|

市場調査レポート

商品コード

1689845

欧州の保険仲介市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Insurance Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の保険仲介市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

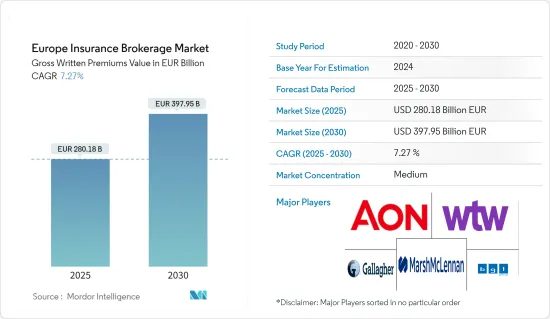

欧州の保険仲介市場規模(総保険料ベース)は、2025年の2,801億8,000万ユーロから2030年には3,979億5,000万ユーロに成長し、予測期間(2025~2030年)のCAGRは7.27%と予測されます。

保険仲介は現在、先進国の保険業務の約80%にサービスを提供している活動の一種です。保険市場、商品、価格、プロバイダを熟知し、保険顧客のニーズを理解する保険仲介は、独自の役割を得ることになります。保険仲介を持たない欧州数カ国のプラクティスを調べたところ、保険契約の締結件数は非常に少なかりました。

COVID-19の大流行は、保険会社にメガ動向への早急な対応を迫っており、りわけ重要なのは気候変動とデジタル化です。保険産業は、物理的な移行と気候変動による賠償リスクをより正確に理解し始め、保険引受と投資を見直そうとしています。

仲介会社の重要性を考えると、保険産業のデジタル化は流通チャネルにも影響を与えます。アグリゲーター、すなわちオンライン仲介は、過去20年間、欧州でその地位を確立してきました。技術の進歩は最終的に、仲介という重要な役割を担う欧州の仲介会社の将来を形作る。

ブレグジットは欧州連合(EU)と英国のありとあらゆる産業に永遠の影響を与えます。EUと英国で事業を展開する仲介会社も、この影響を免れることはできないです。登録から事業の収益性に至るまで、保険仲介はより慎重に仕事をしなければならないです。

欧州の保険仲介市場の動向

保険契約の需要増加が欧州の保険仲介市場を牽引

ベビーブーマーとミレニアル世代の人口拡大により、医療保険、生命保険、傷害保険の成長機会が生まれています。保険仲介は、顧客に最大限のメリットを提供する保険契約に注力しています。顧客に安心感を与え、個々人に合わせた金融サービスを提供することで、保険商品に対する需要が高まっています。保険会社はまた、保険市場における潜在力を引き出すため、革新的な保険施策やサービスに投資しています。このように、保険契約のメリットに関する意識の高まりが、予測期間中の欧州の保険仲介市場の成長を促進すると考えられます。

欧州におけるデジタル仲介の重要性が市場成長を急増させる見込み

欧州のアグリゲーターはデジタル仲介であり、専門アドバイザーはここ数年で大きく進化しました。推定によると、欧州のオンライン保険のほぼ50%はアグリゲーター経由で販売されています。多くの国で、アグリゲーターは顧客と接する側のビジネスを行っています。このビジネスは、アグリゲーターが高い利益率を獲得し、潜在的な買収者からM&Aへの関心が高まるなど、相互にメリットがあります。保険会社は、アグリゲーターのビジネスモデルの長所と短所を理解することで、大規模な顧客ベースに対応することができます。

アグリゲーターは一般的に、ある商品のスペシャリストとしてスタートし、より多くの業種を取り込むことでその幅を広げていきます。欧州の主要市場の多くでは、アグリゲーターの総収入の75%以上を保険商品が占めています。

欧州の保険仲介産業概要

本レポートでは、調査対象市場で事業を展開する大手保険仲介とオンラインアグリゲーター概要を掲載しています。一部の主要企業が市場シェアで調査対象市場を独占する寡占市場について詳しく取り上げています。本レポートでは、Marsh & McLennan Co.、Willis Towers Watson PLc、Arthur J. Gallagher & Co.、BGL Groupなどの主要企業の企業プロファイルを掲載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 欧州の保険産業の歴史的業績(保険タイプ別)

- 欧州における保険市場の流通チャネル

- 仲介の台頭-保険タイプ別市場シェア

- 仲介の台頭-国別市場シェア

- デジタルブローキング

- 欧州の保険市場におけるアグリゲーター概要

- 仲介技術の進化に関する産業の見解

- デジタルブローキングによるアンダーライティングとリードジェネレーションの自動化

- Bexitが欧州の保険仲介に与える影響

- ブレグジットによるEUと関係のある保険仲介のビジネスモデルの変化

- ブレグジットによる仲介事業への影響(保険タイプ別)

- 市場の促進要因

- 市場抑制要因

- この地域における規制状況の変化に関する概要

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- 保険タイプ別

- 生命保険

- 損害保険

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- ベルギー

- スペイン

- その他の国

第6章 競合情勢

- 市場集中度概要

- 企業プロファイル

- Marsh & McLennan Co.

- Willis Towers Watson PLC

- Aon PLC

- Arthur J. Gallagher & Co.

- BGL Group

- AmWINS Group Inc.

- Assured Partners Inc.

- NFP Corp.

- Lockton Companies

- HUB International Ltd*

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

The Europe Insurance Brokerage Market size in terms of gross written premiums value is expected to grow from EUR 280.18 billion in 2025 to EUR 397.95 billion by 2030, at a CAGR of 7.27% during the forecast period (2025-2030).

Insurance brokerage is a type of activity currently serving about 80% of insurance operations in the developed world. Insurance brokers who know the insurance market, its products, prices, and providers and understand the needs of insurance customers will gain a unique role. After looking at the practice of several European countries without insurance brokers, a very small number of insurance contracts were concluded.

The COVID-19 pandemic is pressing insurance companies to respond urgently to megatrends, most importantly, climate change and digitalization. The industry is starting to understand the physical transition more precisely and the liability risks of climate change and is revising underwriting and investments.

Given the importance of brokerage companies, the digitalization of the insurance industry also impacts the distribution channels. Aggregators, i.e., online brokers, have had their place in Europe for the past 20 years. The technological advancements ultimately shape the future of brokerage firms in Europe in the critical roles of brokers.

Brexit has an everlasting impact on every possible industry in the European Union and the United Kingdom. Brokerage firms with EU and UK operations are not exempt from this. From registration to business profitability, insurance brokers have to work more cautiously.

Europe Insurance Brokerage Market Trends

Increased Demand for Insurance Policies Driving the Insurance Brokerage Market in Europe

The expanding population of baby boomers and millennials generates growth opportunities for medical, life, and accidental insurance. Insurance brokers are focusing on insurance policies that provide maximum benefits for customers. Providing customers with security and personalized financial services has increased the demand for insurance products. Insurance firms are also investing in innovative insurance policies and services to tap their potential in insurance markets. Thus, increased awareness about the benefits of insurance policies is likely to drive the growth of the European insurance brokerage market during the forecast period.

Importance of Digital Brokers in the European Region is Expected to Surge the Market Growth

European aggregators are digital brokers, and expert advisers have evolved significantly in the past few years. As per an estimate, almost 50% of the online insurance in Europe is sold via aggregators. In many countries, aggregators have been the customer-facing side of their business. This business is mutually beneficial, as aggregators get good profit margins and a surge in M&A interest from potential acquirers. Insurers can cater to a large customer base by understanding the pros and cons of aggregators' business models.

Aggregators generally begin as specialists in any one product and broaden their reach by incorporating more verticals. Insurance products in many major European markets still account for 75% or more of aggregators' total revenue.

Europe Insurance Brokerage Industry Overview

The report includes an overview of the largest insurance brokers and online aggregators operating in the market studied. An oligopoly market with some of the major players dominating the market studied in terms of market share is covered in detail. The report covers company profiles of major players including, Marsh & McLennan Co., Willis Towers Watson PLc, Arthur J. Gallagher & Co., BGL Group, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.1.1 Historical Performance of the Insurance Industry in Europe, by Insurance Type

- 4.1.2 Distribution Channels for the Insurance Market across Europe

- 4.1.3 Prominence of Brokers - Market Share by Insurance Types

- 4.1.4 Prominence of Brokers - Market Share by Country

- 4.2 Digital Broking

- 4.2.1 A Brief about Aggregators in the European Insurance Market

- 4.2.2 Industry Perspective on the Evolution of Broker Technology

- 4.2.3 Automation of Underwriting and Lead Generation Through Digital Broking

- 4.3 Impact of Bexit on Insurance Broking in Europe

- 4.3.1 Changes in Business Models of Insurance Brokers with EU Ties due to Brexit

- 4.3.2 Impact on Broking Business due to Brexit, by Insurance Type

- 4.4 Market Drivers

- 4.5 Market Restraints

- 4.6 A Brief on Evolving Regulatory Landscape in the Region

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type of Insurance

- 5.1.1 Life Insurance

- 5.1.2 Non-life Insurance

- 5.2 By Country

- 5.2.1 Germany

- 5.2.2 United Kingdom

- 5.2.3 France

- 5.2.4 Italy

- 5.2.5 Belgium

- 5.2.6 Spain

- 5.2.7 Other Countries*

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Marsh & McLennan Co.

- 6.2.2 Willis Towers Watson PLC

- 6.2.3 Aon PLC

- 6.2.4 Arthur J. Gallagher & Co.

- 6.2.5 BGL Group

- 6.2.6 AmWINS Group Inc.

- 6.2.7 Assured Partners Inc.

- 6.2.8 NFP Corp.

- 6.2.9 Lockton Companies

- 6.2.10 HUB International Ltd*