|

市場調査レポート

商品コード

1644849

米国の自動車ロジスティクス:市場シェア分析、産業動向、成長予測(2025~2030年)United States Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の自動車ロジスティクス:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

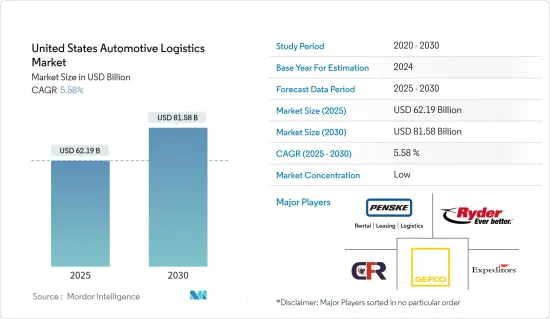

米国の自動車ロジスティクス市場規模は2025年に621億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.58%で、2030年には815億8,000万米ドルに達すると予測されます。

米国の自動車市場は電気自動車部門が牽引しており、軽自動車が米国市場を独占しています。

米国の自動車産業は、昨年の2020年3月にCOVID-19が発生したため、急激な需要減退に見舞われました。これは自動車サプライチェーンロジスティクス産業全体に影響を与えました。米国の自動車販売台数は前年比38%減となりました。

封鎖規制が解除され市場が開放された後、軽自動車部門は立ち直り、今年度の販売台数は約1,384万台に達しました。米国で販売された自動車のうち、軽自動車だけで約97%を占めました。パンデミック後、市場が立ち直ったことで、米国の自動車ロジスティクス産業は輸出入ともに大きな成長を遂げると予想されます。

米国は世界第2位の自動車市場と自動車産業であり、第1位は中国です。このセグメントは米国の輸出入において重要な役割を果たしています。米国は世界第2位の自動車メーカーであり、150万台以上の自動車と760万台以上の商用車を生産しています。米国は、この地域で最も有望かつ急成長している自動車市場のひとつです。米国の自動車産業は、研究開発努力、労働力の確保、政府支援、地理的優位性など複数の要因によって支えられています。

米国の自動車ロジスティクス市場動向

米国で成長する電気自動車部門

産業団体によると、米国の自動車販売台数の約5.7%が完全電気自動車で、2021年の3.2%から2022年には増加します。同地域のバッテリー電気自動車販売台数は、世界のプラグイン電気自動車販売台数全体の8%強を占めます。Teslaは米国のEV市場を独占し続けており、米国での電気自動車販売台数は推定30万2,000台です。しかし、競合は勢いを増し始めており、General Motorsなどのメーカーは、提供する車種に新しいEVモデルを追加し続けています。シボレーのボルトは、電気自動車のベストセラー・モデル一覧に入った。その年の販売台数は、同モデルが発売された年の販売台数をわずかに下回り、第2位を記録しました。General Motorsは2035年までにゼロ・エミッション車のみを販売する意向であり、すでに世界のプラグインEV市場をリードしていました。

Teslaは同地域のプラグインEV市場を独占していたが、Volkswagen Groupも僅差で追随していました。全体として、メーカーは研究開発費を増やそうとしており、その中でも電気モビリティは投資の最前線にあった。これは、米国政府が2030年までに全自動車販売台数の半分をゼロ・エミッションにするという公約を掲げていることも一因となっています。

米国市場を独占する軽自動車

2022年、米国の自動車産業は約1,384万台の軽自動車を販売しました。この数字には、約290万台の自動車小売販売台数と1,090万台弱の小型トラック販売台数が含まれます。小型車が米国市場を席巻しているのは、その実用性と燃費の良さで人気があり、消費者にとって経済的な選択肢となっているからです。小型商用車の需要増加に伴い、メキシコ-米国間の短海輸送量の増加が観察されており、米国-メキシコ-カナダ協定(USMCA)の締結により自動車ロジスティクスセグメントの成長が予測されています。産業団体によると、軽自動車の満足度について尋ねたところ、米国の消費者はHonda、Lexus、BMWのモデルに最も満足していました。Lexusは、100台あたり報告された問題数から、最も信頼できるブランドの一つでした。

米国の自動車ロジスティクス産業概要

米国の自動車ロジスティクス市場は非常に細分化され、競争が激しく、国内外に大手企業が進出しています。Expeditors International of Washington Inc.、DHL、GEFCO、Nippon Expressなどの国際的参入企業は、CFR Rinkens、Ryder System Inc.、Penske Logisticsなどの国内大手と競合しています。国内と国際レベルでの電気自動車需要の増加、軽量車両の需要増加、その他市場に影響を与える要因により、市場は成長すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場力学

- 促進要因

- eコマースとオンライン販売の成長

- 軽自動車生産による需要

- 抑制要因

- 燃料価格の変動

- 熟練労働者の不足

- 機会

- アディティブ・マニュファクチャリング

- コネクテッドカーと自律走行車の需要の高まり

- 促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 政府の規制と取り組み

- COVID-19の市場への影響

第5章 市場セグメンテーション

- タイプ別

- 完成車

- 自動車部品

- その他

- サービス別

- 輸送

- 倉庫業

- 流通・在庫管理

- その他

第6章 競合情勢

- 企業プロファイル

- Expeditors International of Washington Inc.

- CFR Rinkens

- Ryder System Inc.

- GEFCO

- Penske Logistics

- US Auto Logistics

- DHL

- Nippon Express

- J.B. Hunt Transport Services Inc.

- C.H Robinson Worldwide*

第7章 市場の将来

第8章 付録

- マクロ経済指標(活動別GDP分布、輸送・貯蔵部門-経済への貢献など)

- 貿易統計輸出入統計

- 自動車セクターに関連する対外貿易統計

The United States Automotive Logistics Market size is estimated at USD 62.19 billion in 2025, and is expected to reach USD 81.58 billion by 2030, at a CAGR of 5.58% during the forecast period (2025-2030).

The US automotive market is driven by the electric vehicle sector, and light vehicles dominate the US market.

The automotive industry in the United States experienced a sharp decline in demand because of the COVID-19 outbreak last year in March 2020. This impacted the entire automotive supply chain logistics industry. The US vehicle sales were down by 38% year-on-year.

After the lockdown restrictions were lifted and the market was opened, the light vehicle segment sector bounced back to reach some 13.84 million units of sales in the current year. Light vehicles alone accounted for about 97% of the motor vehicles that were sold in the United States. Post-pandemic and with the market bouncing back, the United States automotive logistics industry is anticipated to see huge growth in both imports and exports.

The United States is the world's second-biggest auto market and automotive industry, the first being China. This sector plays an important role in US imports and exports. The country is the second-largest automaker in the world, manufacturing more than 1.5 million cars and 7.6 million commercial vehicles. The United States is one of the most promising and fastest-growing automobile markets in the region. The United States automobile industry is supported by multiple factors such as R&D efforts, labor availability, government support, and geographic advantages.

U.S. Automotive Logistics Market Trends

Electric Vehicle Sector growing in the United States

According to an industry association, approximately 5.7% of US car sales were fully electric in 2022, up from 3.2% in 2021. The battery electric vehicle sales in the region made up just over eight percent of the total plug-in electric vehicle sales worldwide. Tesla continues to dominate the US EV market, with an estimated 302,000 electric vehicles sold in the United States. However, competition is beginning to gain momentum, and manufacturers such as General Motors are continuing to add new EV models into their range of vehicles offered. Chevrolet's Bolt made it into the list of best-selling electric vehicle models. The model recorded its second-largest sales volume that year, just under its sales-the year the model launched. General Motors intends to sell only zero-emission vehicles by 2035 and was already one of the global plug-in EV market leaders.

While Tesla dominated the plug-in electric vehicle market in the region, it was also followed closely by the Volkswagen Group, whose worldwide electric vehicle sales soared that same year. Overall, manufacturers were looking to increase their research and development expenditure, with electric mobility at the forefront of their investments. This was in part motivated by the US Government's commitment to zero-emission for half of all vehicle sales by 2030.

Light Vehicles dominating the US Market

In 2022, the auto industry in the United States sold approximately 13.84 million light vehicle units. This figure includes retail sales of about 2.9 million autos and just under 10.9 million light truck units. Light-duty vehicles dominate the US market because they are popular for their utility and better fuel economy, which makes them an economical choice for consumers. With the increase in demand for light commercial vehicles, growth in short-sea volumes between Mexico and the US is being observed, which is forecasted to grow the automotive logistics sector with the signing of the US-Mexico-Canada Agreement (USMCA). According to an industry association, when asked about light vehicle satisfaction, consumers in the United States were most satisfied with Honda, Lexus, and BMW models. Lexus was among the most dependable brands based on the number of problems reported per 100 vehicles.

U.S. Automotive Logistics Industry Overview

The US automotive logistics market is highly fragmented and competitive, with the presence of big international and domestic firms in the country. International players like Expeditors International of Washington Inc., DHL, GEFCO, and Nippon Express compete with local giants like CFR Rinkens, Ryder System Inc., and Penske Logistics. The market is expected to grow because of the growing demand for electric vehicles at the domestic and international levels, an increase in the demand for lightweight vehicles, and other factors influencing the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Growth of E-commerce and Online Sales

- 4.2.1.2 Demand from Light Vehicle Production

- 4.2.2 Restraints

- 4.2.2.1 Fluctuating fuel prices

- 4.2.2.2 Shortage of skilled workforce

- 4.2.3 Opportunities

- 4.2.3.1 Additive Manufacturing

- 4.2.3.2 Rising demand for Connected and Autonomous vehicles

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Government Regulations and Initiatives

- 4.5 Impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Finished Vehicle

- 5.1.2 Auto Component

- 5.1.3 Other Types

- 5.2 By Service

- 5.2.1 Transportation

- 5.2.2 Warehousing

- 5.2.3 Distribution and Inventory Management

- 5.2.4 Other Services

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration Analysis and Major Player)

- 6.2 Company Profiles

- 6.2.1 Expeditors International of Washington Inc.

- 6.2.2 CFR Rinkens

- 6.2.3 Ryder System Inc.

- 6.2.4 GEFCO

- 6.2.5 Penske Logistics

- 6.2.6 US Auto Logistics

- 6.2.7 DHL

- 6.2.8 Nippon Express

- 6.2.9 J.B. Hunt Transport Services Inc.

- 6.2.10 C.H Robinson Worldwide*

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution by Activity, Transport and Storage Sector-contribution to Economy, etc.)

- 8.2 Trade Statistics: Imports and Exports

- 8.3 External Trade Statistics related to the Automotive Sector