|

市場調査レポート

商品コード

1690938

インドネシアの防衛:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Indonesia Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシアの防衛:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

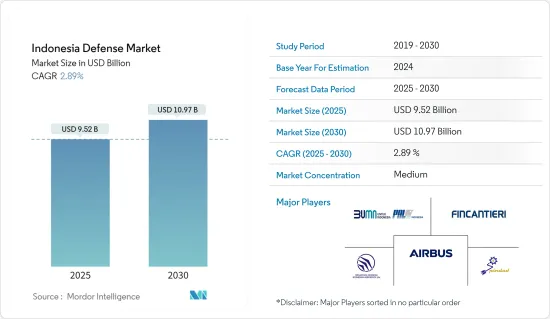

インドネシアの防衛の市場規模は2025年に95億2,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは2.89%で、2030年には109億7,000万米ドルに達すると予測されます。

インドネシアでは、先進的な軍事機器に対する需要の高まりを受けて、防衛産業の強化に力を入れています。政府の戦略では、長期的な自給自足への道を開くため、大手OEMからの技術移転を重視しながら、武器や防衛システムを調達しています。インドネシア国内では、陸上車両、武器、ミサイル、UAVの専門技術を磨いています。今後数年間は、飛行制御装置、弾頭、ジェットエンジンなど、より複雑なシステムに進出する計画です。

MEF構想の下、インドネシアは能力ベースの防衛アプローチを採用し、軍備を強化しています。この戦略は、脅威の評価と財政能力に見合った防衛資産の獲得を伴う。特筆すべきは、インドネシアや他のASEAN諸国が南シナ海で中国との領土紛争に巻き込まれているため、インドネシア政府が軍事投資を活発化させていることです。

さらにインドネシアは、進化する戦略情勢をうまく乗り切るため、老朽化した防衛システムの大幅な見直しを考えています。このような近代化の推進が市場の成長を後押ししており、予測期間中はプラスの軌道を描くと見られています。

インドネシアの防衛市場の動向

最も高い成長が見込まれる弾薬セグメント

インドネシアの地政学的緊張の高まりと防衛予算の増加が市場の需要を促進しています。2023年、インドネシアの防衛費は94億8,000万米ドルに達します。現政権は、最小必要戦力(MEF)目標の達成という課題に直面しています。この遅れは主に予算の制約と政治的不確実性に起因します。2022年6月、インドネシアは2019年から2024年までのMEF目標を70%に修正しました。軍事的野心と地域の安全保障上の懸念に後押しされ、インドネシアは防衛支出を強化しました。同国の軍隊は陸海空軍合わせて約40万4,500人で、さまざまな銃器を装備しています。こうした需要の高まりは、最近の調達活動にも表れています。例えば、2023年7月、インドネシア警察は330万米ドルに相当する1,857丁の暴動用銃を確保しました。

インドネシアは、近代化のニーズに対して地元企業を優先させる構えで、外国のサプライヤーへの依存度を下げることを目指しています。また、国内防衛産業を強化するため、技術移転とオフセットを重視する計画です。この方向での顕著な動きは、2023年8月にインドネシアが防衛部門強化のためにサウジアラビアに支援を求めた際に見られました。この協議の中で、ピンバドのような国営兵器メーカーがその能力を披露し、防衛生産における自給自足への推進を示唆しました。このように、防衛力強化のための投資拡大と先進弾薬の調達増加が、このセグメントの成長を牽引しています。

予測期間中、航空機が市場を独占する

インドネシアの大統領府は、2040年代半ばまでに1,250億米ドルを投資するという野心的な軍事近代化計画を発表しました。この計画は、インドネシアが外国からの融資に依存し続けていることを強調しています。具体的には、防衛装備品に790億米ドル、25年間の維持費に325億米ドル、そして残りの134億米ドルを対外融資の利払いに充てるとしています。

財務省の文書によると、2022年には防衛予算の約32%が近代化プロジェクトに充てられ、調達と維持が対象となります。特筆すべきは、固定翼航空機の増強です。2024年1月、インドネシアではラファール18機の最終納入が開始されました。これは、2022年9月と2023年8月にそれぞれ6機と18機のラファールが納入されたのに続くもので、インドネシアが2022年2月に発注した42機の航空機の注文を満たすことになります。2024年2月、インドネシアはさらに3機のCN235-220輸送機を国営航空宇宙会社PT Dirgantara Indonesia(PTDI)に8,500万米ドルで発注しました。広く評価されているC-130ハーキュリーズよりも軽量かつコンパクトに設計されたCN-235は、特にC-130のような大型の輸送プラットフォームを使用することが非効率的である場合に、補完的な資産となります。これらの調達努力は、防衛予算のより大きな割合を必要とする態勢を整えており、現政権に課題を突きつける可能性があります。

インドネシアの防衛市場の産業概要

インドネシアの防衛市場は半固定的です。過去、インドネシアは主要な軍事機器の調達を外国の防衛請負業者に依存していました。しかし、最近の動向では、インドネシアは国営企業の開発に力を入れています。PT PAL Indonesia、PT Pindad、PT Dirgantara Indonesia、Airbus SE、FINCANTIERI SpAなどが市場の主要企業です。

政府からの最近の防衛契約は、地元企業の繁栄を助けた。しかし、予算の制約がこれらの企業の成長機会をすぐに妨げる可能性があります。日本やインドなど他のアジア諸国との緊密な関係は、同国の防衛産業の成長を助け、輸出を通じて経済に貢献しています。共同防衛生産計画は、現地の防衛産業の将来のサプライ・チェーンをさらに強化することができます。このように、インドネシアが大規模な軍備近代化を計画している中、防衛企業はインドネシアの防衛市場で存在感を高める大きな成長機会を手にしています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- 人員訓練と保護

- 通信システム

- 武器・弾薬

- 砲兵および迫撃砲システム

- 歩兵兵器

- ミサイルおよびミサイル防衛システム

- 弾薬

- ビークル別

- 陸上機

- 海洋機

- 航空機

第6章 競合情勢

- 企業プロファイル

- PT PAL Indonesia

- PT Pindad

- PT. Dirgantara Indonesia

- PT Len Industri

- PT. Dahana

- SCYTALYS

- Leonardo SpA

- Airbus SE

- BAE Systems PLC

- FINCANTIERI SpA

- Kongsberg Gruppen ASA

- Daewoo Shipbuilding & Marine Engineering Co. Ltd

第7章 市場機会と今後の動向

The Indonesia Defense Market size is estimated at USD 9.52 billion in 2025, and is expected to reach USD 10.97 billion by 2030, at a CAGR of 2.89% during the forecast period (2025-2030).

Indonesia is intensifying its focus on bolstering the local defense industry in response to rising demand for advanced military equipment. The government's strategy involves procuring weapons and defense systems, emphasizing technology transfers from leading OEMs to pave the way for long-term self-sufficiency. Domestically, Indonesian entities are honing their expertise in land vehicles, arms, missiles, and UAVs. In the coming years, they plan to venture into more intricate systems like flight controls, warheads, and jet engines.

Under the MEF initiative, Indonesia is adopting a capability-based defense approach to fortify its armed forces. This strategy entails acquiring defense assets aligned with threat assessments and financial capabilities. Notably, Indonesia and other ASEAN nations are embroiled in territorial conflicts with China in the South China Sea, prompting heightened military investments from the Indonesian government.

Furthermore, Indonesia is contemplating a significant overhaul of its aging defense systems to better navigate the evolving strategic landscape. This modernization thrust is propelling the market's growth, with projections indicating a positive trajectory during the forecast period.

Indonesia Defense Market Trends

Ammunition Segment Expected to Show Highest Growth

Indonesia's rising geopolitical tensions and increased defense budgets have fueled market demand. In 2023, Indonesia's defense spending reached USD 9.48 billion. The current administration faces challenges in meeting its minimum essential force (MEF) target. This delay primarily stems from budget constraints and political uncertainties. In June 2022, Indonesia revised its MEF target to 70% for the 2019-2024 phase. Driven by its military ambitions and regional security concerns, Indonesia bolstered its defense spending. The nation's military comprises approximately 404,500 personnel across its Army, Navy, and Air Force, all equipped with various firearms. This heightened demand is evident in recent procurement activities. For instance, in July 2023, the Indonesian police secured 1,857 riot guns worth USD 3.3 million.

Indonesia is poised to prioritize local firms for its modernization needs, aiming to lessen its reliance on foreign suppliers. The nation also plans to emphasize technology transfers and offsets to bolster its domestic defense industry. A notable move in this direction was seen in August 2023 when Indonesia sought assistance from Saudi Arabia to enhance its defense sector. During the discussions, state-owned arms manufacturers like Pinbad showcased their capabilities, signaling a push toward self-sufficiency in defense production. Thus, growing investment in enhancing defense capabilities and rising procurement of advanced ammunition are driving the growth of the segment.

Air-based Vehicles to Dominate the Market During the Forecast Period

Indonesia's presidential office has outlined an ambitious military modernization plan, earmarking a substantial USD 125 billion investment through the mid-2040s. This plan underscores Indonesia's ongoing reliance on foreign loans. Specifically, the proposal allocates USD 79 billion for defense equipment, another USD 32.5 billion for sustainment over 25 years, and the remaining USD 13.4 billion to service interest on foreign loans.

Documents from the Ministry of Finance indicate that in 2022, approximately 32% of the defense budget was earmarked for modernization projects, covering procurement and sustainment. Notably, the country is bolstering its fixed-wing aircraft fleet. In January 2024, Indonesia saw the final installment of 18 Rafale aircraft come into effect. This followed the earlier deliveries of 6 and 18 Rafale aircraft in September 2022 and August 2023, respectively, culminating in fulfilling the 42-aircraft order placed by Indonesia in February 2022. In February 2024, Indonesia ordered three more CN235-220 transport aircraft from the state-owned aerospace company PT Dirgantara Indonesia (PTDI) for USD 85 million. The CN-235, designed to be lighter and more compact than the widely acclaimed C-130 Hercules, is a complementary asset, especially when using a larger transport platform like the C-130 would be inefficient. These procurement endeavors are poised to necessitate a larger share of the defense budget, potentially posing a challenge for the incumbent government.

Indonesia Defense Market Industry Overview

Indonesia's defense market is semi-consolidated. In the past, Indonesia depended on foreign defense contractors to procure major military equipment. However, in recent years, Indonesia has focused more on developing its state-owned companies. PT PAL Indonesia, PT Pindad, PT Dirgantara Indonesia, Airbus SE, and FINCANTIERI SpA are some of the major players in the market.

Recent defense contracts from the government helped the local companies to prosper. However, budget constraints can hamper the growth opportunities of these companies soon. Close relationships with other Asian countries like Japan and India helped the country's defense industry grow and contribute to the economy through exports. Joint defense production plans can further enhance the future supply chain of the local defense industry. Thus, as Indonesia plans for a major military equipment modernization, defense companies have a significant growth opportunity to increase their presence in the Indonesian defense market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Personnel Training and Protection

- 5.1.2 Communication Systems

- 5.1.3 Weapons and Ammunitions

- 5.1.3.1 Artillery and Mortar Systems

- 5.1.3.2 Infantry Weapons

- 5.1.3.3 Missile and Missile Defense Systems

- 5.1.3.4 Ammunition

- 5.1.4 By Vehicles

- 5.1.4.1 Land-based Vehicles

- 5.1.4.2 Sea-based Vehicles

- 5.1.4.3 Air-based Vehicles

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 PT PAL Indonesia

- 6.1.2 PT Pindad

- 6.1.3 PT. Dirgantara Indonesia

- 6.1.4 PT Len Industri

- 6.1.5 PT. Dahana

- 6.1.6 SCYTALYS

- 6.1.7 Leonardo SpA

- 6.1.8 Airbus SE

- 6.1.9 BAE Systems PLC

- 6.1.10 FINCANTIERI SpA

- 6.1.11 Kongsberg Gruppen ASA

- 6.1.12 Daewoo Shipbuilding & Marine Engineering Co. Ltd