|

市場調査レポート

商品コード

1687740

エスニック食品:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Ethnic Foods - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エスニック食品:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

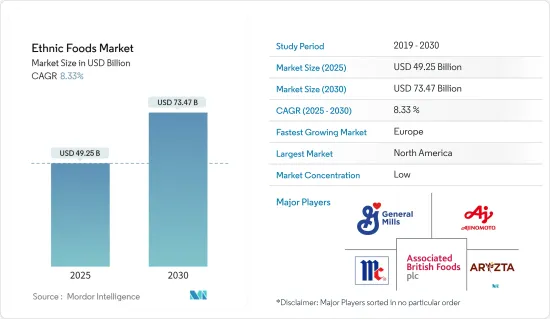

エスニック食品の市場規模は2025年に492億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.33%で、2030年には734億7,000万米ドルに達すると予測されます。

COVID-19以降、消費者はさまざまな民族に由来する多様な調理済み食品の摂取を緩やかに増加させ、世界中で広く求められているため、当年はエスニック食品の需要を牽引しています。

雇用機会、高等教育、観光による移民率の増加に伴い、エスニック食品の需要は増加しており、中期的には、栄養価の高い食品の消費の増加と、健康的なエスニックベースの食品を生産するための設備投資の増加に伴い、予測期間中に調査された市場は牽引力を増すと予想されます。

エスニック食品の需要を促進する要因のひとつは、エスニック食品専門のスーパーマーケット・チェーンを通じてエスニック食品を入手しやすくなっていることです。新興諸国では西洋化が進み、人々の嗜好が変化しています。外食が一般的になり、大陸間料理やエキゾチックな料理を試したいと思う人が増えています。消費者が革新的で創造的な料理を好むようになった結果、食品はより治療的なものになりつつあります。

さらに、エスニック食品メーカーは、製品の利便性、食品の品質、料理のバリエーション、包装形態に注目しています。エスニック食品市場は、消費者が新しい世界の料理を試し続けているため、多様化が続いています。ニッチなエスニック食品カテゴリーには、アフリカ料理、インド料理、インドネシア料理などがあり、これらは最近成長しつつあります。

エスニック食品市場の動向

米国のエスニック食品市場空間におけるアジア料理の存在感

タイ料理、韓国料理、ベトナム料理、日本料理などのアジア料理に対する消費者の関心は世界的に高まっており、大胆な味を求めるようになっています。この動向の原動力となっているのは、移民人口の増加に加え、先住民からの旺盛な需要です。

過去10年間で、アジアから米国や欧州諸国に移り住んだ移民の数は、世界的に見ても他のどの地域よりも多いです。例えば米国では、2021年にはアジア諸国からの移民が移民全体の47%を占めました。このことが、同国におけるエスニック食品の需要を煽っています。

さらに、韓国料理、日本料理、中華料理、インド料理が原住民の間に浸透していることも、調査期間中に顕著でした。予測期間中、世界のエスニック食品産業はエスニック・ブレンドの融合に依存する可能性が高いです。

アジア太平洋地域におけるエスニック料理への嗜好の高まり

若い人口が増加していることに加え、州をまたがる様々な料理や国をまたがる料理を頻繁に食べたり試したりするというペースの速い動向が、アジア太平洋地域のエスニック料理サービス事業に多くの成長機会をもたらしています。

インド人やその他の発展途上国の人々の間でソーシャルメディアの利用が増加しているため、彼らが自分の料理体験を共有することが可能になり、共有されたレビューに基づいて消費者が新しい料理の選択肢や店舗を試すよう促しています。アジア太平洋の消費者の間では、世界な料理や本格的な郷土料理を求めて新たな食体験を探求する傾向が高まっています。さらに、メーカー各社は、より多くの国際的な人気料理、付加された多様性、スパイス、大胆な風味を備えた、新しく異なる食品に対する消費者の需要を満たそうと努力しています。

アジア太平洋地域のスーパーマーケットでは、消費者、特にミレニアル世代がエスニック料理に傾倒しているため、特殊食品と国際食品の販売が増加しています。海外旅行やグローバリゼーション政策など、その他の要因も市場にプラスの影響を与えています。

エスニック食品業界の概要

エスニック食品市場は競争が激しく、さまざまな中小企業が参入しています。市場の主要企業には、味の素株式会社、マコーミック・アンド・カンパニー・インク、アソシエイテッド・ブリティッシュ・フーズ PLC、ゼネラル・ミルズ・インクなどがあります。

中華料理、イタリア料理、インド料理、英国料理、フランス料理、メキシコ料理、カリブ料理、アフリカ料理など、人気の高い料理を含む多様な製品ポートフォリオを開発することで、主要企業は消費者に様々な料理を販売しています。主要企業はまた、複数の流通チャネル、特にスーパーマーケットとハイパーマーケットに製品を提供することに成功しており、これらは調査対象市場の流通チャネルにおいて最大級のセグメントを占めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 流通チャネル

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- オンライン小売チャネル

- その他の流通チャネル

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- 英国

- ドイツ

- スペイン

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- 最も活発な企業

- 主要企業の戦略

- 市場シェア分析

- 企業プロファイル

- Ajinomoto Co. Inc.

- McCormick & Company Inc.

- Associated British Foods PLC

- General Mills Inc.(Old El Paso)

- Orkla ASA

- ARYZTA AG

- Paulig Ltd.

- Asli Fine Foods

- Capital Foods(Ching's Secret)

- Charlie Bigham

- The Spice Tailor

- Quality Ethnic Foods Inc.

第7章 市場機会と今後の動向

The Ethnic Foods Market size is estimated at USD 49.25 billion in 2025, and is expected to reach USD 73.47 billion by 2030, at a CAGR of 8.33% during the forecast period (2025-2030).

Post-COVID-19, consumers moderately increased the intake of a variety of ready-to-eat food products, which come from various ethnicities and are popularly demanded across the world, driving the demand for ethnic foods during the current year.

With the growing immigration rates due to employment opportunities, higher education, and tourism, the demand for ethnic food has been increasing, and over the medium term, with the increasing consumption of nutritious food and rising capital investment in producing healthy, ethnic-based food, the market studied is expected to gain traction over the forecast period.

One factor driving ethnic food demand is the availability and accessibility of ethnic food items through specialized ethnic food supermarket chains. Developing countries are experiencing an increase in westernization, which is changing people's tastes and preferences. It is becoming more popular to eat out, and more people are interested in trying intercontinental and exotic foods. Food is becoming more therapeutic as a result of consumers' growing preference for innovative and creative cuisines.

Moreover, ethnic food manufacturers are focusing on the convenience factor, quality of food, cuisine variants, and packaging formats of the products. The ethnic food market continues to diversify as consumers continue to experiment with new global cuisines. Some of the niche ethnic food categories include African, Indian, and Indonesian cuisines that have been growing over the recent past.

Ethnic Food Market Trends

Presence of Asian Cuisine in the US Ethnic Food Marketspace

Consumers' interest in Asian cuisines, such as Thai, Korean, Vietnamese, and Japanese, is increasing globally, and they seek bold flavors. This trend is driven by the increasing immigrant population, as well as robust demand from native populations.

Over the past decade, more immigrants have moved to the United States and European countries from Asia than any other region globally. For instance, in the United States, immigrants from Asian countries constituted 47% of the total immigrants to the country in 2021. This has fuelled the demand for ethnic foods in the country.

Furthermore, the penetration of Korean, Japanese, Chinese, and Indian cuisines among the native population has been strong over the review period. During the forecast period, the global ethnic food industry is more likely to rely upon the fusion of ethnic blends.

Increasing Indulgence in Ethnic Food in the Asia-Pacific Region

The growing young population, along with the fast-paced trend of eating and experimenting with various interstate and inter-country food cuisines frequently, has provided many growth opportunities for ethnic food services operations in the Asia-Pacific region.

The increasing use of social media among Indians and people from other developing countries has enabled them to share their culinary experiences, urging consumers to try new food options and outlets based on the reviews shared. Exploring new culinary experiences for global and authentic regional cuisines is rising among consumers in Asia-Pacific. Moreover, manufacturers are striving to satisfy the demand from consumers for new and different food products with more international favorites, added variety, spices, and bold flavors.

Specialty and international food sales are increasing in supermarkets in Asia-Pacific as consumers, especially millennials, are inclined toward ethnic cuisines. Other factors, such as international travel and globalization policies, influence the market positively.

Ethnic Food Industry Overview

The ethnic foods market is competitive, with various small and medium-sized companies. Some major companies in the market include Ajinomoto Co. Inc., McCormick & Company Inc., Associated British Foods PLC, and General Mills Inc.

By developing diversified product portfolios, which include popular cuisines such as Chinese, Italian, Indian, English, French, Mexican, Caribbean, and African, the leading companies are marketing various cuisines to consumers. The top players have also succeeded in providing their products across multiple channels of distribution, particularly supermarkets and hypermarkets, which also happen to hold some of the largest segments in terms of distribution channels in the market studied.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Distribution Channel

- 5.1.1 Supermarkets/Hypermarkets

- 5.1.2 Convenience Stores

- 5.1.3 Online Retail Channels

- 5.1.4 Other Distribution Channels

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 Spain

- 5.2.2.4 France

- 5.2.2.5 Italy

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Rest of the World

- 5.2.4.1 South America

- 5.2.4.2 Middle East & Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Strategies Adopted by Key Players

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Ajinomoto Co. Inc.

- 6.4.2 McCormick & Company Inc.

- 6.4.3 Associated British Foods PLC

- 6.4.4 General Mills Inc. (Old El Paso)

- 6.4.5 Orkla ASA

- 6.4.6 ARYZTA AG

- 6.4.7 Paulig Ltd.

- 6.4.8 Asli Fine Foods

- 6.4.9 Capital Foods (Ching's Secret)

- 6.4.10 Charlie Bigham

- 6.4.11 The Spice Tailor

- 6.4.12 Quality Ethnic Foods Inc.