中国の自動車物流:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

China Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644873

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

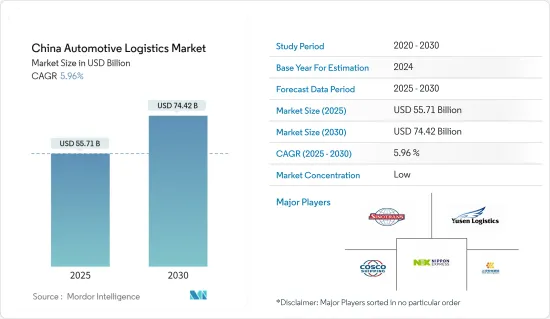

中国の自動車物流の市場規模は2025年に557億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.96%で、2030年には744億2,000万米ドルに達すると予測されます。

主なハイライト

- 中国の自動車産業は大きな転換期を迎えており、これを受けて中国政府は自動車消費を活性化させる施策を実施しています。こうした措置には、財政・税制面での支援、旧式ディーゼルトラックの廃止加速、中古車取引チャネルの最適化などが含まれます。さらに、政府は新エネルギー車への補助金を導入し、自動車部門を支援するためにインフラ開発に投資しており、こうした取り組みが市場を浮揚させると思われます。

- 中国は依然として世界最大の自動車市場であり、年間販売台数、生産台数ともにトップです。予測では、国内生産台数は2025年までに3,500万台に達します。さらに、電気自動車に対する世界の関心の高まりに後押しされ、中国の自動車販売は海外で顕著な伸びを見せています。10月、中国の製造業に改善の兆しが現れ、Caixin China General Manufacturing Purchasing Managers'Index(PMI)が1ポイント上昇し、50.3に達したことが強調された、とGlobal Timesが報じた。

- 電気自動車市場の急速な成長は、この産業の軌道において極めて重要な役割を果たしています。電気自動車の分野で圧倒的な地位を占める中国は、自動車輸出の顕著な増加を記録しています。倉庫施設や専用輸送路の整備など、物流インフラの強化が功を奏しています。電気自動車メーカーへの補助金や充電インフラへの投資など、政府の支援政策がこの成長をさらに後押ししています。

- 車両輸送と部品取り扱いの複雑さを乗り切るため、企業はますますAIとIoT技術に目を向け、ロジスティクスの最適化と効率性の向上を目指しています。例えば、2024年初頭から、最大手自動車メーカーの1つであるSAIC Motor Corporationは、IoTセンサーとAIアルゴリズムを統合した自動倉庫システムを展開しました。その結果、AIとIoTの統合は業界の標準的な慣行となりつつあり、さらなる進歩を促し、効率性と信頼性の新たなベンチマークを設定しています。

- このような自動車セクターの成長、自動車販売の増加、輸出の増加が、同国の自動車物流市場を牽引すると予想されます。

中国の自動車物流市場の動向

中国のNEV(新エネルギー車)への投資が市場成長を牽引

2024年J.D. Power中国新エネルギー車-自動車性能・実行・レイアウト(NEV-APEAL)調査は、自動車物流市場における極めて重要な動向、すなわち中国における新エネルギー車(NEV)の着実な上昇を強調しています。中国のNEVのNEV-APEAL平均スコアは1000点満点中789点で、2023年から13ポイント上昇しました。この一貫した上昇傾向は、NEVに対する消費者の受容と満足度の高まりを示すものであり、その結果、合理化されたロジスティクス・ソリューションに対する需要に拍車をかけています。

NEVセクターの急速な成長は、バッテリー・セクターに顕著な焦点を当てながら、関連する産業チェーンを再構築しています。パワー・バッテリーは、自動車のバッテリー寿命、安全性、総コストを左右する極めて重要な役割を担っています。中国メーカーはリン酸鉄リチウム(LFP)バッテリーを明確に好み、リチウム・ニッケル・マンガン・コバルト(NMC)バッテリーに傾倒する欧米市場とは一線を画しています。2024年4月までに、新型乗用車の小売普及率は50%を超えます。この変化は、市場におけるNEVの急成長ぶりを浮き彫りにするだけでなく、NEVの流通を促進するための専門的な物流サービスに対する需要の高まりを際立たせています。

NEV市場の急成長は、自動車物流の領域で、カスタマイズされた輸送・ハンドリングサービスの需要を増幅させています。この急増する需要は、単にサプライチェーンを拡大するだけでなく、インフラ開発を促進し、持続可能なロジスティクスの実践を促進しています。ロジスティクス企業がこうした進化する需要に対応するために軸足を移すことで、新たな収益の流れが開けると同時に、中国の自動車事情変革において極めて重要な役割を果たしています。

結論として、中国におけるNEVの急速な進歩は、物流市場を再形成しているだけでなく、自動車セクターにも大きな変化をもたらしています。消費者受容の高まりと持続可能な慣行へのシフトは、ロジスティクス企業に課題と機会の両方をもたらし、最終的には自動車エコシステム全体の進化に貢献しています。

倉庫部門が市場の成長を促進

さまざまなサービス分野が市場の成長を後押ししています。中国の自動車産業の拡大に伴い、倉庫部門はサプライチェーン全体において極めて重要な存在となっています。商品量の増加に対応するため、各企業は倉庫容量の拡大に大規模な投資を行っています。

さらに、eコマースの台頭と自動車生産の増加に伴い、自動車メーカーは変動する在庫レベルを管理するための堅牢な倉庫ソリューションを求めています。例えば、郵船ロジスティクスは2024年に中国での倉庫業務を拡大し、自動保管・検索システムを統合して在庫管理を強化し、処理時間を最小化しました。

さらに、リアルタイムの在庫監視のためにIoT技術を活用した先進的な在庫管理システムの導入が進んでいます。例えば、COSCO Shippingはスマート在庫管理ソリューションを導入し、ネットワーク全体で自動車部品の正確な追跡を可能にしています。

結論として、中国の自動車産業の成長は、輸送、倉庫管理、在庫管理サービスの進歩によって大きく牽引されています。こうした技術革新は、市場における効率性と信頼性に対する需要の高まりに応える上で不可欠です。

中国の自動車物流業界の概要

中国の自動車物流市場は非常に細分化され競合が激しく、国際的な企業とは別に、国内の自動車物流企業が複数存在しています。DHLや日本通運のような国際企業と、上海汽車安吉物流や郵船ロジスティクスのような地場企業が競合しています。また、中国遠洋海運(集団)有限公司(COSCO)、HYCXグループ、Sinotrans Limitedなど、他の多くのプレーヤーもいます。

自動車部門のプレーヤーは、最先端技術を統合することによって、多様なサービスを仕立てています。例えば、最近では2024年に深センがAIを統合した工場を建設し、あらゆる製造業のバックボーンであるサプライ・チェーンが大きな変革を遂げました。高度な分析の助けを借りて、これらの工場は現在、原材料のニーズを正確に予測し、在庫レベルを最適化し、タイムリーな調達を保証することができます。これにより、保有コストを最小限に抑えるだけでなく、無駄も削減できます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 現在の市場シナリオ

- 市場促進要因

- 新エネルギー自動車販売の成長

- 政府の取り組みと支援

- 市場抑制要因

- 中国と米国の貿易戦争

- サプライチェーンの混乱

- 市場機会

- デジタル変革

- 新興市場への進出

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

- 政府の規制と取り組み

- 中国自動車産業の概要(概要、開発動向、統計など)

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- タイプ別

- 完成車

- 自動車部品

- サービス別

- 輸送

- 倉庫、流通、在庫管理

- その他のサービス

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- China Ocean Shipping(Group)Company

- SAIC Anji Logistics

- BLG Logistics

- HYCX Group

- Yusen Logistics Co. Ltd

- DHL

- Nippon Express

- GEODIS

- Sinotrans Co. Ltd

- DHL Supply Chain

- Apex Group*

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標(活動別GDP分布、運輸・倉庫部門-経済への貢献など)

- 貿易統計輸出入統計

- 自動車セクターに関連する対外貿易統計

目次

The China Automotive Logistics Market size is estimated at USD 55.71 billion in 2025, and is expected to reach USD 74.42 billion by 2030, at a CAGR of 5.96% during the forecast period (2025-2030).

Key Highlights

- China's automotive industry underwent substantial shifts which in response, the Chinese government has implemented measures to rejuvenate automobile consumption. These measures include providing fiscal and taxation support, accelerating the elimination of obsolete diesel trucks, and optimizing second-hand vehicle trading channels. Additionally, the government has introduced subsidies for new energy vehicles and invested in infrastructure development to support the automotive sector, such initiatives will keep the market afloat.

- China remains the world's largest vehicle market, leading in both annual sales and manufacturing output. Projections indicate that domestic production will hit 35 million vehicles by 2025. Furthermore, bolstered by a global surge in interest for electric vehicles, Chinese automobile sales overseas have seen notable growth. In October, signs of improvement emerged in China's manufacturing sector, highlighted by a 1 percentage point uptick in the Caixin China General Manufacturing Purchasing Managers' Index (PMI), reaching 50.3, as reported by Global Times.

- The swift growth of the electric vehicle market plays a pivotal role in this industry's trajectory. With its dominant stance in the electric vehicle arena, China has recorded a pronounced uptick in vehicle exports. Enhancements in logistics infrastructure, marked by upgraded warehouse facilities and specialized transport corridors, have been instrumental. The government's supportive policies, which include subsidies for electric vehicle manufacturers and investments in charging infrastructure, have further fueled this growth.

- To navigate the complexities of vehicle transportation and parts handling, companies are increasingly turning to AI and IoT technologies, aiming to optimize logistics and boost efficiency. For instance, from the begining of 2024, SAIC Motor Corporation, one of the largest automotive manufacturers, has rolled out an automated warehousing system integrated with IoT sensors and AI algorithms. As a result, the integration of AI and IoT is becoming a standard practice in the industry, driving further advancements and setting new benchmarks for efficiency and reliability.

- This growing automotive sector, increasing vehicle sales, and exports are expected to drive the country's automotive logistics market.

China Automotive Logistics Market Trends

Chinese Investment in NEVs (New Energy Vehicles) Driving the Market Growth

The 2024 J.D. Power China New Energy Vehicle - Automotive Performance, Execution and Layout (NEV-APEAL) Study underscores a pivotal trend in the automotive logistics market: the steady ascent of New Energy Vehicles (NEVs) in China. Chinese NEVs have achieved an average NEV-APEAL score of 789 out of 1000, marking a notable 13-point rise from 2023. This consistent upward trend signals an increasing consumer acceptance and satisfaction with NEVs, subsequently fueling the demand for streamlined logistics solutions.

The swift growth of the NEV sector is reshaping associated industrial chains, with a pronounced focus on the battery sector. Power batteries play a pivotal role in influencing a vehicle's battery life, safety, and overall cost. Chinese manufacturers have shown a clear preference for lithium Iron Phosphate (LFP) batteries, setting themselves apart from the Western markets that lean towards Lithium Nickel Manganese Cobalt (NMC) batteries. By April 2024, new passenger cars achieved a retail penetration rate exceeding 50%, a milestone previously held by traditional petrol vehicles. This shift not only highlights the burgeoning dominance of NEVs in the market but also accentuates the escalating demand for specialized logistics services to facilitate their distribution.

The surging NEV market is amplifying the demand for customized transport and handling services within the automotive logistics domain. This burgeoning demand is not just expanding the supply chain but is also catalyzing infrastructure development and promoting sustainable logistics practices. As logistics firms pivot to address these evolving demands, they unlock fresh revenue streams, simultaneously playing a pivotal role in the transformation of China's automotive landscape.

In conclusion, the rapid advancement of NEVs in China is not only reshaping the logistics market but also driving significant changes in the automotive sector. The increasing consumer acceptance and the shift towards sustainable practices present both challenges and opportunities for logistics companies, ultimately contributing to the evolution of the entire automotive ecosystem.

Warehousing Segment Fuels Growth in the Market

Various service segments are fueling market growth. With the expansion of China's automotive industry, the warehouse segment has become pivotal in the overall supply chain. In response to increasing goods volumes, companies are significantly investing in expanding their warehouse capacities.

Moreover, with the rise of e-commerce and increased vehicle production, automotive manufacturers are seeking robust warehousing solutions to manage fluctuating inventory levels. For example, in 2024, Yusen Logistics expanded its warehousing operations in China, integrating automated storage and retrieval systems to enhance inventory management and minimize handling times.

Furthermore, there's a growing adoption of advanced inventory management systems leveraging IoT technology for real-time stock monitoring. For instance, COSCO Shipping has deployed smart inventory management solutions, enabling precise tracking of automotive components throughout its network.

In conclusion, the growth of China's automotive industry is significantly driven by advancements in transportation, warehousing, and inventory management services. These innovations are essential in meeting the increasing demands for efficiency and reliability in the market.

China Automotive Logistics Industry Overview

The Chinese automotive logistics market is highly fragmented and competitive, with the presence of several local automotive logistics companies in the country apart from international firms. International players like DHL and Nippon Express compete with local players like SAIC Anji Logistics and Yusen Logistics. And many other players including China Ocean Shipping (Group) Company (COSCO), HYCX Group, Sinotrans Limited, etc.

Players in the automotive sector are tailoring a diverse array of services by integrating cutting-edge technologies. For instance, Recently in 2024, Shenzhen's updtaed with AI-integrated factories, the supply chain - the backbone of any manufacturing setup - has undergone a significant transformation. With the help of advanced analytics, these factories can now accurately predict raw material needs, optimize inventory levels, and ensure timely procurement. This not only minimizes holding costs but also reduces wastage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Drivers

- 4.2.1 Growing New Energy Vehicles Sales

- 4.2.2 Government Initiatives and Support

- 4.3 Market Restraints

- 4.3.1 Trade War between China and the United States

- 4.3.2 Supply Chain Disruptions

- 4.4 Market Opportunities

- 4.4.1 Digital Transformation

- 4.4.2 Expansion into Emerging Markets

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Industry Value Chain Analysis

- 4.7 Government Regulations and Initiatives

- 4.8 Overview of China's Automotive Industry (Overview, Development and Trends, Statistics, etc.)

- 4.9 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Finished Vehicle

- 5.1.2 Auto Component

- 5.2 By Service

- 5.2.1 Transportation

- 5.2.2 Warehousing, Distribution, and Inventory Management

- 5.2.3 Other Services

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 China Ocean Shipping (Group) Company

- 6.2.2 SAIC Anji Logistics

- 6.2.3 BLG Logistics

- 6.2.4 HYCX Group

- 6.2.5 Yusen Logistics Co. Ltd

- 6.2.6 DHL

- 6.2.7 Nippon Express

- 6.2.8 GEODIS

- 6.2.9 Sinotrans Co. Ltd

- 6.2.10 DHL Supply Chain

- 6.2.11 Apex Group*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution by Activity, Transport and Storage Sector-contribution to Economy, etc.)

- 8.2 Trade Statistics: Imports and Exports

- 8.3 External Trade Statistics related to the Automotive Sector

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日