|

市場調査レポート

商品コード

1690722

北米の自動車ロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の自動車ロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

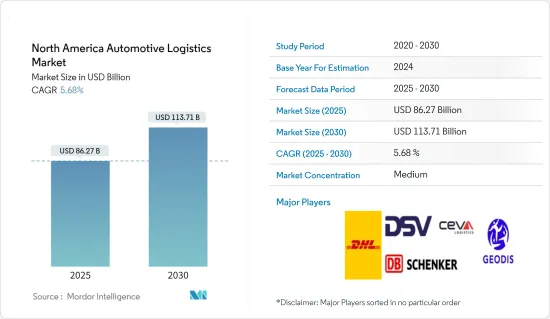

北米の自動車ロジスティクスの市場規模は2025年に862億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは5.68%で、2030年には1,137億1,000万米ドルに達すると予測されます。

北米の自動車ロジスティクスが大きな変化とチャンスを迎えていることはほとんどないです。しかし、広範な自動車業界と同様、自動車ロジスティクスが直面する経済・貿易リスク、新たな規制、消費者行動、投資利益率に関する不確実性はほとんどないです。

かつてないほどの可視性と柔軟性により、車両ロジスティクス・セクターは競争に打ち勝たなければならないです。OEM、ロジスティクス、テクノロジー・プロバイダーは、サプライチェーンの効率的な流れを維持するために、データを共有し、計画を立て、テクノロジーをアップグレードするために協力しなければならないです。

自動車サプライチェーンの将来は、自動車セクターのロジスティクス・サービス・プロバイダー、そしてマクロレベルでは経済全体にとって極めて重要です。自動車のサプライチェーン構造が変われば、世界貿易の性質や各国経済のダイナミズムが影響を受ける可能性があります。

世界の自動車生産施設の増加が、自動車ロジスティクス市場の成長を促しています。さらに、自動車メーカーがロジスティクス・プロバイダーに大きなビジネスチャンスをもたらしているため、市場の成長は今後数年で加速すると予想されます。不況後の新興国経済は着実な成長を遂げ、消費者の可処分所得の増加をもたらしています。

北米の自動車ロジスティクス市場動向

小型自動車生産への需要

- 北米では、消費者の嗜好がスポーツ・ユーティリティ・ビークルやトラックにシフトしており、自動車メーカーは需要増に対応した生産体制を整えています。その例として、フォード・エクスプローラーやシボレー・シルバラードといったモデルの人気が挙げられます。

- 電気自動車の増産は、ハイブリッド車やEVへの関心の高まりによるものです。例えば、2023年12月、テスラのギガファクトリーがテキサスに建設されたが、これは北米における電気自動車の需要増に対応することを目的としていました。

- 北米の自動車業界は、厳しい排ガス規制に対応するための技術への適応と投資を進めており、小型自動車の設計と生産に影響を与えています。2022年8月、米国政府は歴史的なインフレ抑制法に署名し、これは米国史上最も重要な経済・気候関連法案となる可能性があります。米国の製造能力復活の原動力となったインフレ削減法は、クリーン・エネルギー技術の開発と製造に幅広いインセンティブを提供します。

- 小型自動車生産の需要が高まるにつれ、自動車物流会社は輸送量の増加に見舞われます。より多くの車両や部品を製造施設から配送センターや販売店に輸送しなければならないです。

米国におけるEVブースト

- EVの普及には、連邦政府および州レベルのインセンティブが欠かせないです。連邦政府は、対象となる電気自動車の購入に対して税額控除を提供しています。例えば、適格プラグイン電気自動車クレジットでは、最大7,500米ドルのクレジットが提供されます。

- 大手自動車メーカーも電気自動車に積極的に取り組んでいます。ゼネラルモーターズ(GM)やフォードなどの企業は、電気自動車の開発と生産に投資する計画を発表しています。2024年1月、フォード・モーターは、ミネソタ州を拠点とする企業と、1,000台の全電気自動車、具体的にはF-150ライトニングとマスタング・マッハEを購入する契約を結びました。

- 2023年の最初の11ヶ月間に、EVの登録台数は100万台を超え、市場全体の約7.4%に達した(2022年の同時期の5.4%から上昇)。また専門家は、2023年には約110万台のバッテリー電気自動車(BEV)が販売されたと述べています。テスラは2023年にモデル3/Yを173万9,707台販売しました。

- また、2025年燃費基準の撤回や大気浄化法に基づく州の権限について連邦政府および国政関係者の間で議論が続いていることから、市場の持続的成長は規制の動向にも左右されます。

北米の自動車物流産業の概要

北米の自動車物流市場は断片化されています。EV需要の増加、軽量車両の増加、その他いくつかの要因が、今後数年間の市場成長を牽引すると思われます。競合情勢は、以下のような主要企業によって特徴付けられます。 DHL Supply Chain, Ryder System, and C.H. Robinson. These companies offer a comprehensive range of logistics and supply chain solutions, leveraging their global networks and advanced technologies.

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 政府の規制と取り組み

- バリューチェーン/サプライチェーン分析

- 業界の技術動向

- スポットライト:従来の自動車物流サプライチェーンに対するeコマースの影響

- 自動車アフターマーケットとその物流活動に関する洞察

第5章 市場力学

- 市場促進要因

- 環境問題への懸念と規制

- 自動車技術の進歩

- 市場抑制要因

- 経済の不確実性

- 市場機会

- 電気自動車の普及

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- サービス別

- 輸送

- 倉庫、流通、在庫管理

- その他のサービス

- タイプ別

- 完成車

- 自動車コンポーネント

- その他

- 国別

- 米国

- カナダ

- メキシコ

第7章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- CEVA Logistics AG

- DB Schenker

- DHL

- DSV

- GEODIS

- KUEHNE+NAGEL International AG

- Nippon Express Co. Ltd

- Ryder System Inc.

- XPO Logistics Inc.

- United Parcel Service Inc.*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

- 活動別GDP分布

- 資本フローの洞察

- 経済統計-運輸・倉庫部門、経済への貢献

The North America Automotive Logistics Market size is estimated at USD 86.27 billion in 2025, and is expected to reach USD 113.71 billion by 2030, at a CAGR of 5.68% during the forecast period (2025-2030).

North American automotive logistics has rarely been on the verge of much change and opportunity. Yet, as in the broader automotive industry, there are few uncertainties about economic and trade risks, new regulations, consumer behavior, or returns on investment faced by vehicle logistics.

With greater visibility and more flexibility than ever before, the vehicle logistics sector must be able to compete. OEMs, logistics, and technology providers must collaborate to share data, plan, and upgrade technology to keep the supply chain flowing efficiently.

The future of automotive supply chains is vital to logistics service providers in the automotive sector and, at the macro level, whole economies. The nature of global trade and the dynamics of different national economies can be affected by any change in the supply chain structure for vehicles.

An increasing number of vehicle production facilities worldwide compels the growth of the automotive logistics market. In addition, the market growth is expected to accelerate in the coming years due to automobile manufacturers' significant business opportunities for logistics providers. In the post-recession era, emerging economies have seen steady growth, leading to a rise in disposable income for consumers.

North America Automotive Logistics Market Trends

Demand for Light Vehicle Production

- In North America, consumer preferences have shifted to sport utility vehicles and trucks, driving auto manufacturers to adapt their production to meet rising demand. Instances include the popularity of models like Ford Explorer and Chevrolet Silverado.

- Increased production of electric vehicles results from the increasing interest in hybrids and EVs. For example, in December 2023, Tesla's Gigafactory in Texas aimed to meet North America's growing demand for electric vehicles.

- The automotive industry in North America has been adapting to and investing in technologies to meet stringent emission standards, influencing the design and production of light vehicles. In August 2022, the US government signed the historic Inflation Reduction Act into law, which could prove to be the most critical economic and climate legislation in American history. The Act to reduce inflation, which has driven a revival in US manufacturing capacity, offers broad incentives for developing and manufacturing clean energy technologies.

- As the demand for light vehicle production rises, automotive logistics companies experience increased shipping volumes. More vehicles and components must be transported from manufacturing facilities to distribution centers and dealerships.

EV Boost in United States

- Federal and state-level incentives have been crucial in promoting EV adoption. The federal government offers tax credits for the purchase of qualifying electric vehicles. For instance, the Qualified Plug-In Electric Drive Motor Vehicle Credit provides a credit of up to USD 7,500.

- Major automakers have made substantial commitments to electric vehicles. Companies like General Motors (GM), Ford, and others have announced plans to invest in developing and producing electric vehicles. In January 2024, Ford Motor Co. inked a deal with a Minnesota-based company to buy a fleet of 1,000 all-electric vehicles, specifically the F-150 Lightning and Mustang Mach-E.

- During the first 11 months of 2023, EV registrations exceeded 1 million units, which is about 7.4% of the total market (up from 5.4% at this same time in 2022). Experts also stated that around 1.1 million battery-electric vehicles (BEVs) were sold in 2023. Tesla sold 1,739,707 Model 3/Y cars in 2023.

- The market's sustainable growth also depends on regulatory developments, given ongoing discussions among federal and national parties regarding the rollback of 2025 fuel-economy standards and state authority under the Clean Air Act.

North America Automotive Logistics Industry Overview

The North American Automotive Logistics Market is fragmented. The increasing demand for EVs, an increase in lighter vehicles, and several other factors are likely to drive the market's growth over the coming years. The competitive landscape is marked by key players such as DHL Supply Chain, Ryder System, and C.H. Robinson. These companies offer a comprehensive range of logistics and supply chain solutions, leveraging their global networks and advanced technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Government Regulations and Initiatives

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Technological Trends in the Industry

- 4.5 Spotlight - Effect of E-commerce on Traditional Automotive Logistics Supply Chain

- 4.6 Insights into Automotive Aftermarket and its Logistics Activities

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Environmental Concerns and Regulations

- 5.1.2 Technological Advancements in Automotive Technology

- 5.2 Market Restraints

- 5.2.1 Economic Uncertainty

- 5.3 Market Opportunities

- 5.3.1 Electric Vehicle Adoption

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Transportation

- 6.1.2 Warehousing, Distribution and Inventory Management

- 6.1.3 Other Services

- 6.2 By Type

- 6.2.1 Finished Vehicle

- 6.2.2 Auto Components

- 6.2.3 Other types

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

- 6.3.3 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 CEVA Logistics AG

- 7.2.2 DB Schenker

- 7.2.3 DHL

- 7.2.4 DSV

- 7.2.5 GEODIS

- 7.2.6 KUEHNE + NAGEL International AG

- 7.2.7 Nippon Express Co. Ltd

- 7.2.8 Ryder System Inc.

- 7.2.9 XPO Logistics Inc.

- 7.2.10 United Parcel Service Inc.*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 GDP Distribution, by Activity

- 9.2 Insights into Capital Flows

- 9.3 Economic Statistics-Transport and Storage Sector, Contribution to Economy