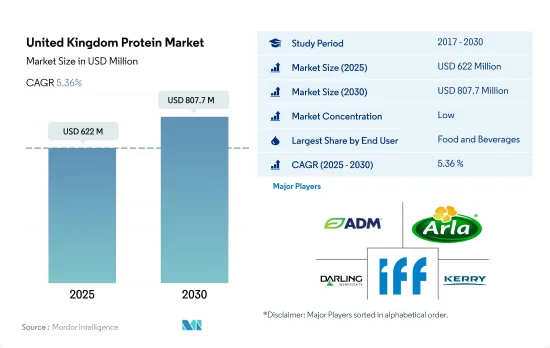

The United Kingdom Protein Market size is estimated at 622 million USD in 2025, and is expected to reach 807.7 million USD by 2030, growing at a CAGR of 5.36% during the forecast period (2025-2030).

Emerging indulgence towards health-oriented products with public awareness on protein is impacting the growth

- By application, in 2022, the F&B industry was the leading application sector for protein in the region, followed by the animal feed sector. In the F&B category, the meat/meat alternatives segment accounted for the major volume share of 32.40%, followed by the dairy and dairy alternatives segment, with 27.9% by volume share in 2022. The United Kingdom is the leading market for the meat and dairy alternative products. The market is continuously launching healthy sources of protein derived from plants, seaweed, non-animal cell culture, fermentation, or cultivated meat, which provide an alternative to more traditional protein sources.

- The animal feed segment occupied the second-largest share in the market, i.e., 35.5% by volume in 2020, which is anticipated to drive the market with a nominal CAGR value of 2.65% during the forecast period. One of the main factors fueling market expansion is the growing public awareness of the health benefits of algae-based protein ingredients in animal feed. In the early stages of bovine development, microalgae are crucial for adding nutrients to animal feed. It also promotes physical growth and ensures the production of high-quality eggs, milk, and meat.

- By value, among all the end-user segments, the supplement segment is anticipated to register the fastest growth rate of 6.47% during the forecast period. The emerging indulgence toward health-oriented products, along with rising interest in the list of ingredients, is highly driving the market's growth. Under the supplement category, sport and performance nutrition holds a prominent share of the market, mainly due to the rising awareness regarding daily nutritional intake, and sports nutrition products aid in compensating for nutrients lost during digestion and consumption.

United Kingdom Protein Market Trends

The consumption growth of animal protein fuels opportunities for key players in the ingredients segment

- Consumers in the United Kingdom are looking for healthier food options due to increasing urbanization, the growing geriatric population, lifestyle changes, and the increasing number of women in the registered workforce. The demand for protein-fortified foods is also growing among consumers in the country to meet their daily dietary requirements. Animal protein has transformed from a low-profile commodity to a value-enhancing ingredient. The per capita consumption of overall animal protein increased from 60.4 g in 2018 to 65.2 g in 2022.

- The highly matured food and beverage industry witnessed a rising demand for high-quality protein ingredients from health-conscious people. There is also a growing popularity of personal care and sports nutrition products in the United Kingdom. These industries are boosting the animal protein market. Animal protein is one of the primary ingredients in products that promote weight management and boost immunity. As of July 2022, around 40% of consumers in the United Kingdom looked for protein while choosing foods and beverages for their exercise schedules. The demand rose by almost 50% among people aged 18-29 years.

- With a significant focus on overall health and clean-label products, the demand for natural ingredients from the sports nutrition segment is growing. The market for whey protein is mostly driven by the rising intention of leading healthy lifestyles. The number of health and fitness clubs increased largely due to this trend, significantly enhancing the market's growth possibilities. The UK whey protein market was also driven by the industry's experience in consumers' demand for high-quality protein ingredients. The number of gyms and fitness centers in the United Kingdom increased from 2,642 in 2017 to 3,060 in 2021.

Rapid development in dairy processing industry to drive milk production

- The animal protein market include the production of distinct raw materials, like meat from cattle, chickens, and pigs with bone, raw milk from cattle, skim milk from cows, and dry whey powder. Consumers are inclined toward consuming home-slaughtered meat, including beef/veal and pig. In 2020, the demand for beef/veal and pig meat increased by 1.92% and 2.81%, respectively, amounting to 932.10 thousand tons and 984.30 thousand tons, respectively. The constant rise in meat production is catering to the country's animal protein sector.

- Milk production is constantly rising in the United Kingdom despite the continuous decline in the number of dairy cows. During 2016-2019, the average daily protein intake of individuals aged 19 to 64 years was 76 g per person, which was more than the 64 g/day average adult daily requirement. This number was calculated using a reference intake value of 0.83 g/kg of body weight per day. The average daily consumption of animal protein per person is projected to be 39.6 g, with 25.9 g coming from meat and meat products and 9.9 g from milk and milk products. Accordingly, the total domestic milk production has risen. Less than 7% of the domestic production is exported, providing easy access to manufacturers.

- The forecast year, 2023, was challenging for the UK pig industry. The contraction in the breeding herd in 2022 led to a significant reduction in the number of finishing pigs in 2023. This, in turn, was expected to result in production volumes falling Y-o-Y as clean pig slaughter fell to its lowest number in a decade. The estimated cost of pig production fell in 2023 and moved net margins into a positive position for the first time in over two years.

United Kingdom Protein Industry Overview

The United Kingdom Protein Market is fragmented, with the top five companies occupying 27.23%. The major players in this market are Archer Daniels Midland Company, Arla Foods AmbA, Darling Ingredients Inc., International Flavors & Fragrances Inc. and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 United Kingdom

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Agrial Enterprise

- 5.4.3 Archer Daniels Midland Company

- 5.4.4 Arla Foods AmbA

- 5.4.5 Darling Ingredients Inc.

- 5.4.6 Glanbia PLC

- 5.4.7 International Flavors & Fragrances Inc.

- 5.4.8 Kernel Mycofood

- 5.4.9 Kerry Group PLC

- 5.4.10 Roquette Freres

- 5.4.11 Volac International Limited

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms