|

市場調査レポート

商品コード

1721494

高帯域幅メモリ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測High Bandwidth Memory Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 高帯域幅メモリ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月04日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

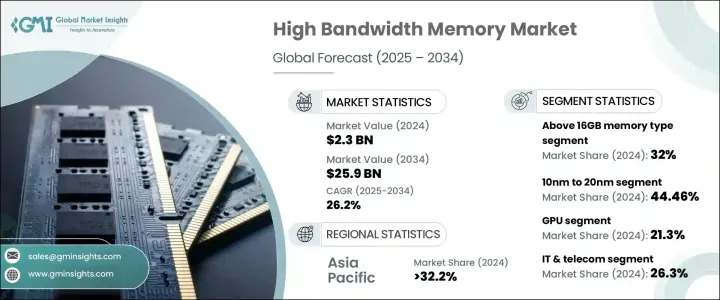

高帯域幅メモリの世界市場規模は、2024年に23億米ドルとなり、CAGR 26.2%で成長し、2034年には259億米ドルに達すると予測されています。

データ中心技術への世界のシフトは、メモリソリューションの展望を再形成しており、より高速なデータ処理とエネルギー効率の高いコンピューティングを実現する重要な手段として、情勢が浮上しています。さまざまな分野の企業が次世代技術の採用にしのぎを削る中、高速で低レイテンシのメモリに対する需要が顕著に急増しています。

人工知能(AI)、機械学習(ML)、ADAS(先進運転支援システム)、5Gネットワークの影響力の高まりは、強力なメモリ技術への需要を引き続き促進しています。企業は、ビッグデータ、高解像度画像、リアルタイム分析、ディープラーニングのワークロードをサポートするために、HBMに大きく依存しています。自動車、ヘルスケア、金融サービス、メディアなどの分野でデジタルトランスフォーメーションが加速する中、HBMソリューションは、よりスマートで、より高速な、より接続性の高いシステムの開発において、急速に基盤となりつつあります。世界中の企業は、この急速に進化する領域で競争力を維持するため、最先端のイノベーションへの投資と製造能力の拡大によって対応しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 23億米ドル |

| 予測金額 | 259億米ドル |

| CAGR | 26.2% |

市場は技術ノード別に10nm未満、10nm~20nm、20nm以上に区分されます。10nm~20nmのカテゴリーは2024年に10億米ドルを占め、2025年から2034年にかけてCAGR 26.7%で成長すると予測されています。このノードは、車載用電子機器、IoT機器、ミッドレンジの消費者向け製品など、バランスの取れた性能とコスト効率を必要とするアプリケーションに最適であることが証明されています。そのスケーラビリティは、高歩留まり生産と信頼性の高い熱管理と相まって、製造コストを高騰させることなく性能の最適化を目指す開発者にとっての有力な選択肢であり続けています。

高帯域幅メモリ市場は、用途別にGPU、CPU、FPGA、ASIC、AI、ML、HPC、ネットワーキング、データセンターに分類されます。GPUセグメントは2024年に21.3%のシェアを獲得し、プロフェッショナルおよび没入型ゲームのエコシステムにおける需要急増に支えられています。超高精細グラフィックス、リアルタイムレンダリング、拡張現実環境が主流になるにつれ、グラフィックスプロセッシングユニットは、帯域幅ニーズの高まりに対応するため、HBM3Eなどの高度なHBM技術を統合しています。この動向は、高速リフレッシュレートと応答性の高いユーザー体験が不可欠なゲーミングとアニメーションの分野で特に顕著です。

アジア太平洋地域は、2024年に32.2%のシェアで世界市場をリードしました。一方、米国の高帯域幅メモリ市場は、クラウドとデータセンター・インフラのデジタル近代化が牽引し、同年の市場規模は5億2,300万米ドルとなりました。同国には膨大な数のデータセンターがあるため、HBMの採用において圧倒的な力を持っており、リアルタイムのデータ分析やエッジコンピューティング・アプリケーションが導入加速への道を開いています。

世界の高帯域幅メモリ市場の主要企業には、Cadence Design Systems, Inc.、Advanced Micro Devices, Inc.(AMD)、Broadcom Inc.、GlobalFoundries Inc.、IBM Corporation、富士通株式会社、Infineon Technologies AGなどがあります。これらの企業は、HBM製品の速度、拡張性、効率を高めるために研究開発に多額の投資を行っています。AI、ゲーム、半導体の各分野にわたる戦略的提携は、世界の拡大努力をさらに後押ししています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- ベンダーマトリックス

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 業界への影響要因

- 促進要因

- データ集約型アプリケーションの拡張

- 高性能コンピューティングの成長

- 次世代プラットフォーム統合

- ゲームとグラフィックスの需要の高まり

- データセンターとクラウドサービスの拡張

- 業界の潜在的リスク&課題

- 高い生産コスト

- 技術統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

- 将来の市場動向

- 規制情勢

第4章 市場推計・予測:メモリ容量別、2021 –2034

- 主要動向

- 4GB未満

- 4GBから8GB

- 8GBから16GB

- 16GB以上

第5章 市場推計・予測:テクノロジーノード別、2021 –2034

- 主要動向

- 10nm以下

- 10nmから20nm

第6章 市場推計・予測:用途別、2021 –2034

- 主要動向

- グラフィックスプロセッシングユニット(GPU)

- 中央処理装置(CPU)

- フィールドプログラマブルゲートアレイ(FPGA)

- 特定用途向け集積回路(ASIC)

- 人工知能(AI)と機械学習(ML)

- 高性能コンピューティング(HPC)

- ネットワークとデータセンター

- その他

第7章 市場推計・予測:最終用途産業別、2021 –2034

- 主要動向

- ITおよび通信

- ゲームとエンターテイメント

- ヘルスケアとライフサイエンス

- 自動車

- 軍事・防衛

- その他

第8章 市場推計・予測:地域別、2021–2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 日本

- 中国

- インド

- 韓国

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- サウジアラビア

第9章 企業プロファイル

- Advanced Micro Devices、Inc.(AMD)

- Broadcom Inc.

- Cadence Design Systems、Inc.

- Fujitsu Limited

- GlobalFoundries Inc.

- IBM Corporation

- Infineon Technologies AG

- Intel Corporation

- Marvell Technology Group Ltd.

- Micron Technology、Inc.

- Nanya Technology Corporation

- NVIDIA Corporation

- Qualcomm Incorporated

- Rambus Inc.

- Samsung Electronics Co.、Ltd.

- SK Hynix Inc.

- Synopsys、Inc.

- Taiwan Semiconductor Manufacturing Company Limited(TSMC)

- Toshiba Corporation

The Global High Bandwidth Memory Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 26.2% to reach USD 25.9 billion by 2034. The global shift toward data-centric technologies is reshaping the landscape of memory solutions, with high bandwidth memory emerging as a critical enabler for faster data processing and energy-efficient computing. As organizations across various sectors race to adopt next-generation technologies, the demand for high-speed, low-latency memory has seen a notable surge.

The growing influence of artificial intelligence (AI), machine learning (ML), advanced driver-assistance systems (ADAS), and 5G networks continues to fuel demand for powerful memory technologies. Enterprises are leaning heavily on HBM to support big data, high-resolution imaging, real-time analytics, and deep learning workloads. With digital transformation accelerating in sectors like automotive, healthcare, financial services, and media, HBM solutions are rapidly becoming foundational to the development of smarter, faster, and more connected systems. Companies worldwide are responding by investing in cutting-edge innovations and expanding manufacturing capabilities to stay competitive in this rapidly evolving space.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 26.2% |

The market is segmented by technology node into below 10nm, 10nm to 20nm, and above 20nm. The 10nm to 20nm category accounted for USD 1 billion in 2024 and is projected to grow at a CAGR of 26.7% between 2025 and 2034. This node has proven ideal for applications requiring balanced performance and cost-efficiency, such as automotive electronics, IoT devices, and mid-range consumer products. Its scalability, coupled with high-yield production and reliable thermal management, continues to make it a go-to option for developers aiming to optimize performance without inflating manufacturing costs.

Based on application, the high bandwidth memory market is categorized into GPUs, CPUs, FPGAs, ASICs, AI, ML, HPC, networking, and data centers. The GPU segment captured a 21.3% share in 2024, supported by soaring demand in professional and immersive gaming ecosystems. As ultra-high-definition graphics, real-time rendering, and extended reality environments become mainstream, graphics processing units are integrating advanced HBM technologies such as HBM3E to meet rising bandwidth needs. This trend is particularly prominent in the gaming and animation sectors, where rapid refresh rates and responsive user experiences are essential.

The Asia Pacific region led the global market with a 32.2% share in 2024. Meanwhile, the U.S. high bandwidth memory market was valued at USD 523 million in the same year, driven by the digital modernization of cloud and data center infrastructures. The country's vast number of data centers makes it a dominant force in HBM adoption, with real-time data analytics and edge computing applications paving the way for accelerated deployment.

Leading players in the global high bandwidth memory market include Cadence Design Systems, Inc., Advanced Micro Devices, Inc. (AMD), Broadcom Inc., GlobalFoundries Inc., IBM Corporation, Fujitsu Limited, and Infineon Technologies AG. These companies are investing heavily in R&D to boost the speed, scalability, and efficiency of their HBM offerings. Strategic alliances across AI, gaming, and semiconductor sectors further support their global expansion efforts.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Vendor matrix

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.7 Industry impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Expansion of Data-Intensive Applications

- 3.7.1.2 Growth of High-Performance Computing

- 3.7.1.3 Next-Generation Platform Integration

- 3.7.1.4 Enhanced gaming and graphics demand

- 3.7.1.5 Expansion of the data center and cloud services

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High Production Costs

- 3.7.2.2 Technical Integration Complexity

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Regulatory landscape

Chapter 4 Market Estimates and Forecast, By Memory Capacity, 2021 – 2034 ($ Mn & Bn GB)

- 4.1 Key trends

- 4.2 Less than 4GB

- 4.3 4GB to 8GB

- 4.4 8GB to 16GB

- 4.5 Above 16GB

Chapter 5 Market Estimates and Forecast, By Technology Node, 2021 – 2034 (USD Mn & Bn GB)

- 5.1 Key trends

- 5.2 Below 10nm

- 5.3 10nm to 20nm

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Mn & Bn GB)

- 6.1 Key trends

- 6.2 Graphics Processing Units (GPUs)

- 6.3 Central Processing Units (CPUs)

- 6.4 Field-Programmable Gate Arrays (FPGAs)

- 6.5 Application-Specific Integrated Circuits (ASICs)

- 6.6 Artificial Intelligence (AI) and Machine Learning (ML)

- 6.7 High-Performance Computing (HPC)

- 6.8 Networking and Data centers

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Mn & Bn GB)

- 7.1 Key trends

- 7.2 IT & telecom

- 7.3 Gaming & entertainment

- 7.4 Healthcare & life Sciences

- 7.5 Automotive

- 7.6 Military & defense

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021– 2034 (USD Mn & Bn GB)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 UAE

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Advanced Micro Devices, Inc. (AMD)

- 9.2 Broadcom Inc.

- 9.3 Cadence Design Systems, Inc.

- 9.4 Fujitsu Limited

- 9.5 GlobalFoundries Inc.

- 9.6 IBM Corporation

- 9.7 Infineon Technologies AG

- 9.8 Intel Corporation

- 9.9 Marvell Technology Group Ltd.

- 9.10 Micron Technology, Inc.

- 9.11 Nanya Technology Corporation

- 9.12 NVIDIA Corporation

- 9.13 Qualcomm Incorporated

- 9.14 Rambus Inc.

- 9.15 Samsung Electronics Co., Ltd.

- 9.16 SK Hynix Inc.

- 9.17 Synopsys, Inc.

- 9.18 Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- 9.19 Toshiba Corporation