|

市場調査レポート

商品コード

1910814

高帯域幅メモリ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)High Bandwidth Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 高帯域幅メモリ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

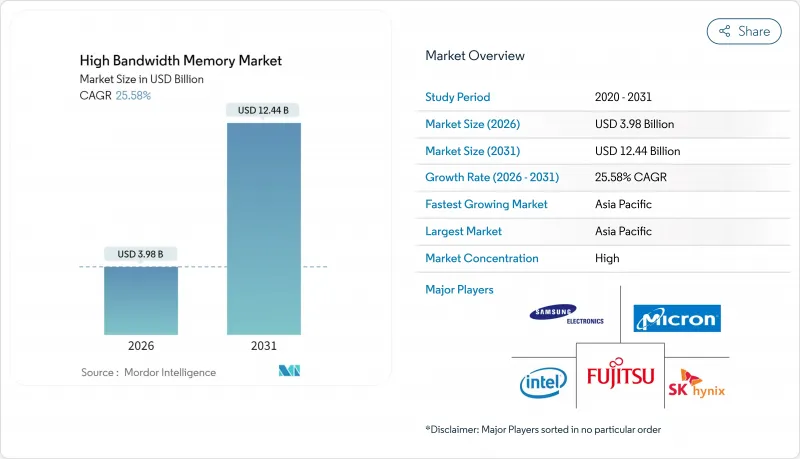

高帯域幅メモリ市場は、2025年の31億7,000万米ドルから2026年には39億8,000万米ドルへ成長し、2026年から2031年にかけてCAGR25.58%で推移し、2031年までに124億4,000万米ドルに達すると予測されています。

2025年には、AI最適化サーバーへの持続的な需要、DDR5の普及拡大、ハイパースケーラーによる積極的な投資が相まって、半導体バリューチェーン全体での生産能力拡大が加速しました。過去1年間、サプライヤーはTSVの歩留まり向上に注力する一方、パッケージングパートナーは基板不足を緩和するため新たなCoWoSラインへの投資を進めました。自動車メーカーは、レベル3およびレベル4の自動運転プラットフォーム向けにISO 26262認証取得済みHBMを確保するため、メモリベンダーとの連携を強化しました。アジア太平洋地域の製造エコシステムは、韓国メーカーが次世代HBM4E量産化に向け数十億米ドル規模の投資を約束したことで、生産面での主導権を維持しました。

世界の高帯域幅メモリ市場の動向と洞察

AIサーバーの普及とGPU接続率

大規模言語モデルの急速な成長により、2024年には従来のHPCデバイスと比較してGPUあたりのHBM要件が7倍に増加しました。NVIDIAのH100は80GBのHBM3を搭載し3.35TB/sを実現、一方H200は2025年初頭に141GBのHBM3Eを搭載し4.8TB/sでサンプル提供されました。受注残により2026年までサプライヤーの生産能力の大半が確保されたため、データセンター運営者は在庫の事前購入やパッケージングラインへの共同投資を余儀なくされています。

データセンターのDDR5および2.5-Dパッケージングへの移行

ハイパースケーラー企業は、ワット当たりの性能を50%向上させるため、ワークロードをDDR4からDDR5へ移行させると同時に、AIアクセラレータとシリコンインターポーザ上の積層メモリを接続する2.5-D統合技術を採用しました。基板不足により2024年を通じてGPUの発売が遅れた際、単一のパッケージングプラットフォームへの依存がサプライチェーンリスクを高めました。

12層スタックを超えるTSV歩留まり低下

16層HBMスタックでは、熱サイクルによるTSV内部の銅移動故障が発生し、歩留まりが70%を下回りました。メーカーは信頼性安定化のため、熱対応TSV設計や新規誘電体材料を追求していますが、商用化にはあと2年を要する見込みです。

セグメント分析

サーバーカテゴリーは、2025年に高帯域幅メモリ市場の67.80%の収益シェアを占め、ハイパースケール事業者が8~12個のHBMスタックを統合したAIサーバーへ移行したことを反映し、市場を牽引しました。クラウドプロバイダーがGPUあたり3TB/s超の帯域幅を必要とする基盤モデルサービスを開始したことで需要が加速しました。2025年のエネルギー効率目標では、ディスクリートソリューションよりも優れた性能/ワットを実現する積層DRAMが優位となり、データセンター事業者が電力枠内に収まることを可能にしました。企業向けリフレッシュサイクルが始動し、DDR4ベースのノードをHBM対応アクセラレータに置き換える動きが2027年まで購入契約を延長しています。

自動車・輸送セグメントは現在規模こそ小さいもの、2031年までCAGR34.18%と最も高い成長率を記録すると予測されています。チップメーカーはティア1サプライヤーと連携し、ASIL D要件を満たす機能安全機能を組み込みました。欧州および北米におけるレベル3生産プログラムは2024年末に限定的な展開を開始し、各車両は従来データセンター推論クラスター専用だったメモリ帯域幅を活用しています。無線更新戦略の成熟に伴い、自動車メーカーは車両をエッジサーバーとして扱うようになり、HBM搭載率をさらに支えています。

HBM3はAIトレーニングGPUでの普及拡大を受け、2025年には売上高の45.70%を占めました。HBM3Eのサンプル出荷は2024年第1四半期に開始され、第一波の生産では9.2Gb/sを超えるピン速度で稼働しました。性能向上によりスタックあたり1.2TB/sを達成し、目標帯域幅に必要なスタック数を削減するとともに、パッケージの熱密度を低減しました。

HBM3Eの予測CAGR40.90%は、2025年半ばに量産を開始したマイクロンの36GB・12ハイ製品によって支えられており、最大5,200億パラメータのモデルサイズを持つアクセラレータをターゲットとしています。今後の展望として、2025年4月に公開されたHBM4規格では、スタックあたりのチャネル数が倍増し、総スループットが2TB/sに向上し、マルチペタフロップス級のAIプロセッサの基盤が整います。

高帯域幅メモリ(HBM)市場は、用途別(サーバー、ネットワーク、高性能コンピューティング、民生用電子機器など)、技術別(HBM2、HBM2E、HBM3、HBM3E、HBM4)、スタックあたりのメモリ容量別(4GB、8GB、16 GB、24 GB、32 GB以上)、プロセッサインターフェース(GPU、CPU、AIアクセラレータ/ASIC、FPGAなど)、地域(北米、南米、欧州、アジア太平洋、中東・アフリカ)によって区分されます。

地域別分析

アジア太平洋地域は2025年の収益の41.00%を占め、韓国が中核をなしています。韓国ではSKハイニックスとサムスンが生産ラインの80%以上を支配しています。2024年に発表された政府の優遇措置により、2027年の稼働を予定する拡張製造クラスターが支援されました。台湾のTSMCは最先端CoWoSのパッケージングにおける独占を維持しており、メモリの供給を現地の基板供給に依存させることで、地域的な集中リスクを生み出しています。

北米のシェアは、マイクロン社がCHIPS法による61億米ドルの資金調達を確保し、ニューヨーク州とアイダホ州に先進DRAM工場を建設したことで拡大しました。パイロット生産のHBMは2026年初頭開始が見込まれています。ハイパースケーラーの設備投資が現地需要を牽引し続けていますが、ほとんどのウエハーは依然としてアジアで加工された後、米国で最終モジュール組立が行われています。

欧州は自動車需要を起点に市場参入。ドイツの自動車メーカー各社は、2024年末出荷予定のレベル3運転支援システム向けHBMの認定を完了しました。EUの半導体戦略は研究開発中心の姿勢を維持し、将来の高帯域メモリ市場拡大の鍵となるフォトニック相互接続やニューロモーフィック研究を重視しました。中東・アフリカ地域は導入初期段階に留まりましたが、2025年に開始された国家主導のAIデータセンタープロジェクトは、地域需要の増加を示唆しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- AIサーバーの普及とGPU搭載率

- データセンターのDDR5および2.5-Dパッケージングへの移行

- 自動車用ADASにおけるエッジAI推論

- ハイパースケーラーにおけるシリコンインターポーザースタックの選好

- 地域別メモリ生産補助金(韓国、米国、日本)

- フォトニクス対応HBMロードマップ(HBM-P)

- 市場抑制要因

- 12層スタックを超えるTSV歩留まり損失

- 限定的なCoWoS/SoIC先進パッケージング能力

- 1TB/s超の帯域幅デバイスにおけるサーマルスロットリング

- AIアクセラレータに対する地政学的輸出規制

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- DRAM市場分析

- DRAM収益と予測

- 地域別DRAM収益

- DDR5製品の現行価格

- DDR5製品メーカー一覧

- マクロ経済要因の影響

第5章 市場規模と成長予測

- 用途別

- サーバー

- ネットワーク

- 高性能コンピューティング

- 民生用電子機器

- 自動車および輸送機器

- 技術別

- HBM2

- HBM2E

- HBM3

- HBM3E

- HBM4

- メモリ容量別(スタックあたり)

- 4 GB

- 8 GB

- 16 GB

- 24 GB

- 32 GB以上

- プロセッサインターフェース別

- GPU

- CPU

- AIアクセラレータ/ASIC

- FPGA

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- その他南米

- 欧州

- ドイツ

- フランス

- 英国

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- Micron Technology, Inc.

- Intel Corporation

- Advanced Micro Devices, Inc.

- Nvidia Corporation

- Taiwan Semiconductor Manufacturing Company Limited

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- Powertech Technology Inc.

- United Microelectronics Corporation

- GlobalFoundries Inc.

- Applied Materials Inc.

- Marvell Technology, Inc.

- Rambus Inc.

- Cadence Design Systems, Inc.

- Synopsys, Inc.

- Siliconware Precision Industries Co., Ltd.

- JCET Group Co., Ltd.

- Chipbond Technology Corporation

- Cadence Design Systems Inc.

- Broadcom Inc.

- Celestial AI

- ASE-SPIL(Silicon Products)

- Graphcore Limited